Why Bitcoin is Actually Worth Somewhere Between $20 and $800,000

The point is that precision matters less than thought process and underlying principles. JL

Lionel Laurent reports in Bloomberg:

What’s the value of a cryptocurrency

made of code with no country enforcing it, no central bank controlling

it, and few places to spend it? Is it $2, $20,000, or $2 million? Can

one try to grasp at rational analysis? How can something be worth $20, $600, and $15,000 within the same

theory? One key reason stems from what we don’t know than what we do know. Those with long memories remember the quantitative analyses that

underpinned the hot new asset classes of the past, from dot-com stocks

to securitized art. It means science and snake oil, side by side. It took two economists one three-course meal and two bottles of wine to calculate the fair value of one Bitcoin: $200.

It took an extra day for them to realize they were one decimal place out: $20, they decided, was the right price for a virtual currency that was worth $1,200 a year ago, flirted with $20,000 in December, and is still around $8,000. Setting aside the fortunes lost on it this year, Bitcoin, by their calculation, is still overvalued, to the tune of about 40,000 percent. The pair named this the Côtes du Rhône theory, after the wine they were drinking.

“It’s how we get our best ideas. It’s the lubricant,” says Savvas Savouri, a partner at a London hedge fund who shared drinking and thinking duties that night with Richard Jackman, professor emeritus at the London School of Economics. Their quest is one shared by the legions of traders, techies, online scribblers, and gamblers and grifters mesmerized by Bitcoin. What’s the value of a cryptocurrency made of code with no country enforcing it, no central bank controlling it, and few places to spend it? Is it $2, $20,000, or $2 million? Can one try to grasp at rational analysis, or is this just the madness of crowds?

Answering this question isn’t easy: Buying Bitcoin won’t net you any cash flows, or any ownership of the blockchain technology underpinning it, or really anything much at all beyond the ability to spend or save it. Maybe that’s why Warren Buffett once said the idea that Bitcoin had “huge intrinsic value” was a “joke”—there’s no earnings potential that can be used to estimate its value. But with $2 billion pumped into cryptocurrency hedge funds last year, there’s a lot of money betting the punchline is something other than zero. If Bitcoin is a currency, and currencies have value, surely some kind of stab—even in the dark—should be made at gauging its worth.

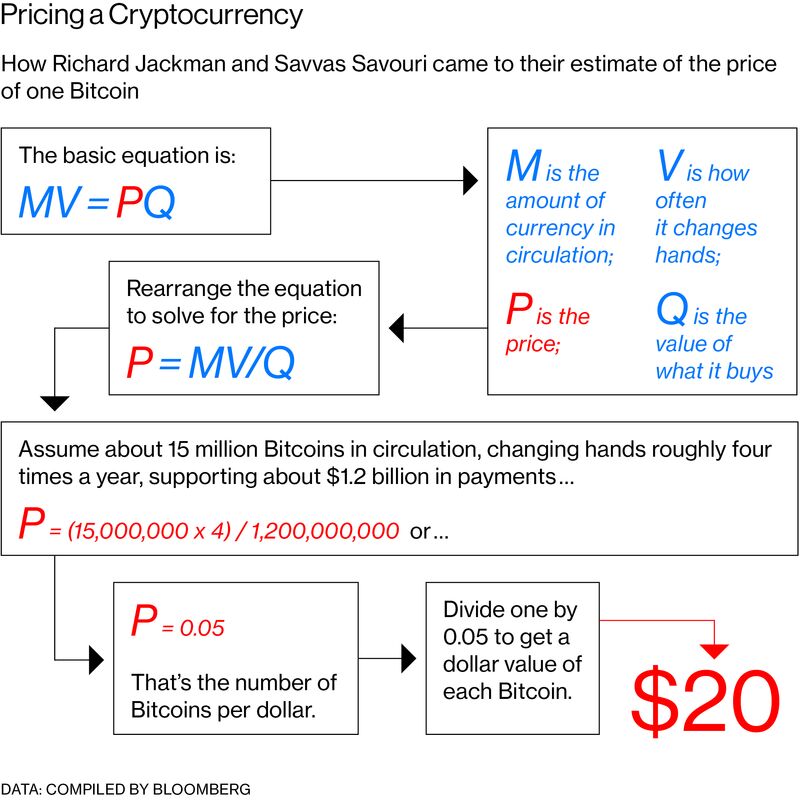

Writing on a tablecloth, Jackman and Savouri turned to the quantity theory of money. Formalized by Irving Fisher in 1911, with origins that go back to Copernicus’s work on the effects of debasing coinage, the theory holds that the price of money is linked to its supply and how often it’s used.

Here’s how it works. By knowing a money’s total supply, its velocity—the rate at which people use each coin—and the amount of goods and services on which it’s spent, you should be able to calculate price. Estimating Bitcoin’s supply at about 15 million coins (it’s currently a bit more), and assuming each one is used an average of about four times a year, led Jackman and Savouri to calculate that 60 million Bitcoin payments were supporting their assumed $1.2 billion worth of total U.S. dollar-denominated purchases. Using the theory popularized by Fisher and his followers, you can—simplifying things somewhat—divide the $1.2 billion by the 60 million Bitcoin payments to get the price of Bitcoin in dollars.

That’s $20.

So far, so straightforward. It turns out, however, that when it comes to putting a price on Bitcoin, the same equation can yield many different answers. In September, Dan Davies, an analyst at financial research firm Frontline Analysts Ltd., wrote up a “guesstimate” of Bitcoin’s value that he’d originally conducted in 2014 using—again—the quantity theory of money. He plugged in estimates for each variable and got about $600.

On Dec. 10, Mark Kirker, a high school math teacher in California, published an analysis online using the same equation for the same purpose. He concluded that Bitcoin should be way above then-current levels. He’s since revised the number. Contacted by Bloomberg, he says it could be $15,000.

How can something be worth $20, $600, and $15,000 within the same theory? One key reason stems from what we don’t know about cryptocurrencies rather than what we do know. We know Bitcoin’s maximum supply is 21 million, and we know the velocity of most commonly used currencies. We don’t know how widely Bitcoin will be adopted tomorrow, how frequently it will transact, or what it will be used for. In Davies’s example, a guide to Bitcoin’s future potential was the illicit drugs market, an obvious home for more-or-less-untraceable digital cash. The United Nations has estimated this market at $120 billion. Plugging in that number helped Davies get to $600.

For Kirker, though, drugs and criminals are only part of the story. He imagines including the output of some developing countries where cryptocurrencies might have better takeup than traditional banking. But with so much up in the air, the equation starts to look less like algebra and more like alchemy. Even in the non-Bitcoin world, the velocity of money and its price can fluctuate in ways not predicted by fundamental analysis. “I am not wholly surprised it doesn’t pin down a price target to within a factor of 100 either way,” Davies says.

Some believe the cloud of confusion has to do with the simple fact that cryptocurrency is something entirely new—it needs a fresh school of economic thinking to go with it. A quantity theory of cryptomoney, perhaps.

John Pfeffer, formerly a partner at KKR & Co., has written several papers to this effect, arguing that technology is turning the centuries-old equation on its head. Bandwidth and computing resources are the fuel of cryptocurrencies, and they need their place in quantity theory, he argues. His version of the equation imagines a world in which more powerful computers and faster connection speeds combine to lower the cost of maintaining a crypto-economy over time, while the same forces radically increase the availability and speed of its digital coins. There already exist hundreds of tokens other than Bitcoin, pointing to a world where digital currencies are, well, a dime a dozen.

In a future where cryptocurrencies become a form of economic resource (like fuel, water, or electricity) that’s computerized and commoditized, would anyone get rich from hoarding them in her trading account? No, says Pfeffer. In his view, the more widely used a particular brand of digital cash becomes, the higher the probability its value tends toward zero. In quantity theory terms, cryptocoins’ velocity could go way, way up, while the cost of many services within the crypto-economy could go way, way down. Crypto could change the world and still leave a lot of people with worthless tokens.

Pfeffer dangles one hope in front of the Bitcoin faithful who dream of riches: the possibility there’s one cryptocurrency out there that will serve as a store of value for the digital world. Like gold, a metal seen by investors as a haven in times of crisis or when the purchasing power of cash is eroding, whichever coin wins that crown will have a completely different use—and price—than the rest. Applying this thinking to Bitcoin, Pfeffer explains, would yield a price target of $260,000 to $800,000.

Such a value would be not too far off $1 million—where the frequently mocked, frizzy-haired self-help guru James Altucher expects Bitcoin to be in 2020. Software entrepreneur John McAfee has said it will hit $500,000. “If not, I will eat my d--- on national television,” he tweeted. He later doubled his target price. Pfeffer has been more careful than most in warning of significant risk of investment loss. “This could all go substantially to zero for various reasons,” he wrote in December.

Putting a price on Bitcoin is therefore less about crunching numbers and more about deciding just what it is and what it could be, if anything. That’s appetizing for risk-hungry optimists in the venture capital world, who are accustomed to their investments turning into big hits or big flops. Ride-hailing service Uber Technologies Inc., for example, has lost an eye-watering amount of money, yet it’s one of the most highly valued companies in the world. It’s a bet that more traditional investors would have difficulty justifying using traditional metrics.

But it also means science and snake oil sit side by side. Quantity theory is one example of how an equation can be remodeled to fit different scenarios or different wishes about where the price will land. And it’s not the only one: Network adoption, the cost curve of Bitcoin mining, and transaction volumes have all been bundled into marketable literature advising traders and investors on what to buy. It’s a thick numbers soup. At least Uber has financial accounts to review.

Those with long memories also remember the quantitative analyses that underpinned the hot new asset classes of the past, from dot-com stocks to securitized art. These were often sold to investors as new metrics and radical investment theses, only to be ditched when a recession or panicked sell-off hit. “They’re always talking about a new paradigm, but I say it’s the same meat, different gravy,” says Côtes du Rhône theorist Savouri, who maintains traditional economic theory should be embraced rather than ignored by the Bitcoin faithful.

For Savouri, the easiest way to understand the efflorescence of theories and valuations being bandied about is to opt for a simple, overarching one: the greater fool theory. It says that one fool buys in the hope that there’s an ever-bigger sucker willing to pay more. “The problem,” he says, “is that we don’t breed fools geometrically.”

As a Partner and Co-Founder of Predictiv and PredictivAsia, Jon specializes in management performance and organizational effectiveness for both domestic and international clients. He is an editor and author whose works include Invisible Advantage: How Intangilbles are Driving Business Performance. Learn more...

0 comments:

Post a Comment