That means that the amount of energy needed to power a unit of GDP is going to decline.

The reason is that more alternatives are becoming available, but more importantly, energy users at both the corporate and national levels are becoming more skilled at applying their knowledge and experience to the challenge of reducing the amount of energy volume and financial commitment required to run their economies.

This will mean that those resources will be freed up for use in other ways that may be more productive for their economies as a whole. This may well mean that economic growth will be stimulated at a comparable rate.

The implication for OPEC countries and others dependent on energy production is that the future may not be quite so rosy. While most Americans and Europeans will not grieve at this news, the geopolitical impact could be unsettling. Economies whose economic health is based on the sale of energy - from the Middle East, to emerging nations in South America to Russia - will experience a reduction in oil related revenues. The resultant instability may well affect energy consumers as well as oil producing states.

Fossil fuels will remain the dominant energy source for the foreseeable future but their market share will gradually decline. That they will comprise a decreasing amount of investment relative to the growth of the global economy is positive news for innovation, trade, employment, most other economic indicators - and the people whose lives are affected by them. JL

Izabella Kaminska reports in the Financial Times:

Whether the Opec cartel is busted or not, energy intensity of GDP (or how much energy it takes to create $ units of GDP) is likely to keep decreasing regardless.

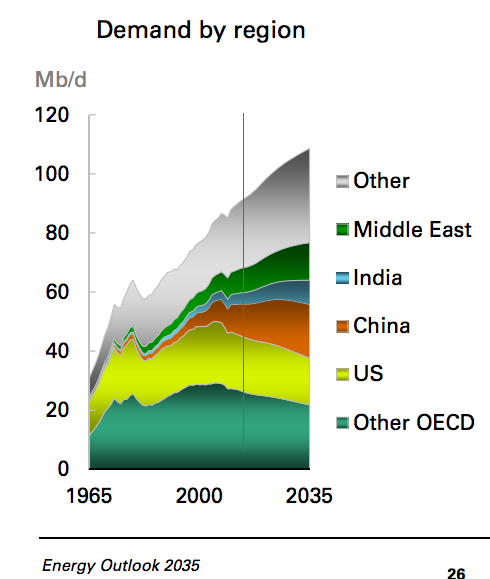

Global energy demand will continue to grow, but that growth is set to slow, driven by emerging economies — mainly China and India.

Notably, BP predicts the fuel mix will also slowly shift away from fossil fuels in that timeframe.

Some notable points from the presentation slides on that front:

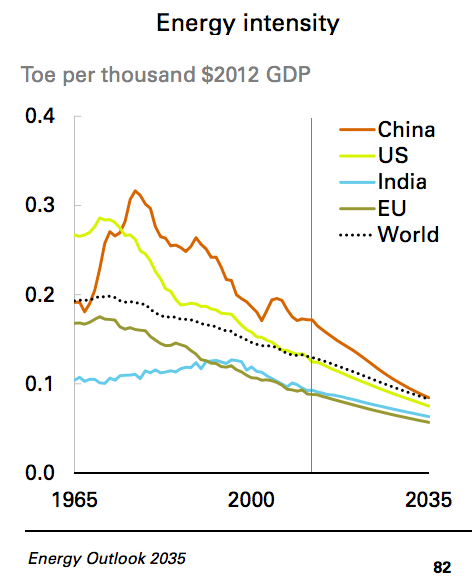

Energy consumption grows less rapidly than the global economy, with GDP growth averaging 3.5% p.a. 2012-35. As a result energy intensity, the amount of energy required per unit of GDP, declines by 36% (1.9% p.a.) between 2012 and 2035. The decline in energy intensity accelerates; the expected rate of decline post 2020 is more than double the decline rate achieved 2000-2010.And here’s the anticipated downward shift in demand for liquid fuels by region:

Fuel shares evolve slowly. Oil’s share continues to decline, its position as the leading fuel briefly challenged by coal. Gas gains share steadily. By 2035 all the fossil fuel shares are clustering around 27%, and for the first time since the Industrial Revolution there is no single dominant fuel. Taken together, fossil fuels lose share but they are still the dominant form of energy in 2035 with a share of 81%, compared to 86% in 2012. Among non-fossil fuels, renewables (including biofuels) gain share rapidly, from around 2% today to 7% by 2035, while hydro and nuclear remain fairly flat. Renewables overtake nuclear in 2025, and by 2035 they match hydro.

Needless to say, the above paints a worrying picture for Opec member counties, which are likely to have their economic growth models severely tested by any reduction or slowdown in projected forward demand.

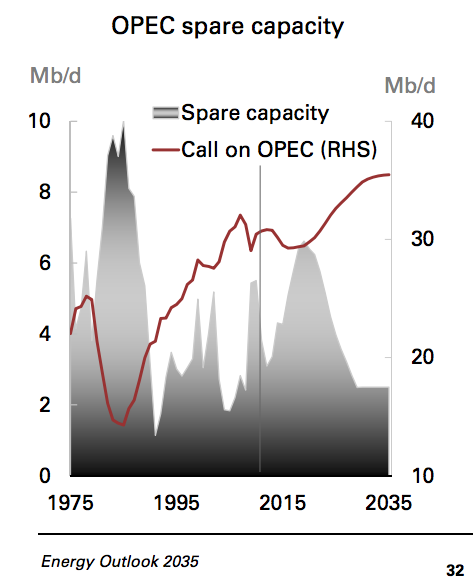

BP agrees: the oil balance suggests that by 2018 OPEC could be severely challenged. If it reacts with production cuts as expected, that could take Opec spare capacity to levels unseen since the late 1980s.

In our outlook, demand growth slow s and non-OPEC supplies rise – both as a result of high prices. We assume that OPEC members cut production over the current decade. As a result, spare capacity will exceed 6 Mb/d by 2018, the highest since the late 1980s.The problem for Opec countries is that what they make up in prices as a result of production cuts they lose in national income revenues. Also, the higher prices stay (at the cost of Opec income revenues), the more alternative producers are encouraged to offset Opec’s production base.

The market requirement for OPEC crude is not expected to reach today’s levels for another decade before rebounding. While we believe that OPEC members will be able to maintain discipline despite high levels of spare capacity, cohesion of the group is a key oil market uncertainty. The challenging decade ahead for OPEC, however, is unlikely to be a repeat of the 1980s. At that time, spare capacity peaked at over 10 Mb/d and the group’s share of global supply dropped well below 30%. The key difference is the response of demand, which collapsed after the price shock of the 1970s, due to the combination of fuel substitution and efficiency improvements. Furthermore, spare capacity as a share of crude production will peak at 7%, compared to 17% in 1985.

If Opec buckles, however, and prices collapse, this could have extremely complex implications for global growth, especially if the deflation that transpires is not recognised as a supply-side shock rather than a demand-side collapse.

Interestingly, according to BP, irrespective of whether the Opec cartel is busted or not, energy intensity of GDP (or how much energy it takes to create $ units of GDP) is likely to keep decreasing regardles:

As they note:

Global energy intensity is improving rapidly, converging across countries at lower and lower levels. We project it to decline by a further 36% by 2035 (-1.9% p.a.), with differences across countries the smallest since the Industrial Revolution. Decline and convergence are both the outcome of market forces and global competition, promoting the most efficient use of energy everywhere.All of which is relatively good news for carbon emissions:

The widening gap between GDP and energy consumption illustrates the impact of falling energy intensity; and the gap between energy and CO 2 emissions reflects changes in carbon intensity, brought about by changes in the fuel mix. Without the projected decline in energy intensity, CO 2 emissions in 2035 would be more than 40% higher than our forecast, given the projected economic growth. The effect of the expected change in the fuel mix is much smaller – about one fifth as large – though bigger than in the past.The question is, are inflation-concerned central bankers watching these trends? And if so, are they ready to adapt their models to a new, less-energy-intensive type of growth?

0 comments:

Post a Comment