Can ease of extending and using credit overcome the presumption of security and financial probity? JL

Kevin Peachey reports in BBC News:

A plastic ring, a bracelet and a keychain which all contain a chip allowing the shopper to make payments on credit. This is just a bridge to technology that will see customers

identified by their eye or fingerprint, located via their smartphone,

and able to shop without queuing up at a checkout.

Imagine strolling into your local supermarket, popping your essentials into a basket, heading to the bagging area - where no items are unexpected - and walking out with your weekly shop.

There is no need to make a payment, no fiddling with coins, and no placement of a debit or credit card in a terminal. In fact, there is no till at all.

This is not casual shoplifting but a realistic prospect of the future way to pay - when technology recognises your presence, scans your shopping, and invisibly takes payment from your account.

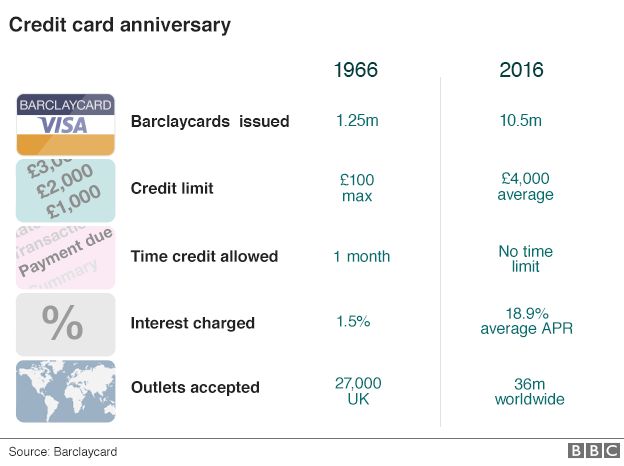

Amer Sajed, the chief executive of Barclaycard, says it will spell the steady demise of the physical plastic credit card, which his company introduced to the UK 50 years ago.

"People will be able to seamlessly shop going between the web, an app or in store," he says.

It will also create a battle for control of your digital wallet between banks and technology companies, as well as prompt debate over our privacy and security.

Image copyrightBarclaycardImage caption Barclaycard launched in 1966. It has left some with a debt hangover Credit cards have evolved since 1966, but the basic procedure of payment has remained the same. A card is either handed over, or the number on it is read out or entered into a machine.

All that requires the existence of a plastic card, but Mr Sajed says this is being replaced by wearable items.

At a display for Barclaycard staff, he shows off a plastic ring, a bracelet and a keychain which all contain a chip allowing the shopper to make payments on credit.

This, he says, is just a bridge to technology that will see customers identified by their eye or fingerprint, located via their smartphone, and able to shop without queuing up at a checkout.

Although cash, cheques and indeed cards will remain an option for shoppers, he says, these new ways of paying will take a growing share of the payments market in 10 years' time.

Image caption Some of the wearable devices may not suit everyone's sense of fashion Such a prospect sounds frightening for anyone who already has concerns about corporations, and potentially hackers, tracking our whereabouts or spending habits.

Mr Sajed argues that nothing will be done without permission.

"We would never track anyone's location or data without their express knowledge. and it would only be for things that the customer has allowed us to do."

There is an extra benefit, he says, as it is much easier to authorise a transaction when a card company knows a customer's location. It is easier to stop fraud for the same reason.

A link in the background between the individual and the payment system is required for any of this to work. This already happens with shopping portals like Amazon and services such as Uber allowing a single-click transaction because bank or credit card details are loaded when the customer first signs up.

"These emerging technologies still use the existing, underlying rails of the card payments system," says Richard Koch, head of policy at the UK Cards Association

As this digital market becomes more prevalent, and the technology advances, there will be a battle among banks, payment providers and others for their product to be used.

The UK Cards Association predicts there will be almost 21 billion "card" transactions in the UK in 2025, up from 12.6 billion last year. Of these, 3.6 billion will be credit card purchases compared with 2.5 billion last year.

Barclaycard clearly wants customers to use its services, but is credit the best option for day-to-day purchases?

Image copyrightPAImage caption Are the days of the plastic credit card numbered? Charities say that there is a danger in using credit cards, loans or overdrafts for everyday spending as this can easily spiral out of control.

The UK Cards Association says that 80% of credit card spending is by those who repay their balance in full the following month without incurring any interest.

Yet the StepChange debt charity says its concern is with the 1.6 million people repeatedly making only the minimum repayments each month and so face growing debt.

"The way that credit products are designed can create such disconnects. An obvious example of this is just making minimum repayments on credit cards which can give a false sense of security and a sense that the debt is being well managed, whereas the balance and repayment period are both growing," says the charity's head of policy, Peter Tutton.

"All too often credit cards stop being the short-term borrowing they are designed to be and become long-term and expensive debts."

Barclaycard's Mr Sajed says: "What we are not trying to do is get customers in debt. Debt is short-term and you should use it for whenever you need to but you should be able to pay it off."

Many consumers turn to their credit cards for major purchases owing to the extra protection they offer if something goes wrong. Credit card suppliers have also tried to encourage regular spending with the offer of loyalty points and other rewards.

Feeling the pinch

Despite this growth, there are pressures facing the credit card sector.

New European rules have capped the cost of so-called interchange fees - which retailers pay to their banks to process card payments.

As a result of the squeeze, many credit card providers have reduced the generosity of their rewards programmes, and increased charges elsewhere.

The UK Cards Association says the long-term effect of this is difficult to judge, but - with a revolution in the way we pay for things - the future will hold many more unknowns for the credit card industry.

Impressive blog and you have shared here information about credit card. as we provide card generator at affordable prices. for more info visit our website.

I recently came across your blog and have been reading along. I thought I would leave my first comment. I don't know what to say except that I have enjoyed reading. Nice blog. I will keep visiting this blog very often free psn codes

If you want to buy a home in a rural area you can take a USDA loan. This loan lets you buy a house with nothing down and low mortgage rates. You can take USDA loans even with a low credit score.

The next thing you need to do is to decide upon the basic equipments required. You can carry out this process by inquiring your merchant regarding the modes of payments. Basically, you need to ask him/her the method by which they receive their sales. How to Sell Credit Card Processing

As a Partner and Co-Founder of Predictiv and PredictivAsia, Jon specializes in management performance and organizational effectiveness for both domestic and international clients. He is an editor and author whose works include Invisible Advantage: How Intangilbles are Driving Business Performance. Learn more...

Can ease of extending and using credit overcome the presumption of security and financial probity? JL

Can ease of extending and using credit overcome the presumption of security and financial probity? JLImage copyright Barclaycard

Image copyright PA

5 comments:

Impressive blog and you have shared here information about credit card. as we provide card generator at affordable prices. for more info visit our website.

hi,

I have checked so many website, your website is very amazing. you should try this

website

I recently came across your blog and have been reading along. I thought I would leave my first comment. I don't know what to say except that I have enjoyed reading. Nice blog. I will keep visiting this blog very often free psn codes

If you want to buy a home in a rural area you can take a USDA loan. This loan lets you buy a house with nothing down and low mortgage rates. You can take USDA loans even with a low credit score.

The next thing you need to do is to decide upon the basic equipments required. You can carry out this process by inquiring your merchant regarding the modes of payments. Basically, you need to ask him/her the method by which they receive their sales. How to Sell Credit Card Processing

Post a Comment