But the primary point is that Amazon is reaping what it sows. JL

Benedict Evans reports in his blog:

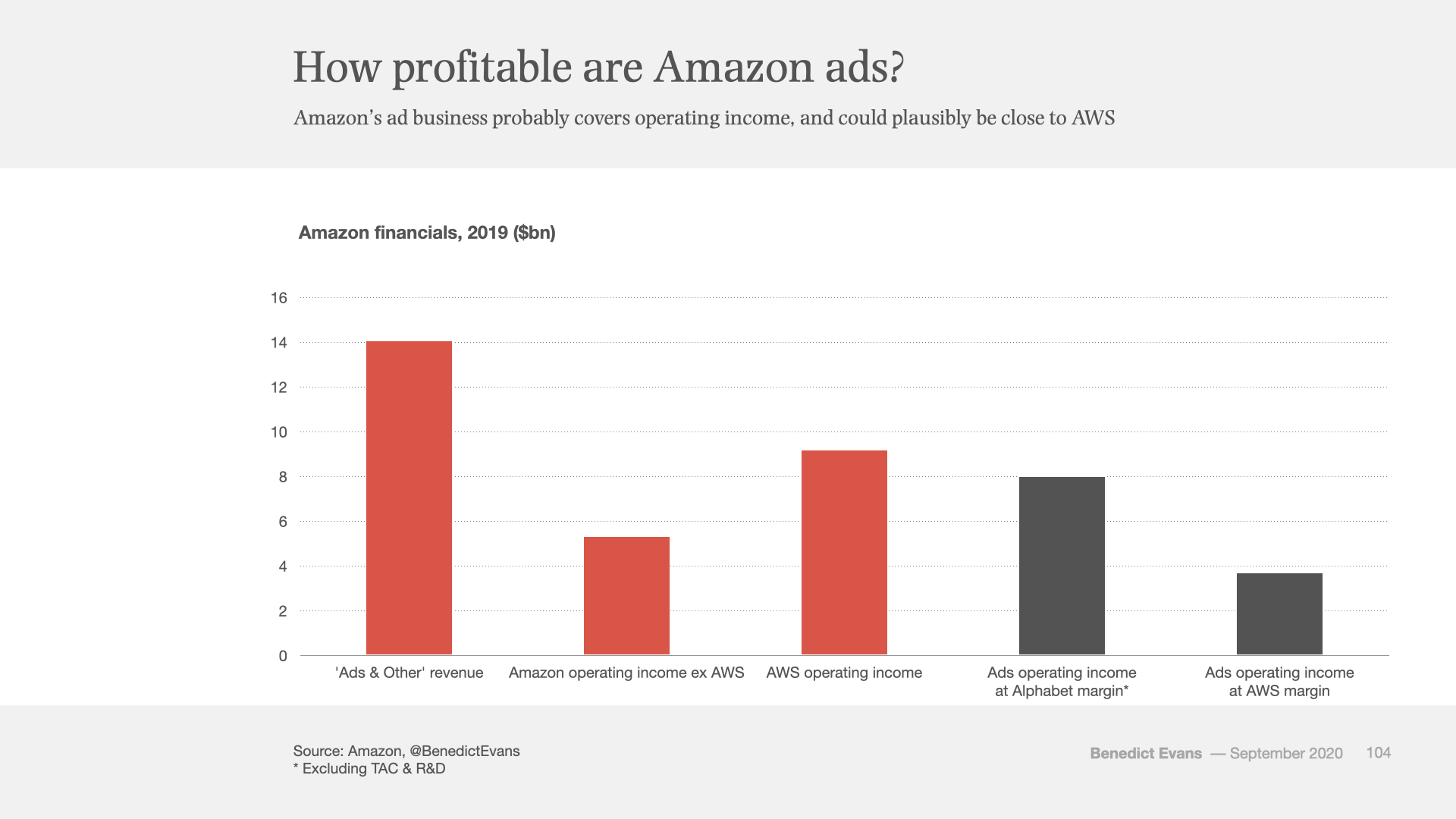

In 2015, Amazon had to start giving numbers (back to 2013), and we discovered it was hugely profitable. In 2015 and 2016 AWS was the great majority of Amazon’s reported operating income. That’s not true anymore - the US business is now generating substantial operating profit. Only the international business is losing money. The ad business is contributing as much operating income as everything apart from AWS, and it might be close to matching AWS. Jeff Bezos says he runs it for ‘trailing 12 months’ absolute free cashflow’, not net income, and it’s had positive cashflow since 2002.

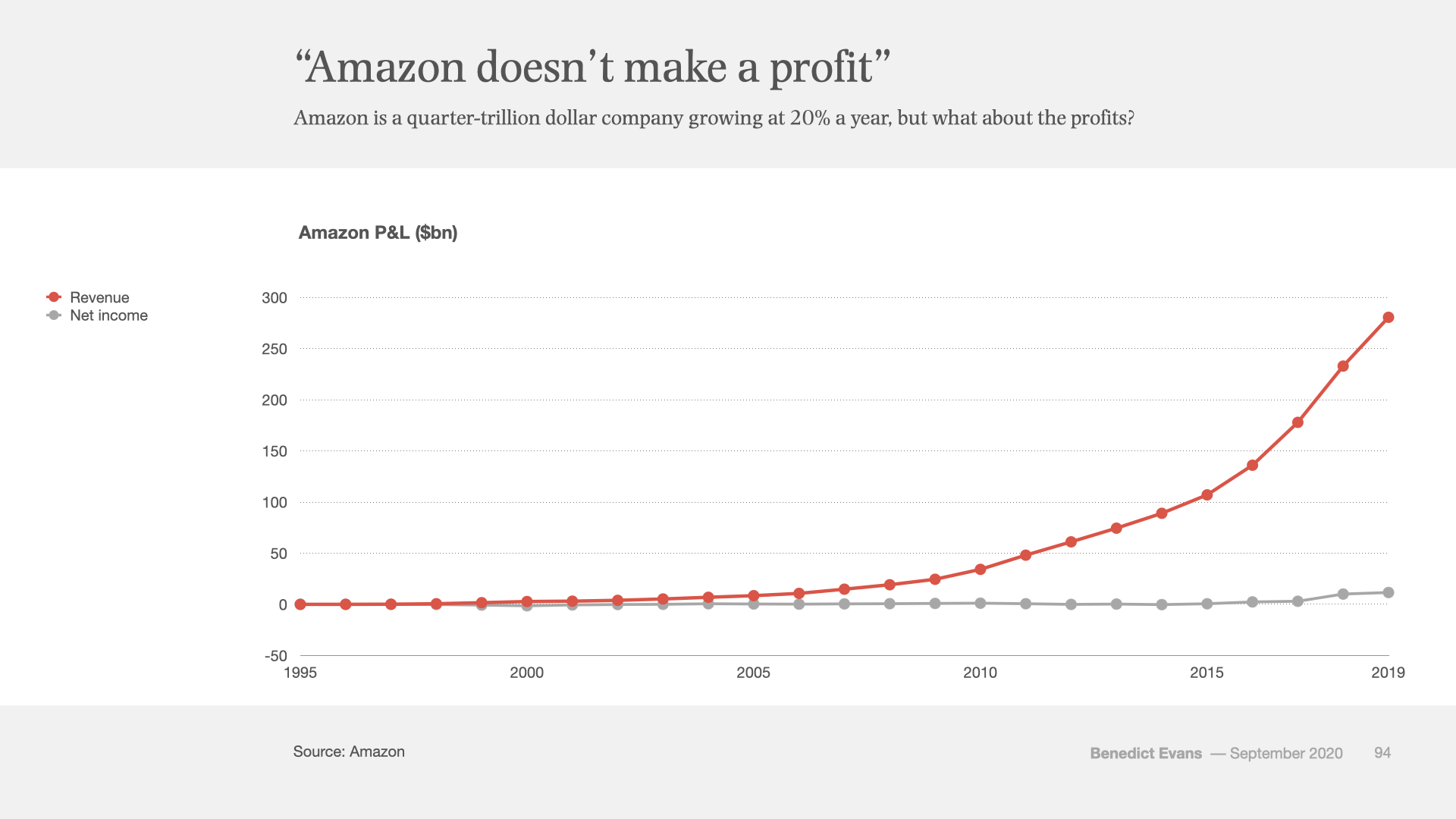

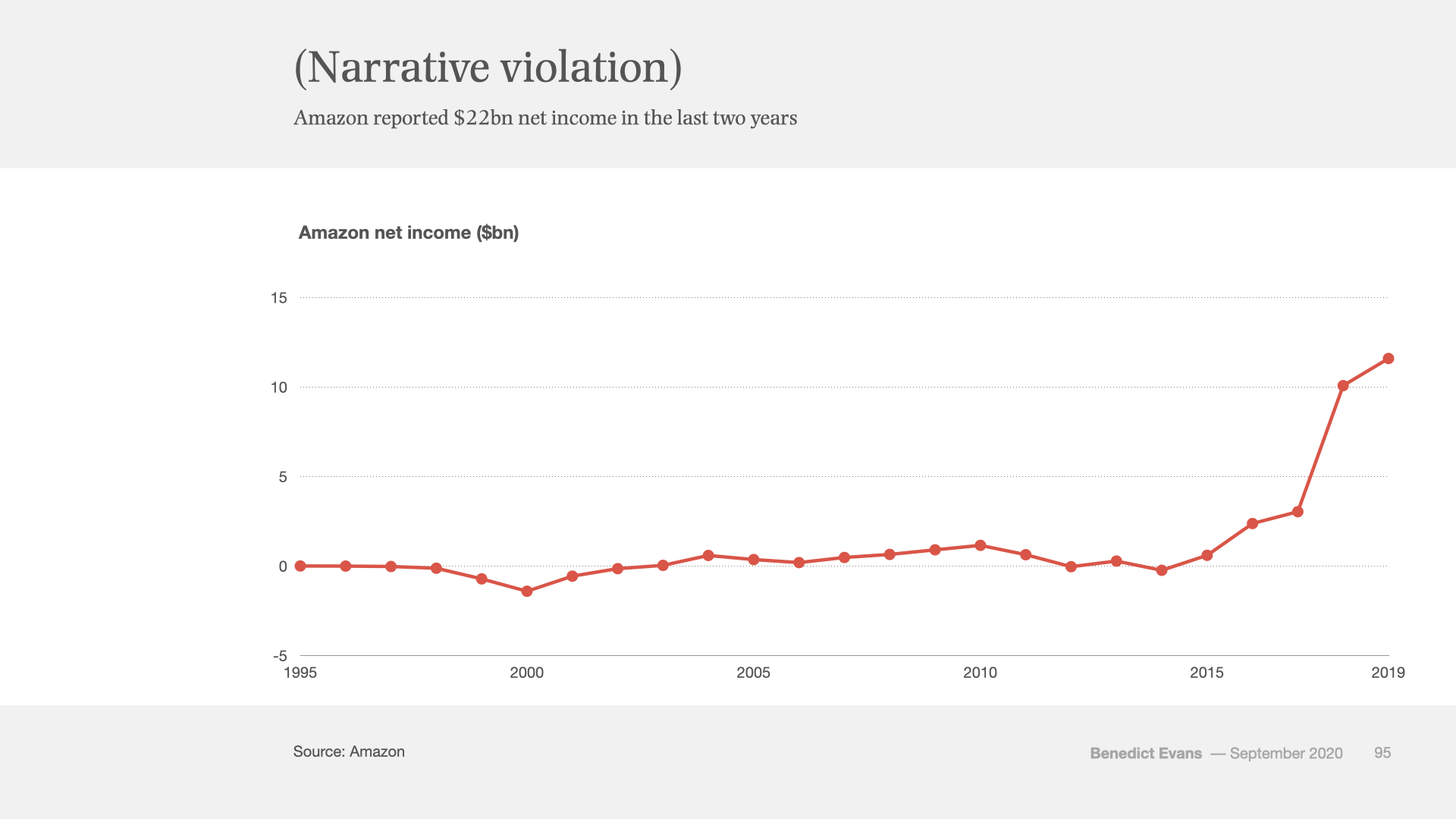

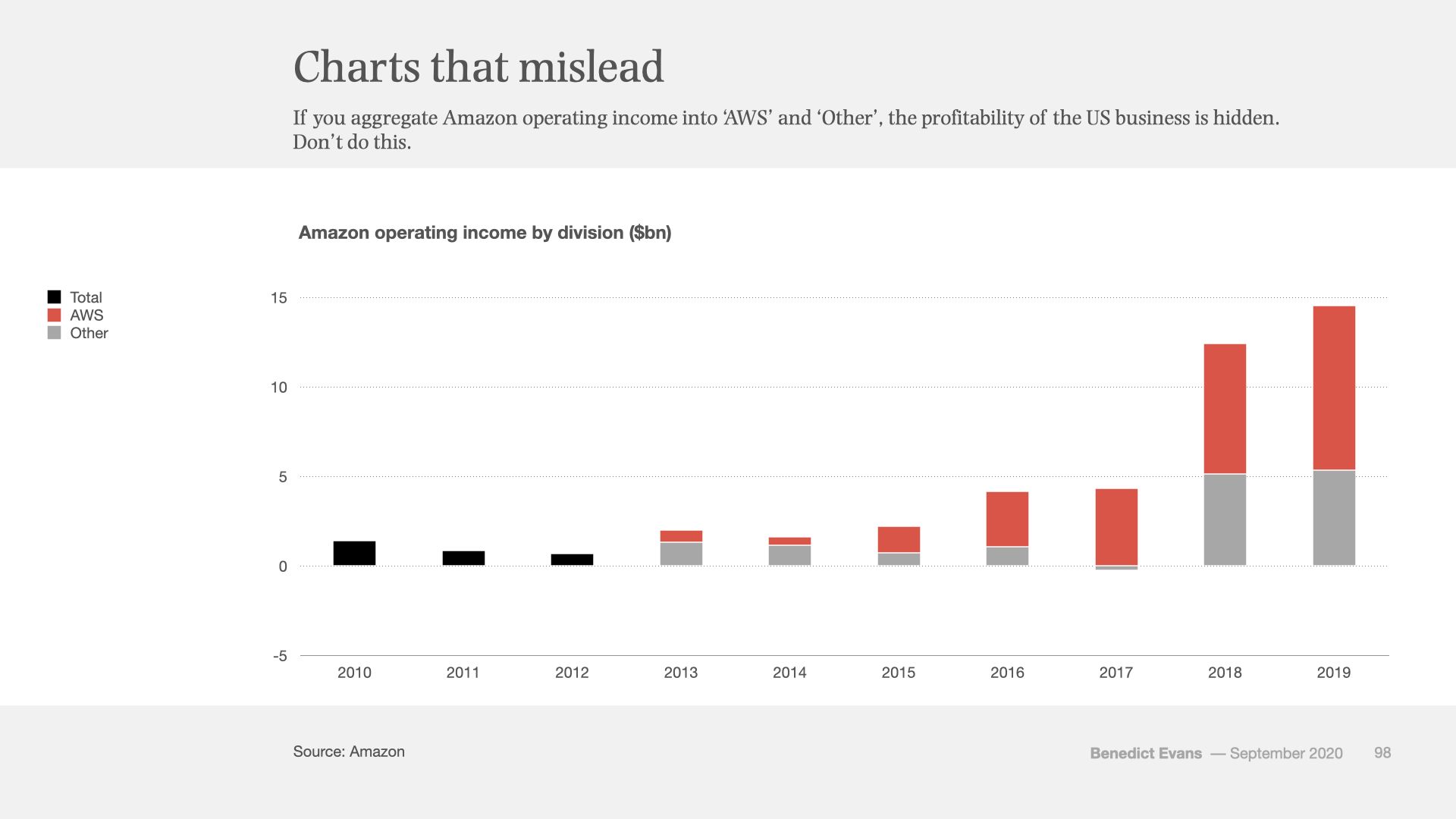

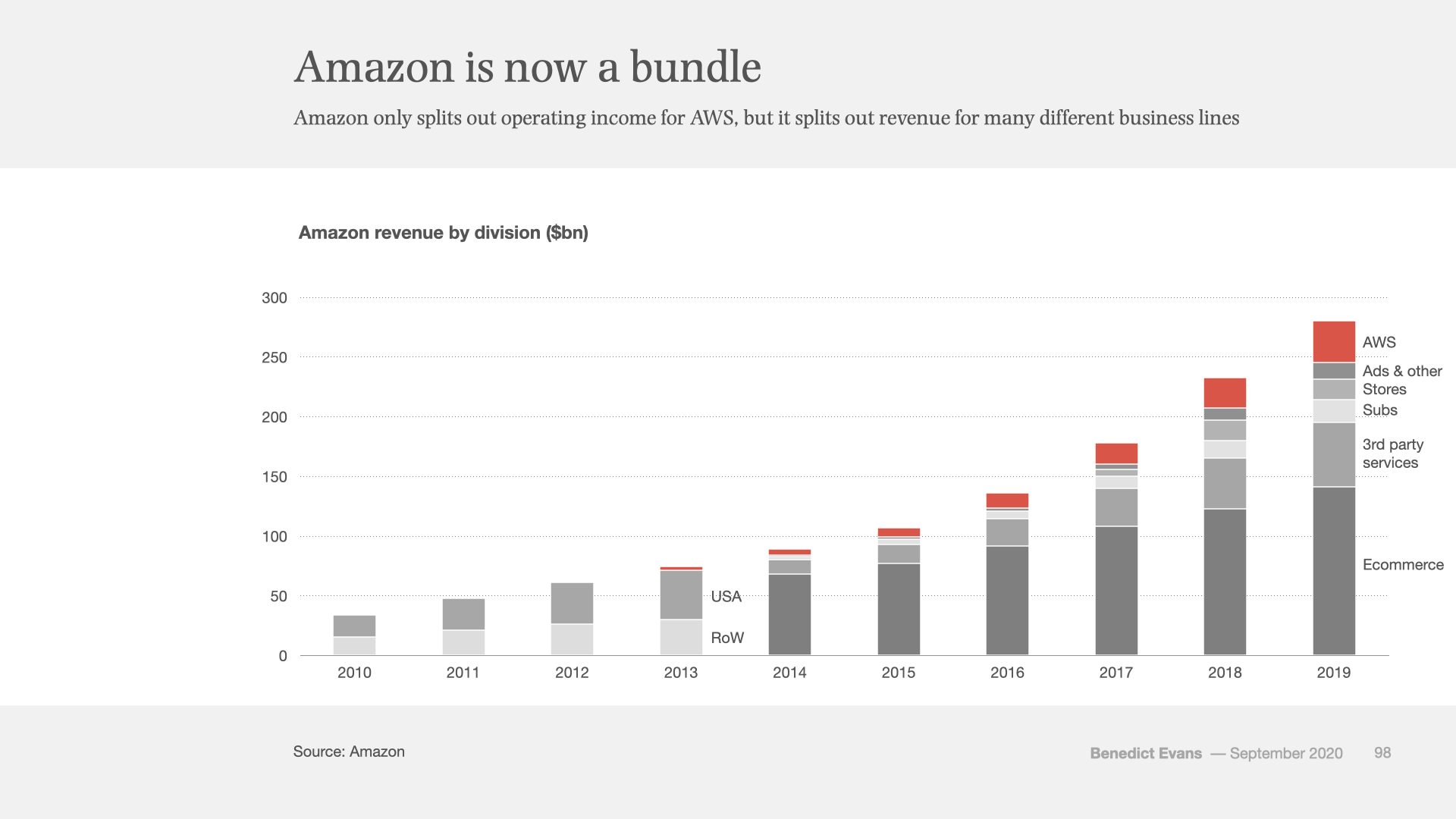

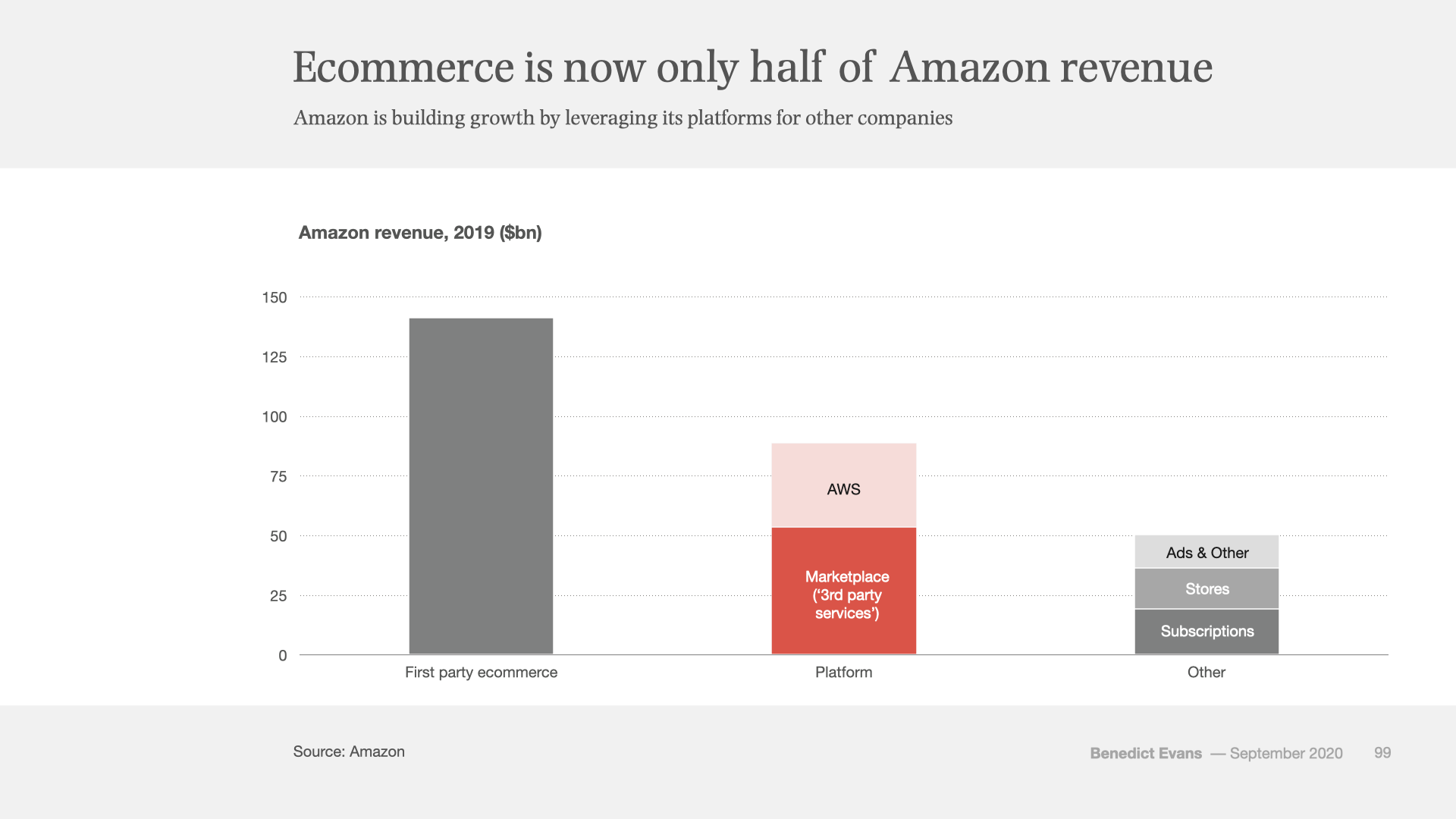

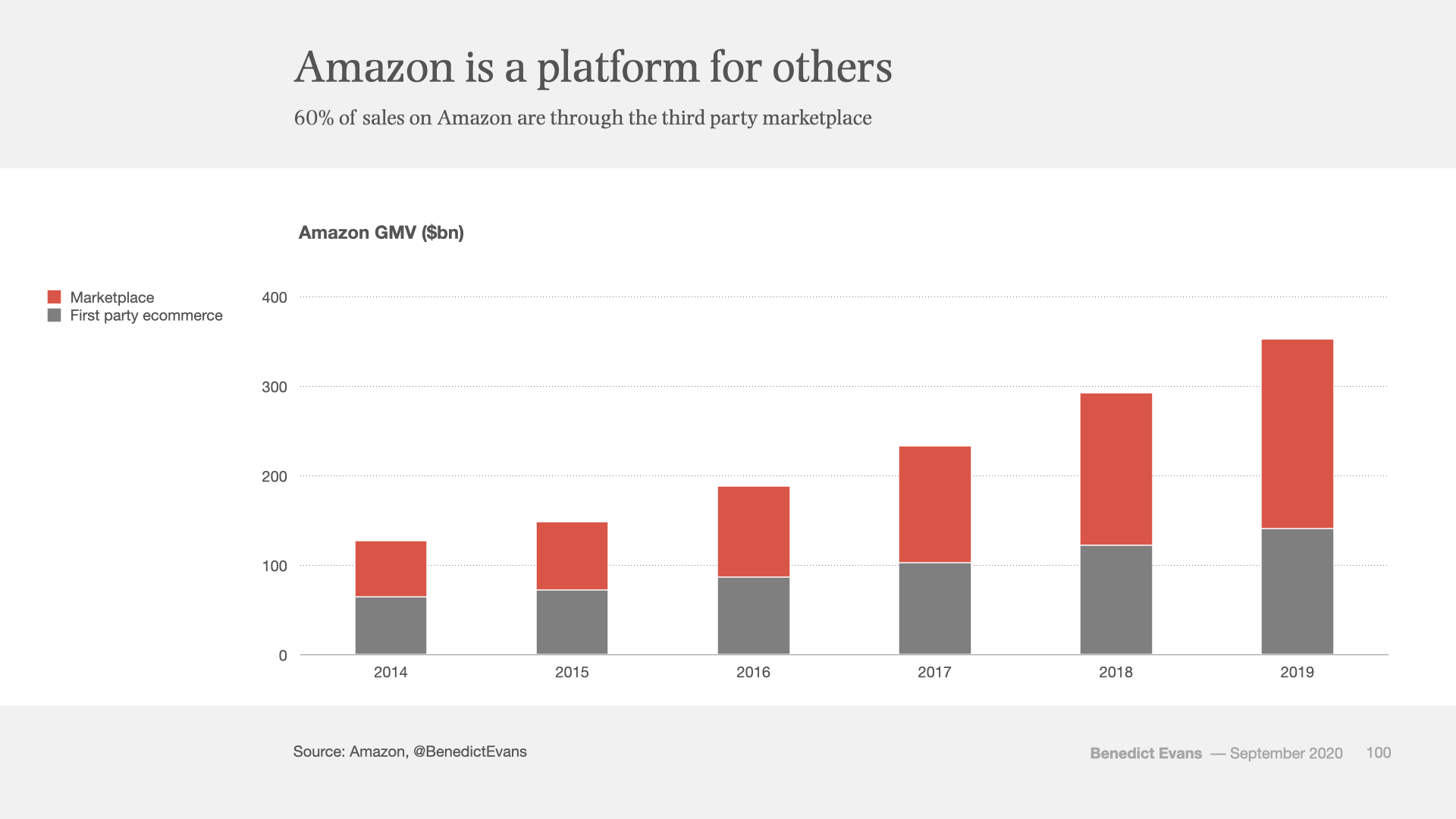

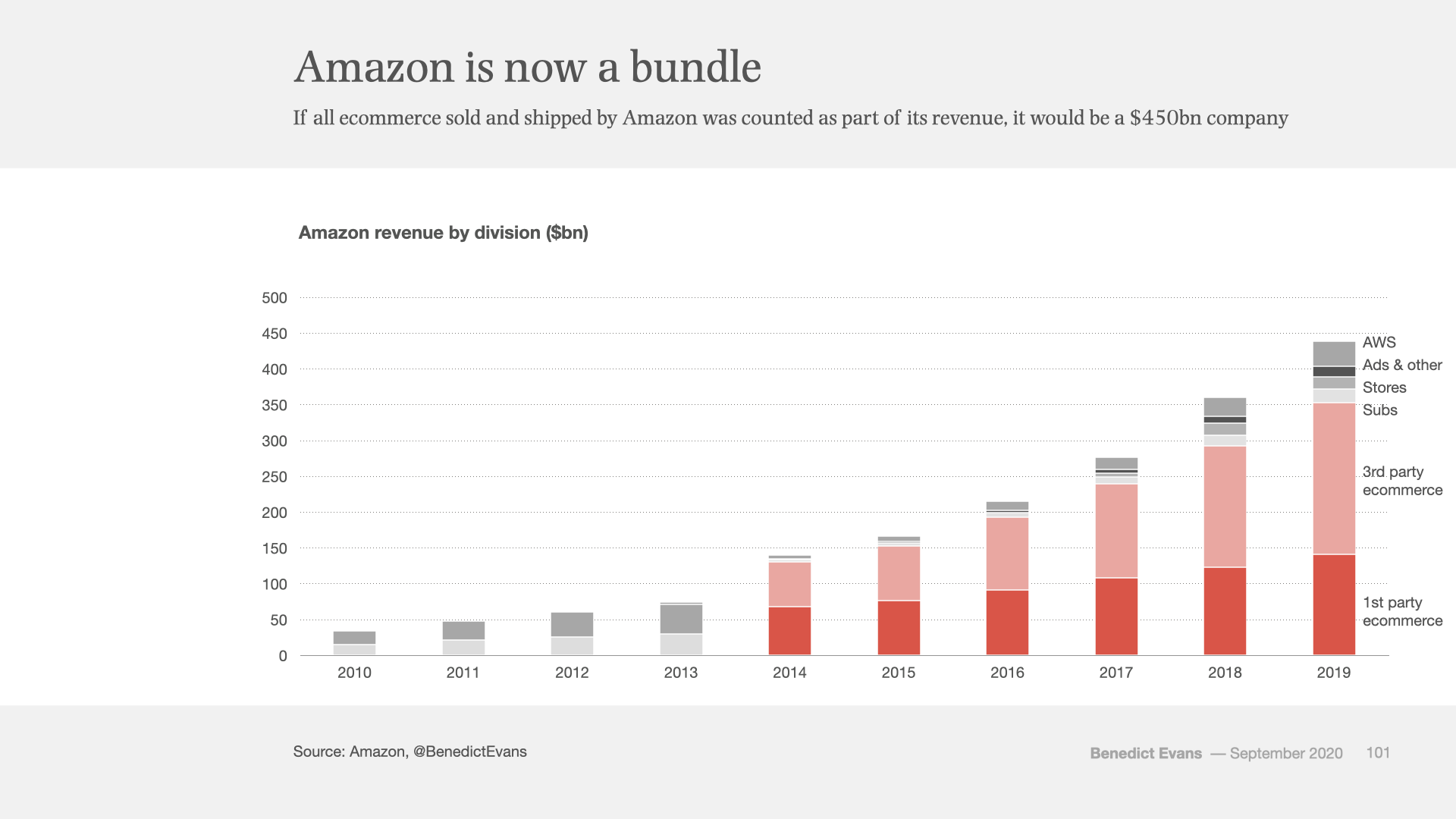

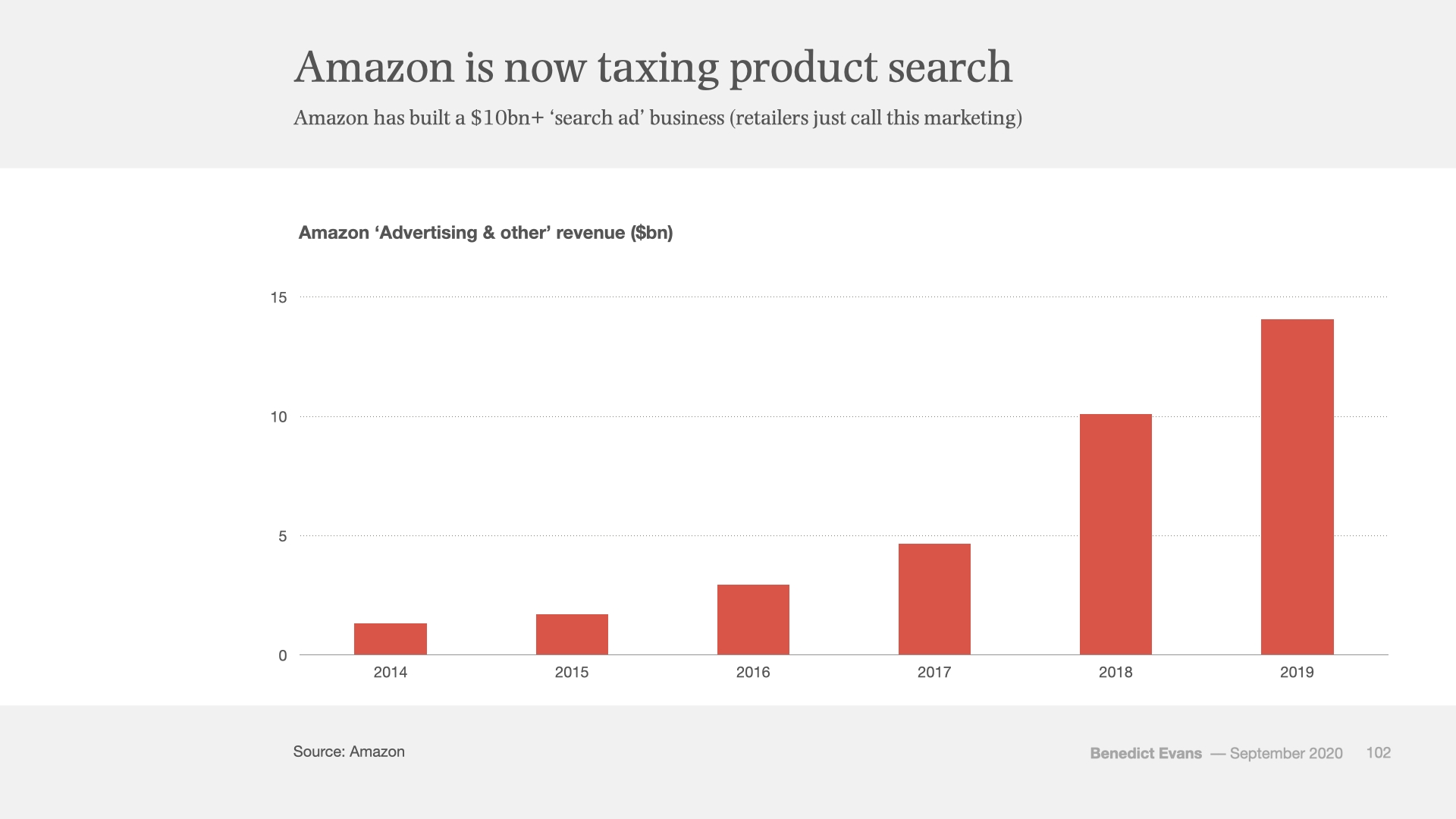

People argue about Amazon a lot, and one of the most common and long-running arguments is about profits. The sales keep going up, and it takes a larger and larger share of US retail every year (7-8% in 2019), but it never seems to make any money. What’s going on?Well, to begin with, this idea itself is a little out of date: if we zoom in on that net income line, we can see that Amazon’s profitability appears to have shot up in the last couple of years. But what else is going on?An obvious response here is that all of the profit is coming from AWS: it’s easy to assume that AWS’s profits subsidise losses in the rest of the company. By extension, if anti-trust intervention split AWS apart from the rest of the company, those cross-subsidies would go away and Amazon would have to put up prices, or grow more slowly, or at any rate be a less formidable and aggressive competitor.That doesn’t really stand up to examination.AWS has been around in some form since the early 2000s, but Amazon didn’t disclose financials, and the products looked so cheap that many people presumed that it must be making a loss. Then, in 2015, reporting regulations meant that Amazon had to start giving numbers (with historic figures back to 2013), and we discovered that in fact it was hugely profitable. Hence, in 2015 and 2016 AWS was the great majority of Amazon’s reported operating income. However, that’s not true anymore - the US business is also now generating substantial operating profit, and, on this basis, it’s only the international business that’s losing money.There is an easy way to get this wrong if you’re not careful. If you only look at AWS and total operating profit, or aggregate the numbers that Amazon reports into AWS and ‘Other’, the resulting numbers will be misleading: the losses for RoW balance out the profit in the USA and make it look as though AWS is the only profitable business, especially from 2015 to 2017. The chart below shows the result: close to $3bn of operating profit in the US business in 2017 has vanished, and so has a $3bn operating loss in the RoW business. Don’t do this.This is a great illustration of a broader challenge: Amazon is lots of businesses, but you only see the profitability of the aggregate.Hence, Amazon reports revenue and operating income for three segments: AWS, USA and Rest of World. The chart below shows the revenue (and also lets you see that AWS is a much higher-margin business).However, this is not the only kind of disclosure that Amazon gives. If you scroll a little further through the 10-K, you will find that since 2014 the company has also disclosed revenue (though not profitability) on a quite different and much more informative basis.‘First party ecommerce’, where Amazon sells you things on its own behalf on the Amazon website, is now only about half of Amazon’s revenue. Another third comes from providing platforms for other people to do business: AWS is one part of this and Marketplace, or ‘third party services’ is the other.Amazon lets other companies list products on its website and ship them through its warehouses as the ‘Marketplace’ business. It charges them a fee for this, and it reports the fee as revenue (‘third party services’), and it makes a profit on that. Amazon doesn’t treat the value of the actual purchases as its own revenue, which is in line with US accounting rules, since technically Amazon is only acting as an agent. So, if you buy a $1,000 TV on Amazon from a third party supplier, Amazon will charge the supplier (say) $150 in fees for shipping and handling and commission, and only report $150 as revenue. However, it has started stating, in rounded numbers, what percentage third party sales make up of total sales on Amazon - so-called ‘gross marketplace value’ or GMV. Last year, it was about 60%.As an intellectual exercise, it’s interesting to think about what this would look like if the accounting rules were different and everything sold and processed through Amazon’s website was reported as Amazon revenue. On an operational level, this is pretty much what happens today: Amazon’s own ecommerce product teams are charged an internal fee by the logistics platform and by the digital platform in much the same way that external marketplace vendors are charged a fee. Hence, if these were reported on a like-for-like basis, Amazon’s revenue in 2019 would have been close to $450bn.Marketplace gets quite a lot of attention these days, but it’s also worth a quick look at one of the small and insignificant-looking series on that chart - ‘ads and other’. The vast majority of this is Amazon’s business selling placement on the home page and in product search results, which it has built up from almost nothing in the last five years. This is what that business looks like in isolation - it did close to $15bn of revenue in 2019. A billion here and a billion there can add up to real money.Amazon doesn’t disclose profitability for this segment, but we can make some informed (wild) guesses. So: it mostly leverages existing technical infrastructure and engineering resource. It must have meaningful numbers of sales and operations people, but the system itself is mostly automated. It will have knock-on consequences to other parts of the business - for example, it may steer sales to product with higher or lower profitability. And it seems reasonable to assume that it has pretty high margins.So, for comparison, Alphabet had a 2019 operating margin before R&D and TAC (it’s at least arguable that neither apply here) of 57%, and AWS reported 2019 operating margin of 26%. On that basis it’s reasonable to suggest that the ad business is contributing as much operating income as everything else apart from AWS, and it’s not absurd to suggest it might be close to matching AWS.Close to six years ago I wrote a pretty popular essay about Amazon’s business at the time - ‘Why Amazon has no profits’. That made two points.First, Amazon is not one business - it’s many different businesses, at different stages of maturity and profitability. Some of those businesses are established and highly profitable and others are new and in a start-up loss making phase, but you can’t really see from the outside, because all of the money gets both aggregated and reinvested. You can see exactly the same thing in these charts. Amazon is not a loss-making business that will eventually have to raise prices to make money; rather, it’s many businesses leveraging a common platform and a common balance sheet.Second, Amazon is run for cash, not net income. Jeff Bezos always says that he runs it for ‘trailing 12 months’ absolute free cashflow’, not net income, and it’s had positive cashflow since 2002, which is before some startup founders were born. It’s a drawback of these charts that they’re based on operating income, not cashflow, but that’s what we’ve got. There’s also a bunch of other interesting things one could dig into - stock compensation, say, or the cash conversion cycle. But the important thing is that if you want to understand a company, it’s worth reading the accounts.

0 comments:

Post a Comment