Americans have more payment options than others in the world, they are accustomed to them - and they trust them. But younger age groups are starting to experiment. JL

ColbySmith reports in FT Alphaville:

A third of the time, Americans use cash to pay.

Debit cards are next (26% of all

purchases), followed by credit cards at 21%. Electronic payments disappoint with only 8.9%. That's nearly the same level as cheques (which they) use for 10% of payments. Americans use cash for smaller payments, cards and cheques for larger ones. Security is a major concern. Urgency matters, too. (But) “the pick-up in digital payments really depends on who holds the money.” And soon it'll be those age groups who've never known a world without smartphones. We've been hearing for years that the world is going “cashless.” This reality does not appear remote. For instance, Sweden has seen a 50 per cent of decrease in the use of cash over the past decade. But America is not Sweden — stateside cash is still king, at least for now.

According to a recent study by the Federal Reserve Banks of Atlanta, Boston, Richmond and San Francisco, US consumers like their paper and plastic. About a third of the time, Americans use cash to pay for things. Debit cards are the next favourite (used in roughly 26 per cent of all purchases), followed closely by credit cards at 21 per cent. The supposed wave of the future — electronic payments — disappoint with only an 8.9 per cent share. That's nearly the same level as one of the most antiquated ways to pay: cheques. Per the new World Payments Report by Capgemini, Americans use them for 10 per cent of payments, just five percentage points less than levels in 2012.

Americans tend to use cash for smaller payments, and cards and cheques for larger ones. Here's a chart from the Fed study showing both the number of transactions per month and the average amount per transaction (“OBBP” stands for online banking bill pay, “BANP” means bank account number payment and “Other” includes PayPal, account-to-account transfers, mobile payments and deductions from incomes):

Overtime, the demand for cash, as measured by the number of notes in circulation, has remained not only robust, but trending upward at a 7.4 per cent annual growth rate, according to the San Francisco Fed.

There are numerous reasons why the US has been slow to pick up on using a smartphone to pay for things. Security is a major concern. Urgency matters, too. Digital payments have become enormously popular in places such as China because unlike America, few adequate services for online purchases existed.

A massive overhaul of consumer behaviour looks unlikely any time soon, but Haim Israel at Bank of America Merrill Lynch says the demographics are becoming more favourable for digital payments.

While the San Francisco Fed does find that younger Americans use cash with more or less the same frequency as older folks, BofA's Israel points out that millennials (born 1981-96) and their younger cohort Generation Z, are far more willing to try out Venmo, PayPal, Zelle and other mobile payment providers. In fact, these age groups are three times as likely to use these platforms than the baby boomer generation. It's for this reason that the mobile banking penetration for Generation Z dwarfs that of the US average by more than two-fold.

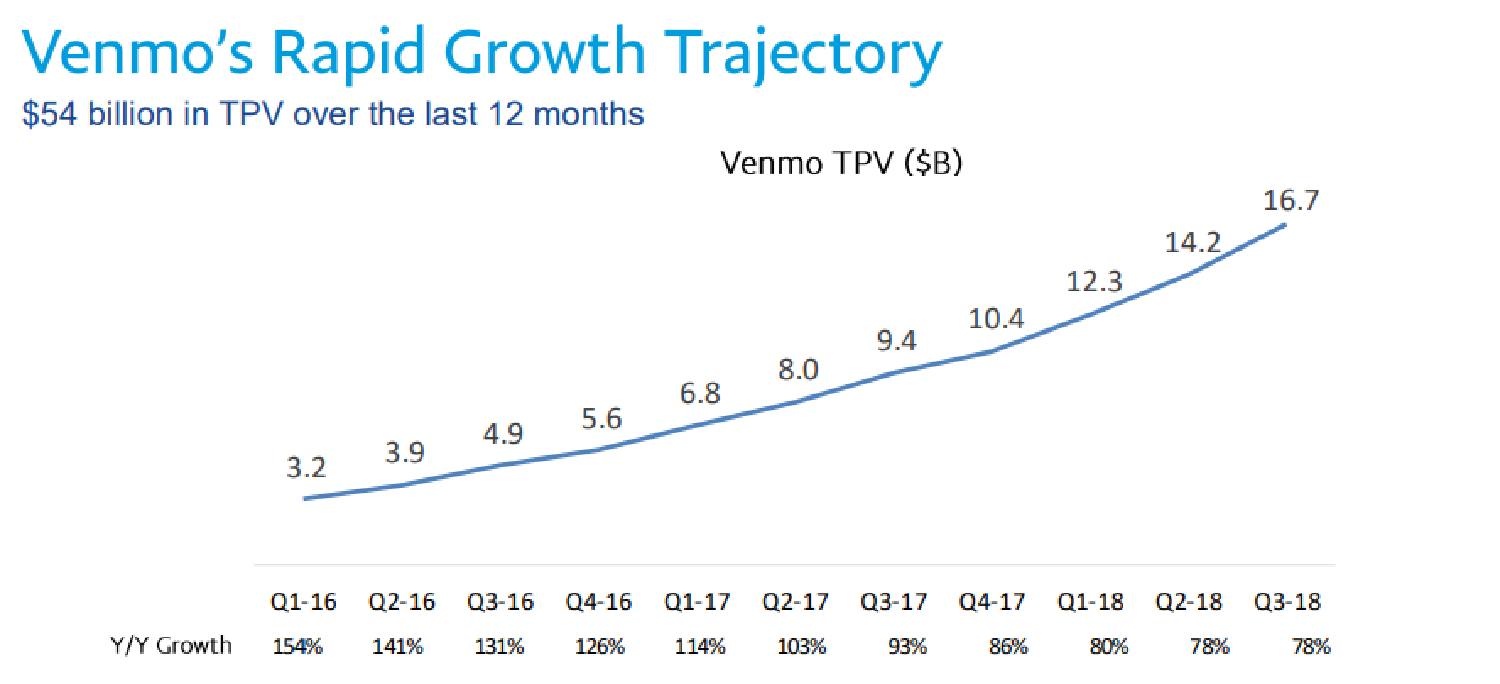

This shift is starting to crop up in the data for some of the leading digital payment companies. Venmo, which is owned by PayPal and allows users to transfer funds between linked accounts or cards via smartphones, saw its total payments volume for the third quarter surge 78 per cent from the year before to $16.7bn. That's up from just $3.2bn two years earlier. Here's a chart from its most recent third-quarter earnings presentation:

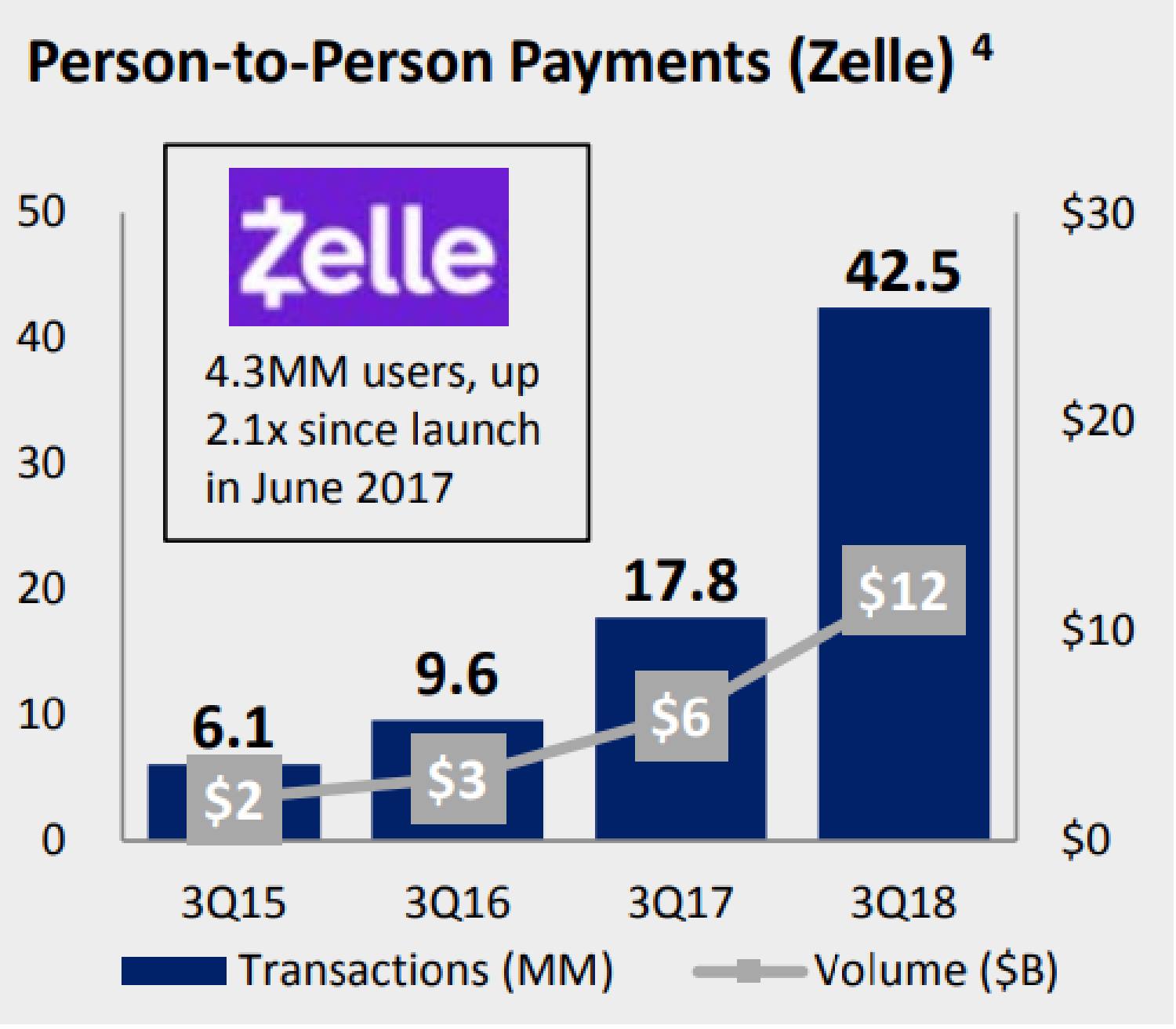

The same is true for Zelle, which is a mobile application launched by the country's largest banks in 2017 that enables account holders to instantly pay one another. On the most recent earnings call, BofA touted the fact that its customers transacted about $12bn worth of payments using Zelle last quarter, double the volume from the previous year:

These numbers are large because they come from such a small base. That being said, “the pick-up in digital payments really depends on who holds the money,” adds Israel.

And soon, he says, it'll be those age groups who've never known a world without smartphones.

As a Partner and Co-Founder of Predictiv and PredictivAsia, Jon specializes in management performance and organizational effectiveness for both domestic and international clients. He is an editor and author whose works include Invisible Advantage: How Intangilbles are Driving Business Performance. Learn more...

0 comments:

Post a Comment