How the Tech Sector Is Leaving the Rest of the US Economy In Its Dust

Historically, there comes a point at which the public - and their representatives - rebel at such concentrations of power.

The question is whether the combination of lower price and more convenience now delivered by tech giants will forestall that outcome this time. Or not. JL

Ben Popper reports in The Verge:

As these companies continue to scale, the network effects bolstering

their business are strengthening. Facebook and Google accounted for

three-quarters of the growth in digital advertising , leaving the rest to be divided among Twitter, Snapchat, and the entire American media industry. Apple and Alphabet have a duopoly on mobile operating systems. The S&P 500 is up

over $1.5 trillion since the start of 2017. Apple, Alphabet, Facebook,

Amazon, and Microsoft make up 37% of the total gains.

When Donald Trump was elected president last November, share prices for America’s big banks and construction firms rose sharply. The bet was that the Trump administration would deregulate the financial sector and approve a massive infrastructure bill. Prices in commodities like steel and copper ticked up in anticipation. Six months later, little of this Trump Trade has come to fruition. The Republican majority is still working to pass a health care bill, and no deregulation, tax reform, or infrastructure spending are in sight.

But that hasn’t slowed the stock market. The S&P 500 closed at a record high yesterday afternoon, and is up over $1.5 trillion since the start of 2017. And the companies doing the most to drive that rally are all tech firms. Apple, Alphabet, Facebook, Amazon, and Microsoft make up a whopping 37 percent of the total gains.

All of these companies saw their share prices touch record highs in recent months. This is in stark contrast to the rest of the US economy, which grew at a rate of less than 1 percent during the first three months of this year. That divide is the culmination of a long-term trend, according to a recent report featured in The Wall Street Journal:

In digital industries—technology, communications, media, software, finance and professional services—productivity grew 2.7% annually over the past 15 years...The slowdown is concentrated in physical industries—health care, transportation, education, manufacturing, retail—where productivity grew a mere 0.7% annually over the same period.

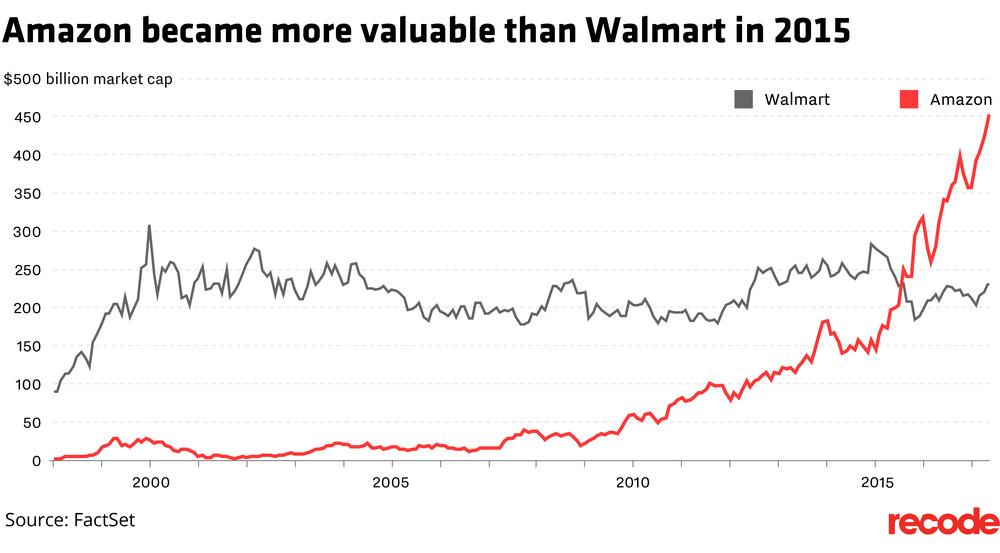

Here’s a dramatic illustration of that trend, in the form of a handy chart from this Recode story on Amazon’s recent success. It took Amazon 15 years to match the market capitalization of Walmart. Two years later, it is worth more than double its biggest rival. And while Amazon’s share price is hitting all-time highs, the rest of the retail sector is gasping for air.

Another example, this time from the education sector, is Google’s venture into the classroom back in 2012. In the five years since it has spread to more than half the primary and secondary schools in the US. Here’s Hal Friedlander, former chief information officer for the New York City Department of Education, the nation’s largest school district, talking to The New York Times: “Between the fall of 2012 and now, Google went from an interesting possibility to the dominant way that schools around the country teach students to find information, create documents and turn them in. Google established itself as a fact in schools.”

There is no industry where these players aren’t competing. Music, movies, shipping, delivery, transportation, energy — the list goes on and on.

As these companies continue to scale, the network effects bolstering their business are strengthening. Facebook and Google accounted for over three-quarters of the growth in the digital advertising industry in 2016, leaving the rest to be divided among small fry like Twitter, Snapchat, and the entire American media industry. Meanwhile Apple and Alphabet have achieved a virtual duopoly on mobile operating systems, with only a tiny sliver of consumers choosing an alternative for their smartphones and tablets.

In another era, Google dominance in search, Facebook’s commanding lead in social, or Amazon’s massive reach in e-commerce might lead regulators to view them as a monopoly. There has been some pushback in Europe, but so far US watchdogs haven’t taken any aggressive action. In part that’s because companies born during or after the dot-com days saw what happened to Microsoft. They found ways to soften their image and avoid the kind of sharp-elbowed competition that might draw the wrong kind of attention. But it’s also because these companies don’t resemble the monopolies our laws were designed to prevent.

Writing in the Yale Law Journal earlier this year, Lina Kahn argued that “the current framework in antitrust—specifically its pegging competition to ‘consumer welfare,’ defined as short-term price effects—is unequipped to capture the architecture of market power in the modern economy.” How do you measure the impact, positive or negative, to the average consumer when products like search and social media are given away for free, and the cost of switching to a new platform is just a few clicks? How do you make the case against Amazon when it drives costs down for consumers and has, over the years, produced little to no profit for itself?

By positioning themselves as the platforms on top of which information technology across every sector now runs, these titans of tech become the new centers of gravity for our economy, growing in size, scope, and influence while everyone else struggles not to fall too far behind. Meanwhile, Silicon Valley tries to convince the rest of America that it’s not coming for their jobs.

As a Partner and Co-Founder of Predictiv and PredictivAsia, Jon specializes in management performance and organizational effectiveness for both domestic and international clients. He is an editor and author whose works include Invisible Advantage: How Intangilbles are Driving Business Performance. Learn more...

Another example, this time from the education sector, is Google’s venture into the classroom back in 2012. In the five years since it has spread to more than half the primary and secondary schools in the US. Here’s Hal Friedlander, former chief information officer for the New York City Department of Education, the nation’s largest school district, talking to The New York Times: “Between the fall of 2012 and now, Google went from an interesting possibility to the dominant way that schools around the country teach students to find information, create documents and turn them in. Google established itself as a fact in schools.”There is no industry where these players aren’t competing. Music, movies, shipping, delivery, transportation, energy — the list goes on and on.As these companies continue to scale, the network effects bolstering their business are strengthening. Facebook and Google accounted for over three-quarters of the growth in the digital advertising industry in 2016, leaving the rest to be divided among small fry like Twitter, Snapchat, and the entire American media industry. Meanwhile Apple and Alphabet have achieved a virtual duopoly on mobile operating systems, with only a tiny sliver of consumers choosing an alternative for their smartphones and tablets.

Another example, this time from the education sector, is Google’s venture into the classroom back in 2012. In the five years since it has spread to more than half the primary and secondary schools in the US. Here’s Hal Friedlander, former chief information officer for the New York City Department of Education, the nation’s largest school district, talking to The New York Times: “Between the fall of 2012 and now, Google went from an interesting possibility to the dominant way that schools around the country teach students to find information, create documents and turn them in. Google established itself as a fact in schools.”There is no industry where these players aren’t competing. Music, movies, shipping, delivery, transportation, energy — the list goes on and on.As these companies continue to scale, the network effects bolstering their business are strengthening. Facebook and Google accounted for over three-quarters of the growth in the digital advertising industry in 2016, leaving the rest to be divided among small fry like Twitter, Snapchat, and the entire American media industry. Meanwhile Apple and Alphabet have achieved a virtual duopoly on mobile operating systems, with only a tiny sliver of consumers choosing an alternative for their smartphones and tablets./cdn0.vox-cdn.com/uploads/chorus_asset/file/8521591/Screen_Shot_2017_05_15_at_2.05.08_PM.png) In another era, Google dominance in search, Facebook’s commanding lead in social, or Amazon’s massive reach in e-commerce might lead regulators to view them as a monopoly. There has been some pushback in Europe, but so far US watchdogs haven’t taken any aggressive action. In part that’s because companies born during or after the dot-com days saw what happened to Microsoft. They found ways to soften their image and avoid the kind of sharp-elbowed competition that might draw the wrong kind of attention. But it’s also because these companies don’t resemble the monopolies our laws were designed to prevent.Writing in the Yale Law Journal earlier this year, Lina Kahn argued that “the current framework in antitrust—specifically its pegging competition to ‘consumer welfare,’ defined as short-term price effects—is unequipped to capture the architecture of market power in the modern economy.” How do you measure the impact, positive or negative, to the average consumer when products like search and social media are given away for free, and the cost of switching to a new platform is just a few clicks? How do you make the case against Amazon when it drives costs down for consumers and has, over the years, produced little to no profit for itself?By positioning themselves as the platforms on top of which information technology across every sector now runs, these titans of tech become the new centers of gravity for our economy, growing in size, scope, and influence while everyone else struggles not to fall too far behind. Meanwhile, Silicon Valley tries to convince the rest of America that it’s not coming for their jobs.

In another era, Google dominance in search, Facebook’s commanding lead in social, or Amazon’s massive reach in e-commerce might lead regulators to view them as a monopoly. There has been some pushback in Europe, but so far US watchdogs haven’t taken any aggressive action. In part that’s because companies born during or after the dot-com days saw what happened to Microsoft. They found ways to soften their image and avoid the kind of sharp-elbowed competition that might draw the wrong kind of attention. But it’s also because these companies don’t resemble the monopolies our laws were designed to prevent.Writing in the Yale Law Journal earlier this year, Lina Kahn argued that “the current framework in antitrust—specifically its pegging competition to ‘consumer welfare,’ defined as short-term price effects—is unequipped to capture the architecture of market power in the modern economy.” How do you measure the impact, positive or negative, to the average consumer when products like search and social media are given away for free, and the cost of switching to a new platform is just a few clicks? How do you make the case against Amazon when it drives costs down for consumers and has, over the years, produced little to no profit for itself?By positioning themselves as the platforms on top of which information technology across every sector now runs, these titans of tech become the new centers of gravity for our economy, growing in size, scope, and influence while everyone else struggles not to fall too far behind. Meanwhile, Silicon Valley tries to convince the rest of America that it’s not coming for their jobs.

0 comments:

Post a Comment