One of the reasons PCs are declining in usage is more fundamental than the growing interest in mobility: manufacturers of the machines are finding that their profits and revenues are being squeezed, irredeemably. That makes continued investment in that platform less justifiable. JL

Charles Arthur reports in The Guardian:

The problem for Windows PC makers is that they are caught in the "value

trap". Even as prices are being forced down by commoditisation and slumping

demand, they have no obvious way to capture any of the money that a consumer who

buys one of their products subsequently spends with it. The news that LG

is considering quitting the traditional Windows PC business isn't

surprising. LG has always been a bit player in the PC market, with shipments of

at best a few million PCs per year - in a market where the largest companies

would expect to shift 10 times more.

As one unnamed LG employee told the Korean Times, exiting the PC business

makes sense: "it doesn't make sense to put more resources into the money-losing

business."

It's not just LG that's hurting. The PC business is in a slump which has seen

year-on-year shipments (and so sales) of Windows PCs fall for five (imminently,

six) quarters in a row, after seven quarters where they barely grew by more than

2%.

The situation is a long way from the boom times of the late 1990s, which saw

20%-plus quarterly growth.

And it's not only growth that's fallen. Analysis by the Guardian suggests

that as well as falling sales, the biggest PC manufacturers now have to contend

with falling prices and dwindling margins on the equipment they sell.

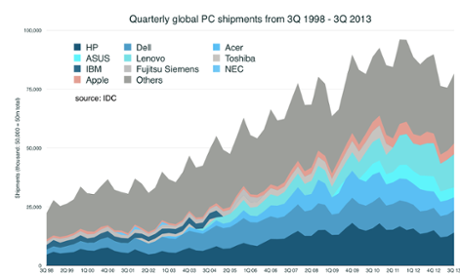

Price and profit falls

PC market global shipments, 3Q 1998 - 3Q 2013.

Source: IDC. Photograph: /IDC/PR

My research took published data from the quarterly financial figures for HP,

Dell, Lenovo, Acer and Asus, which together make more than 60% of the world's

Windows PC shipments.

By comparing revenues, operating profits (which excludes one-off windfalls

from investments) and the proportion of revenues derived from business segments,

it's straightforward to figure out how much each PC costs to make, and how much

profit it generates for the big companies. (For Acer and Asus, which operate in

Taiwan, I used the prevailing exchange rate at each quarter's end to give US

dollar revenues. Lenovo reports its figures in US dollars.)

This yields the "weighted average selling price" (ASP) of PCs from those

companies. It's weighted because HP sells more PCs than Acer; and the ASP is the

price at which the manufacturers sell machines to wholesalers, not the end-user

price.

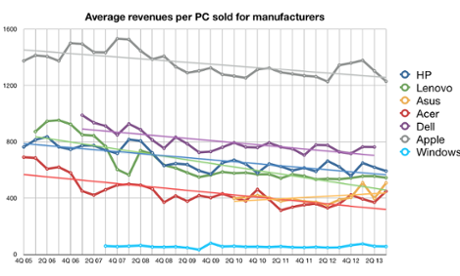

Bitten by ASPs

Average per-PC revenues for various PC

manufacturers over time, by quarter. Lines show overall price trend. Based on

reported revenues and shipments figures from accounts (Apple) or IDC (others).

Photograph: /IDC/PR

The data shows that the weighted average selling price (ASP) of a PC has

fallen from $614.60 in the first quarter of 2010 to just $544.30 in the third

quarter of 2013, the most recent date for which data is available.

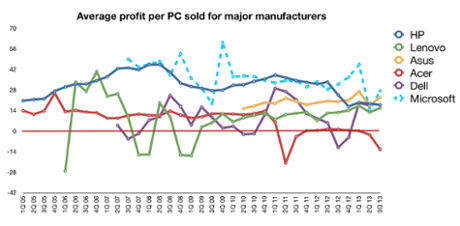

Even worse is the profitability. From the financial data and shipment data,

it's easy enough to calculate the per-PC profitability of each company, though

it creates a confusing picture. (The Microsoft figure is calculated from figures

given for its Windows division; however, they vary greatly because much of that

division's revenue comes from corporate sales to its existing installed base of

PCs, rather than directly from shipments.) Average per-PC profit for major PC

manufacturers, by quarter. Calculated from published financial data and IDC

shipment figures. Photograph: /Guardian

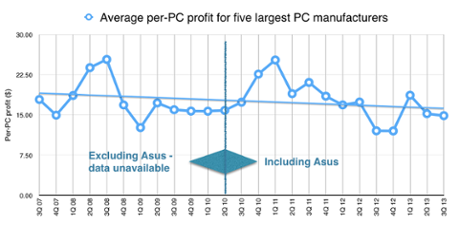

It's hard to see what's happening immediately. But we can calculate a

"weighted average profit per PC" by looking at the profitability of each

company, and weighting that by the number of PCs shipped. This gives a far

clearer picture. Average per-PC profit for the five largest PC

manufacturers, with trend line. Note: doesn't include Asus data before 2Q 2010

as PC shipment data isn't available. Photograph: /Guardian

In the first quarter of 2010, the weighted average profit per PC was $15.71 -

a 2.55% margin. (So the overall per-PC cost of manufacture, sales and marketing

was just under $599.)

But since then, the rise of smartphones (which began outselling PCs at the

end of 2010) and the arrival of the iPad and other tablets have eaten into the

fortunes of PC makers.

So much so that by the third quarter of 2013, the weighted average profit had

fallen to $14.87.

That actually marks an improvement in margin, to 2.73% - but the absolute

fall both in profits and numbers shipped means that companies are struggling.

(The per-PC manufacturing/marketing/sales cost fell to $529. It's getting

cheaper to produce PCs - but the price they're being sold for is falling

too.)

For the Taiwanese company Acer, it has meant a brutal boardroom shakeout that

saw its chief executive forced out after two successive quarters of losses.

That contrasts with the

comments made in January 2010, when its founder Stan Shih remarked that

US-based PC manufacturers would die out over the next 20 years because they

couldn't make the low-priced netbook computers that consumers were

demanding.

"The trend for low-priced computers will last for the coming years," said

Shih confidently.

The problem is that his prediction is coming true. PCs are getting cheaper.

But they're not making much money for their makers. Welcome to the value

trap.

While HP and Dell (and to a lesser extent Lenovo) use PC sales to

corporations as the Trojan horse for more profitable services contracts, any PC

sale to a consumer is effectively the end of the financial relationship. The

OEMs can't extract any more value from them. That's why many tried (and still

try) to extract as much as possible at the point of sale. Chrystalla Labesque,

PC analyst at research company IDC, points to Dell as a classic example: "It was

the leader in pushing costs down, and adding additional services as a way to

improve their hardware margin - so when selling notebooks to consumers, they

would offer antivirus and notebook accessories. Those could double their per-PC

profit."

When you think how thin

that profit could be, you understand the purpose of "crapware" preinstalled on

so many Windows PCs: to escape from the value trap. As Jack Schofield noted in

recommending

a Dell purchase last May, "Dell's Vostro range is aimed at boring business

buyers rather than consumers, so they tend to be well made and they don't

include a lot of bundled crapware to mess things up."

For Asus and Acer, which don't have substantial sales to business, the

attempted solution has been to offer "cloud" services, though with little

result. The idea is sound - retain consumers by tying them to the brand, and so

to future sales - but set against the might of Google or Microsoft, it's an

uphill struggle.

The value trap is deep, though. Because Windows and its apps are easily moved

from one PC to another (which is a huge benefit to the consumer), it's almost

impossible for hardware makers to differentiate themselves from rivals. In the

past, their best hope has been to encourage repeat buying through having extra

hardware features; that's what some are trying to do with touchscreen laptops

and desktops now. But there's little sign that buyers are enthusiastic about

those, preferring instead to buy offerings that are just a little cheaper.

That means there is always downward pressure on both prices and margins,

while the only way to make useful profits is to be able to build at scale.

The alternative is, like HP and Dell, to use PCs as a Trojan horse to sell

much more profitable services to businesses.

The value trap is the

reason why Léo Apotheker suggested that HP

should sell off its PC-selling Personal Systems Group (PSG) when he was head

of the company in 2011. PSG is HP's biggest division in revenue terms - but its

worst-performing in profit margin, at less than 5% compared to Imaging (15%),

Software (20% or more), Storage/Networking (15%), and until recently Services

(which have dipped from 15% to 4%).

Apotheker reasoned that if PSG could be spun off without hurting the rest of

HP, overall margins would lift, and so would the stock. The rest of the board

decided though that that wasn't possible - and spun Apotheker off instead.

Dell, similarly, has struggled ever to make money selling its PCs to

consumers: its "global consumer" division had profit margins which averaged 1%

between February 2007 and January 2013. The rest of its business was much more

profitable, but it's clear that selling PCs to the average person at home just

wasn't a good business for it. (Dell's per-PC profits are calculated from its

total PC revenues and its consumer segment profits.)

"Dell isn't really present in the consumer market," says Labesque.

Lenovo, which completed its acquisition of IBM's PC business in the second

quarter of 2005, has also struggled with profitability - but since it increased

its reach by moving beyond China in the past couple of years, it has become more

and more dominant, and profitable. It's managing to do this even while competes

in smartphones - something that HP, its rival for the PC crown, has signally

failed to do. "With Lenovo, what isn't reflected is that they have a strong

position in China, which means that they have efficiencies which other vendors

can't leverage," explains Labesque.

Asus and Acer, meanwhile, are clearly troubled by the disappearance of

netbooks, even though those pulled down the ASP of PCs, because it has forced

them into the potentially unprofitable field of tablets. Acer's financial

results suggest that it has made a loss on almost every PC it has sold since the

second quarter of 2011. Its best performance in that space was in the second

quarter of 2012 - when for every PC it sold, it made an average profit of just

$1.13.

Asus's plans for the future

- as set out in its Q3

2013 presentation (PDF) - focus on tablets, and particularly in trying to

find extra profits there.

But even with tablets, it's not easy. Asus estimates the TAM - total

addressable market - as 202m, or 230m if you include "white box" makers in China

making super-cheap devices. The competition there is ferocious, with the same

downward pressure on price that is seen in PCs; and Apple always lurks at the

high end with the iPad.

In the personal computer market, Apple wins both ways: its ASPs are much

higher than those of rival computer manufacturers, and it used to be able to

sell OS upgrades, as well as upgrades to its iLife media and iWork office

suites, providing a small but reliable income.

This year, it has decided

to stop charging for any of those upgrades - but it still takes a 30% commission

on software bought through its Mac App Store (though users can still download

and buy desktop apps from the web). With a claimed

installed base worldwide of 72m as of summer 2013 (up from 66m in summer

2012), it's a tidy revenue stream - especially compared to the pit that PC

manufacturers find themselves in.

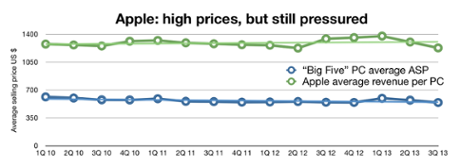

Apple: squeezed, but less so

Apple average PC selling price v "weighted"

average PC selling price for five main manufacturers. Photograph:

/Guardian

Apple isn't immune from the downward pressure on pricing, though they've only

been mildly eroded, as shown in the graph. Its ASPs have eroded only mildly

since 1Q 2010, from $1,277.61 to $1,229.56 (a 4% drop).

And how profitable are Macs on their own, even without that revenue stream?

Apple doesn't break out the figure for Mac profitability. But Horace Dediu of

the Asymco consultancy reckons there's a good-enough rule of thumb: assume that

Macs have an 18.9% profit margin, which fits well enough with its historical

operating margins.

That metric gives a hardware per-PC profit which has dropped from $241 to

$232 - an erosion, certainly, but a margin that Windows PC makers would kill

for: it's more than 10 times greater than their per-PC profit.

Labesque at IDC says: "Apple's cost to produce machines might be higher, but

it isn't fundamentally different from other PC manufacturers. They used to have

the best hardware margin - double-digit [ie over 10%] - while Acer, for

instance, has been losing money."

She notes that once you go outside the top-tier manufacturers, "then there's

Apple, and Samsung, and Sony, which are more consumer and lifestyle brands,

where they can ask for a premium price." Doing that, of course, generally points

to better margins. Samsung shipped around 11m PCs in 2013, and Sony slightly

fewer than 5m, according to IDC. Apple sells around 16m PCs per year.

Winners - and losers?

So who wins? The most obvious beneficiary of every Windows PC sale is

Microsoft. It gets revenue from the sale of the Windows licence - but it then

captures extra value through the high likelihood that even consumer buyers of

PCs will buy its Office suite, and probably buy another version of Windows at

some point in that computer's life. It's the reason why Microsoft is so

fabulously profitable, while PC manufacturers are struggling.

Into this, the arrival of

Chromebooks - running Google's Chrome OS - could be the early signs of a

disruption. Although sales are tiny compared to the overall PC market, at a few

million in 2013, they have the potential to undermine many of Microsoft's most

lucrative markets. Chromebooks don't run Windows; they don't run Office. But

they do pretty much everything that the average user needs (apart perhaps from

running Skype; Microsoft's never going to go there). Google has been pushing

Chromebooks into education and enterprises, with

some success - as noted by NPD (in data that was badly misunderstood by

many, who thought it was referring to consumer sales).

In July, Stephen Baker of NPD told Bloomberg: “While we were sceptical

initially, I think Chromebooks definitely have found a niche in the marketplace…

The entire computing ecosystem is undergoing some radical change, and I think

Google has its part in that change.”

At the research group Gartner, where research director Annette Jump agrees

that "the profit squeeze on PCs is very real", the expectation is that

Chromebooks will make slow - but real - inroads. For 2013, it reckons that

Chromebooks would have been about 0.5% of total shipments - compared to 92% for

Windows, 6% for Apple and 1% for Linux.

By 2017, the expectation is that the overall market will be about the same

size, or slightly smaller. Windows will have fallen to just 83%; Apple will make

up 11% (which, if even vaguely correct, would be its largest share in decades),

while Chrome will be about 4.5%.

That might not be a lot of Chromebooks, though it's likely they could be

going to some key customers: the ones who used to reliably buy Windows and then

subsequently Office.

For Microsoft, that is a

threat - and one which may be behind its curious decision to make an advert

dissing Chromebooks. Consumers probably won't care that they don't run

Office; the advert's "dog whistle" message may have been to people in businesses

considering them.

Meanwhile for PC

manufacturers, seeing sales slump and profits weaken, something certainly does

have to change. So maybe we should take it as a portent that although LG did

announce a couple of

hybrid Windows 8 machines at the International Consumer Electronics Show

(CES) this week, the only computer is showed off in its stage presentation was

an all-in-one (AIO) desktop computer.

And its software? ChromeOS.

I really like and appreciate your work which is about shipment data. The article you have shared here is great. I read your post with carefully, the points you mentioned can be very helpful. It is nice seeing your wonderful post. Import Export Shipment Details

As a Partner and Co-Founder of Predictiv and PredictivAsia, Jon specializes in management performance and organizational effectiveness for both domestic and international clients. He is an editor and author whose works include Invisible Advantage: How Intangilbles are Driving Business Performance. Learn more...

1 comments:

I really like and appreciate your work which is about shipment data. The article you have shared here is great. I read your post with carefully, the points you mentioned can be very helpful. It is nice seeing your wonderful post. Import Export Shipment Details

Post a Comment