Now some might say this is what makes for a robust market. But anyone who has actually tried to make a buck knows that the ideal scenario is a market as tilted, unfair and asymmetric as possible. Enterprises cherish their advantages and go to great lengths; not just to protect them, but to deny their benefits to others.

So when lots of really smart, really rich people start applying the same hardware and software to solving the same challenge - make me more money then the next guy - they quickly find that all those statistically significant conclusions tend to cancel each other out. The result is that no one is making much more than their competitors, which can be bad for business when your primary selling point is how much better you are. And blaming the markets does not tend to score points with customers, either.

That, in short, is why situational awareness, interpretation and self-knowledge may be more valuable than all the algorithms in America. Or anywhere else. JL

The Economist reports:

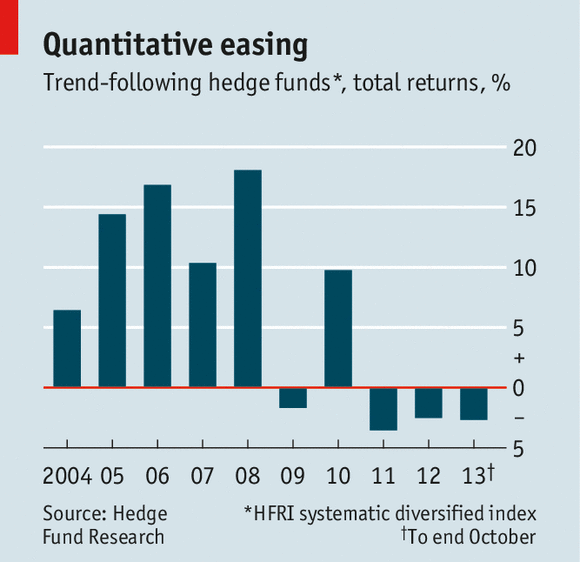

IF SOMETHING has not worked for five years, most people would conclude that it was broken. Tell that to the geeks managing “quant” hedge funds, who craft elaborate algorithms to profit from market movements. Once money-spinners, their prized formulae have misfired since 2009, losing money in four of the past five years.

Unless their results improve markedly, the giant funds will finish this year as the worst-performing of the most common hedge-fund strategies.

“Trend-following” involves programming computers to analyse market movements and try to infer where they might go next. Practitioners speak with reverence of “crossover levels” and “momentum speeds” leading to “breakout points”. A rough translation is that a trend that lasts a few days or weeks can profitably be invested in until it reverses, at which point a new trend may already be forming. Whether the markets are going up or down does not matter. Nor does the underlying asset being analysed—typically a futures contract linked to a commodity or a security.

After prospering through the market rout of 2008 (the prolonged slump gave even the dimmest trend-follower time to cotton on), the sector swelled from $91 billion to $215 billion, according to Hedge Fund Research, a data provider. Winton Capital, Man Group’s AHL fund, Cantab, BlueCrest and other “black box” traders, as their critics dub them, became darlings of the investing world. Unfortunately, the influx of investment coincided with the reversal in the strategy’s fortunes.

The main problem is not with the quants’ models, practitioners insist, but with the markets themselves. In the aftermath of the financial crisis, they have been dancing to the tune set by politicians and central bankers. Efforts to save the euro or stave off deflation regularly send markets into convulsions, in the process distorting the historical patterns that the algorithms are designed to exploit. The ensuing jolts and crashes have no precedent, leaving even the most finely crafted trade at risk from political meddling. Not even the world’s wiliest supercomputers can predict what the European Central Bank will dream of next, apparently.

Worse, such interference prompts stocks, bonds and commodities to move in unison. When in May the Federal Reserve hinted at a “tapering” of America’s ultra-loose monetary policy, for example, both government bonds and shares tumbled. What had started out as a good year for the trend-followers turned into a drubbing. One of the sector’s main selling-points, that its returns are uncorrelated to those of other asset classes, is at risk.

The quants are remarkably sanguine about their recent record. “Performance since 2009 in traditional strategies hasn’t been great, but it’s no disaster either,” says Sandy Rattray, AHL’s boss. Many of the stock-picking hedge funds that had been lionised for making money in the crash suffered large losses in subsequent years, he points out. Low interest rates, which depress returns on the safe assets quants hold as collateral to back their trades, have not helped.

The big unknown is whether trend-following will ever work again. The quants are adamant that the models are simply in hibernation. Profits will return, they say, as soon as prices revert to being dictated by investors rather than policymakers. “Imagine where bonds would be trading if it weren’t for the interference,” says Leda Braga of BlueCrest.

Some wonder whether the growth of quant-fund investing has irreparably harmed returns. Decent trend-following algorithms can be bought online. Some of the funds are adapting in response. Winton, the biggest, now invests some of its cash in equities; it is among the few to have risen in value this year, albeit modestly. AHL is focusing its energies on trading in more esoteric markets, like German power or iron-ore futures, which it hopes are less crowded. Yet it is hard to find markets that are immune to political meddling, or politicians who are inclined to let the forces of finance be. Trend-followers may yet prosper again, but the breakout point, as it were, may be some way off.

0 comments:

Post a Comment