Does the Red Hat Acquisition Really Change IBM's Strategic Position?

They are very late to the open source party. And that could be ok, but for the fact that three of the most important cloud providers to whom they want to the be the customer link are capable of offering that service themselves. JL

Ben Thompson reports in Stratechery:

Gerstner got IBM turned around in three years. (He) talked to customers and found they didn’t actually

like any of his products. “So why are you buying from IBM?” The

customers (replied): “IBM is the only company with an office

everywhere we do business.” Gerstner understood he wasn’t selling products he was selling a service. IBM is betting it can again provide the solution, combining with Red

Hat to build products that will bridge private data centers

and public clouds. The problem is they are building on top of three cloud providers (including Amazon, Google, Microsoft). The best way to understand how it is Red Hat built a multi-billion dollar business off of open source software is to start with IBM. Founder Bob Young explained at the All Things Open conference in 2014:

There is no magic bullet to it. It is a lot of hard work staying up with your customers and understanding and thinking through where are the opportunities. What are other suppliers in the market not doing for those customers that you can do better for them? One of the great examples to give you an idea of what inspired us very early on, and by very early on we’re talking Mark Ewing and I doing not enough business to pay the rent on our apartments, but yet we were paying attention to [Lou Gerstner and] IBM…

Gerstner came into IBM and got it turned around in three years. It was miraculous…Gerstner’s insight was he went around and talked to a whole bunch IBM customers and found out that the customers didn’t actually like any of his products. They were ok, but whenever he would sit down with any given customer there was always someone who did that product better than IBM did…He said, “So why are you buying from IBM?” The customers were saying “IBM is the only technology company with an office everywhere that we do business,” and as a result Gerstner understood that he wasn’t selling products he was selling a service.

He talked about that publicly, and so at Red Hat we go, “OK, we don’t have a product to sell because ours is open source and everyone can use our innovations as quickly as we can, so we’re not really selling a product, but Gerstner at IBM is telling us the customers don’t buy products, they buy services, things that make themselves more successful.” And so that was one of our early insights into what we were doing was this idea that we were actually in the services business, even back when we were selling shrink-wrapped boxes of Linux, we saw that as an interim step to getting us big enough that we could sign service contracts with real customers.

Young’s story came full circle when IBM bought Red Hat for $34 billion, a 60% premium over Red Hat’s Friday closing price. IBM is hoping it too to can come full circle: recapture Gerstner’s magic, which depended not only on his insight about services, but also a secular shift in enterprise computing.

How Gerstner Transformed IBM

I’ve written previously about Gerstner’s IBM turnaround in the context of Satya Nadella’s attempt to do the same at Microsoft, and Gerstner’s insight that while culture is extremely difficult to change, it is impossible to change nature. From Microsoft’s Monopoly Hangover:

The great thing about a monopoly is that a company can do anything, because there is no competition; the bad thing is that when the monopoly is finished the company is still capable of doing anything at a mediocre level, but nothing at a high one because it has become fat and lazy. To put it another way, for a former monopoly “big” is the only truly differentiated asset. This was Gerstner’s key insight when it came to mapping out IBM’s future…In Gerstner’s vision, only IBM had the breadth to deliver solutions instead of products.

A strategy predicated on providing solutions, though, needs a problem, and the other thing that made Gerstner’s turnaround possible was the Internet. By the mid-1990s businesses were faced with a completely new set of technologies that were nominally similar to their IT projects of the last fifteen years, but in fact completely different. Gerstner described the problem/opportunity in Who Says Elephants Can’t Dance:

If the strategists were right, and the cloud really did become the locus of all this interaction, it would cause two revolutions — one in computing and one in business. It would change computing because it would shift the workloads from PCs and other so-called client devices to larger enterprise systems inside companies and to the cloud — the network — itself. This would reverse the trend that had made the PC the center of innovation and investment — with all the obvious implications for IT companies that had made their fortunes on PC technologies.

Far more important, the massive, global connectivity that the cloud depicted would create a revolution in the interactions among millions of businesses, schools, governments, and consumers. It would change commerce, education, health care, government services, and on and on. It would cause the biggest wave of business transformation since the introduction of digital data processing in the 1960s…Terms like “information superhighway” and “e-commerce” were insufficient to describe what we were talking about. We needed a vocabulary to help the industry, our customers, and even IBM employees understand that what we saw transcended access to digital information and online commerce. It would reshape every important kind of relationship and interaction among businesses and people. Eventually our marketing and Internet teams came forward with the term “e-business.”

Those of you my age or older surely remember what soon became IBM’s ubiquitous ‘e’:

IBM went on to spend over $5 billion marketing “e-business”, an investment Gerstner called “one of the finest jobs of brand positions I’ve seen in my career.” It worked because it was true: large enterprises, most of which had only ever interacted with customers indirectly through a long chain of wholesalers and distributors and retailers suddenly had the capability — the responsibility, even — of interacting with end users directly. This could be as simple as a website, or e-commerce, or customer support, not to mention the ability to tap into all of the other parts of the value chain in real-time. The technology challenges and the business possibilities — the problem set, if you will — were immense, and Gerstner positioned IBM as the company that could solve these new problems.

It was an attractive proposition for nearly all non-tech companies: the challenge with the Internet in the 1990s was that the underlying technologies were so varied and quite immature; different problem spaces had different companies hawking products, many of them startups with no experience working with large enterprises, and even if they had better products no IT department wanted to manage and integrate a multitude of vendors. IBM, on the other hand, offered the proverbial “one throat to choke”; they promised to solve all of the problems associated with this new-fangled Internet stuff, and besides, IT departments were familiar and comfortable with IBM.

It was also a strategy that made sense in its potential to squeeze profit out of the value chain:

The actual technologies underlying the Internet were open and commoditized, which meant IBM could form a point of integration and extract profits, which is exactly what happened: IBM’s revenue and growth increased steadily — often rapidly! — over the next decade, as the company managed everything from datacenters to internal networks to external websites to e-commerce operations to all the middleware that tied it together (made by IBM, naturally, which was where the company made most of its profits). IBM took care of everything, slowly locking its customers in, and once again grew fat and lazy.

When IBM Lost the Cloud

In the final paragraph of Who Says Elephants Can’t Dance? Gerstner wrote of his successor Sam Palmisano:

I was always an outsider. But that was my job. I know Sam Palmisano has an opportunity to make the connections to the past as I could never do. His challenge will be to make them without going backward; to know that the centrifugal forces that drove IBM to be inward-looking and self-absorbed still lie powerful in the company.

Palmisano failed miserably, and there is no greater example than his 2010 announcement of the company’s 2015 Roadmap, which was centered around a promise of delivering $20/share in profit by 2015. Palmisano said at the time:

[The consensus view is that] product cycles will drive industry growth. The industry is consolidating and at the end of the day consumer technology will obliterate all computer science over the last 20 years. I’m an East Coast guy. We’re going to have a slightly different view. Product cycles aren’t going to drive sustainable growth. Clients in the future will demand quantifiable returns on their investment. They are not going to buy fashion and trends. Enterprise will have its own unique model. You can’t do what we’re doing in a cloud.

Amazon Web Services, meanwhile, had launched a full four years and two months before Palmisano’s declaration; it was the height of folly to not simply mock the idea of the cloud, but to commit to a profit number in the face of an existential threat that was predicated on spending absolutely massive amounts of money on infrastructure.

Gerstner identified exactly what it was that Palmisano got wrong: he was “inward-looking and self-absorbed” such that he couldn’t imagine an enterprise solution better than IBM’s customized solutions. That, though, was to miss the point. As I wrote in a Daily Update back in 2014 when the company formally abandoned the 2015 profit goal:

The reality…is that the businesses IBM served — and the entire reason IBM had a market — didn’t buy customized technological solutions to make themselves feel good about themselves; they bought them because they helped them accomplish their business objectives. Gerstner’s key insight was that many companies had a problem that only IBM could solve, not that customized solutions were the end-all be-all. And so, as universally provided cloud services slowly but surely became good-enough, IBM no longer had a monopoly on problem solving.

The company has spent the years since then claiming it is committed to catching up in the public cloud, but the truth is that Palmisano sealed the company’s cloud fate when he failed to invest a decade ago; indeed, one of the most important takeaways from the Red Hat acquisition is the admission that IBM’s public cloud efforts are effectively dead.

IBM’s Struggles

So what precisely is the point of IBM acquiring Red Hat, and what if anything does it have to do with Lou Gerstner?

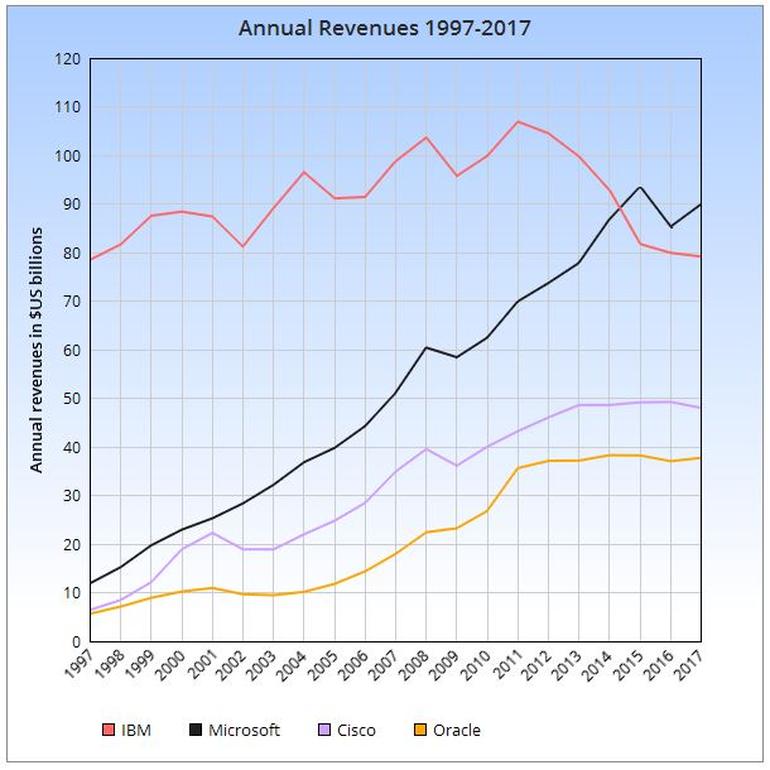

Well first off, IBM hasn’t been doing very well for quite some time now: last year’s annual revenue was the lowest since 1997, part-way through Gerstner’s transformation; of course, as this ZDNet article from whence this graph comes points out, $79 billion in 1997 is $120 billion today. From ZDNetThe company did finally return to growth earlier this year after 22 straight quarters of decline, only to decline again last quarter: IBM’s ancient mainframe business was up 2%, and its traditional services business, up 3%, but Technology Services and Cloud Platforms were flat, and Cognitive Solutions (i.e. Watson) was down 5%.

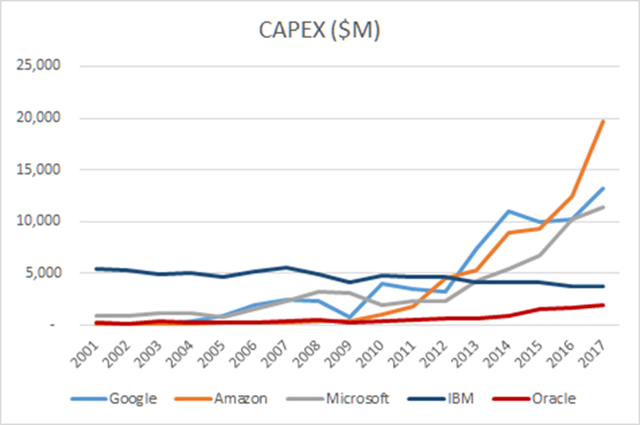

Meanwhile, the aformentioned commitment to the cloud has mostly been an accounting fiction derived from re-classifying existing businesses; the more pertinent number is the company’s capital expenditures, which in 2017 were $3.2 billion, down from 2016’s $3.6 billion. Charles Fitzgerald writes on Platformonomics:

We see IBM’s CAPEX slowly trailing off, like the company itself. IBM has always spent a lot on CAPEX (as high as $7 billion a year in their more glorious past), from well before the cloud era, so we can’t assume the absolute magnitude of spend is going towards the cloud. The big three all surpassed IBM’s CAPEX spend in 2012/13. In resisting the upward pull on CAPEX we see from all the other cloud vendors, IBM simply isn’t playing the hyper-scale cloud game.

The Red Hat Acquisition

This is where the Red Hat acquisition comes in: while IBM will certainly be happy to have the company’s cash-generating RHEL subscription business, the real prize is Openshift, a software suite for building and managing Kubernetes containers. I wrote about Kubernetes in 2016’s How Google is Challenging AWS:

In 2014 Google announced Kubernetes, an open-source container cluster manager based on Google’s internal Borg service that abstracts Google’s massive infrastructure such that any Google service can instantly access all of the computing power they need without worrying about the details. The central precept is containers, which I wrote about in 2014: engineers build on a standard interface that retains (nearly) full flexibility without needing to know anything about the underlying hardware or operating system (in this it’s an evolutionary step beyond virtual machines).

Where Kubernetes differs from Borg is that it is fully portable: it runs on AWS, it runs on Azure, it runs on the Google Cloud Platform, it runs on on-premise infrastructure, you can even run it in your house. More relevantly to this article, it is the perfect antidote to AWS’ ten year head-start in infrastructure-as-a-service: while Google has made great strides in its own infrastructure offerings, the potential impact of Kubernetes specifically and container-based development broadly is to make irrelevant which infrastructure provider you use. No wonder it is one of the fastest growing open-source projects of all time: there is no lock-in.

This acquisition brings together the best-in-class hybrid cloud providers and will enable companies to securely move all business applications to the cloud. Companies today are already using multiple clouds. However, research shows that 80 percent of business workloads have yet to move to the cloud, held back by the proprietary nature of today’s cloud market. This prevents portability of data and applications across multiple clouds, data security in a multi-cloud environment and consistent cloud management.

IBM and Red Hat will be strongly positioned to address this issue and accelerate hybrid multi-cloud adoption. Together, they will help clients create cloud-native business applications faster, drive greater portability and security of data and applications across multiple public and private clouds, all with consistent cloud management. In doing so, they will draw on their shared leadership in key technologies, such as Linux, containers, Kubernetes, multi-cloud management, and cloud management and automation.

This is the bet: while in the 1990s the complexity of the Internet made it difficult for businesses to go online, providing an opening for IBM to sell solutions, today IBM argues the reduction of cloud computing to three centralized providers makes businesses reluctant to commit to any one of them. IBM is betting it can again provide the solution, combining with Red Hat to build products that will seamlessly bridge private data centers and all of the public clouds.

IBM’s Unprepared Mind

The best thing going for this strategy is its pragmatism: IBM gave up its potential to compete in the public cloud a decade ago, faked it for the last five years, and now is finally admitting its best option is to build on top of everyone else’s clouds. That, though, gets at the strategy’s weakness: it seems more attuned to IBM’s needs than potential customers. After all, if an enterprise is concerned about lock-in, is IBM really a better option? And if the answer is that “Red Hat is open”, at what point do increasingly sophisticated businesses build it themselves?

The problem for IBM is that they are not building solutions for clueless IT departments bewildered by a dizzying array of open technologies: instead they are building on top of three cloud providers, one of which (Microsoft) is specializing in precisely the sort of hybrid solutions that IBM is targeting. The difference is that because Microsoft has actually spent the money on infrastructure their ability to extract money from the value chain is correspondingly higher; IBM has to pay rent:

Perhaps the bigger issue, though, goes back to Gerstner: before IBM could take advantage of the Internet, the company needed an overhaul of its culture; the extent to which the company will manage to leverage its acquisition of Red Hat will depend on a similar transformation. Unfortunately, that seems unlikely; current CEO Ginni Rometty, who took over the company at the beginning of 2012, not only supported Palmisano’s disastrous Roadmap 2015, she actually undertook most of the cuts and financial engineering necessary to make it happen, before finally giving up in 2014. Meanwhile the company’s most prominent marketing has been around Watson, the capabilities of which have been significantly oversold; it’s not a surprise sales are shrinking after disappointing rollouts.

Gerstner knew turnarounds were hard: he called the arrival of the Internet “lucky” in terms of his tenure at IBM. But, as the Louis Pasteur quote goes, “Fortune favors the prepared mind.” Gerstner had identified a strategy and begun to change the culture of IBM, so that when the problem arrived, the company was ready. Today IBM claims it has found a problem; it is an open question if the problem actually exists, but unfortunately there is even less evidence that IBM is truly ready to take advantage of it if it does.

As a Partner and Co-Founder of Predictiv and PredictivAsia, Jon specializes in management performance and organizational effectiveness for both domestic and international clients. He is an editor and author whose works include Invisible Advantage: How Intangilbles are Driving Business Performance. Learn more...

0 comments:

Post a Comment