Which Platforms Are Really Leading the Streaming Wars?

After Netflix and Disney+, everyone else is, for now, an also-ran. JL

Kelsey Sutton reports in Ad Week:

The real battle is for third place. There are few illusions that streaming upstarts will be able to

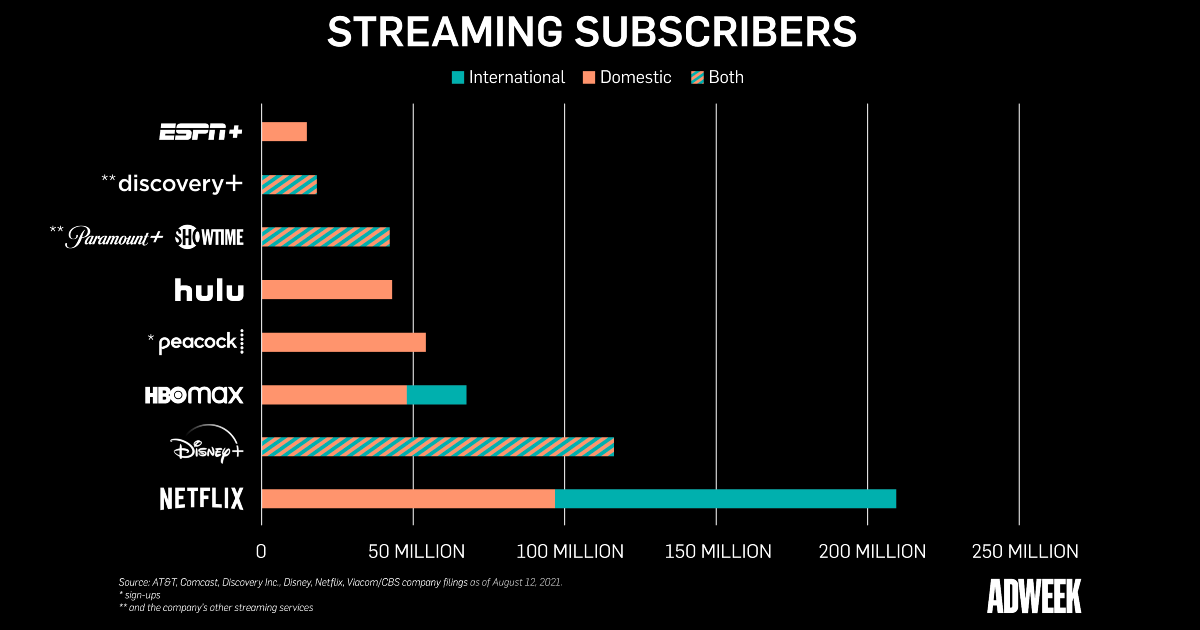

match the scale of Netflix (which) ended the quarter withmore than 209 million global subscribers -

74 million of them from the U.S. and Canada. Only Disney+ has exhibited the ability to

rapidly scale up and potentially be able to reach Netflix. That maybe the biggest reason behindthe mega-merger between Discovery, which has 18 million

streaming subscribers, and WarnerMedia, which has 67.5 million

subscribers through HBO Max and HBO.

Even though streaming wars have been underway for several years, the battle is really only heating up now as all the major players are finally on the battlefield and digging in. The big media companies have been focused on launching their new platforms—or revamping existing ones—in their efforts to fight for relevancy and revenue as consumers shift from linear TV to streaming.

Now that the major streaming players on the market have reported quarterly earnings to investors, we have a better picture of how the competition is currently stacking up. Here are our biggest takeaways from the current state of streaming.

Adweek

The real streaming battle is for third place

There are few illusions that many streaming upstarts will be able to match the scale of Netflix, at least for some time. That streaming goliath ended the quarter withmore than 209 million global subscribers—roughly 74 million of them from the U.S. and Canada—and while other streamers are racing to catch up, only Disney+ has exhibited the ability to rapidly scale up and potentially be able to reach Netflix’s lofty heights.

At the end of the quarter, Disney+ had an astonishing 116 million subscribers. Combine Disney+’s subscriber numbers with the other streamers in its portfolio, ESPN+ and Hulu, and the company’s total combined streaming subscribers are close to nearly 174 million subscribers. (Instead of declaring victory, Disney CEO Bob Chapek told investors not to reach too-early conclusions about the streaming market’s total scale; “I like to think of it like we’re in the first inning of the first game of a very long season,”Chapek said.)

Even as other streamers exceed their internal metrics for growth, they are more realistically aiming for a respectable third place in the streaming wars. Some companies, like WarnerMedia and Paramount+, have head starts simply due to their ability to repurpose existing subscriber bases (from HBO and CBS All Access, respectively) for their new business realities, and the eagerness to bulk up also makes acquisitions an attractive option.

That maybe the biggest reason behindthe planned mega-merger between Discovery Inc., which has 18 million streaming subscribers, and WarnerMedia, which has 67.5 million subscribers globally through HBO Max and HBO.

“We think that this will be the third global streaming service,” Discovery CEO David Zaslavtold investors this quarterabout the soon-to-be combined company. “Successful, sustainable—that’s our mission.”

Scaling globally is taking longer than expected

Streamers can’t make that scale happen without expanding internationally, where many markets are less mature than in the U.S. and offer more room for growth. ViacomCBS CEO Bob Bakish told investors of the strategy that is guiding most major streamers on the market so far.

“Our streaming strategy overall is to access the largest total addressable market and to do so by leveraging the full power of ViacomCBS,” he said. “That obviously means global, so international is a key component.”

For smaller services like Paramount+ and Peacock, global expansions call for distribution partnerships. Comcast, which owns British broadcaster Sky, will add soon NBCUniversal streamer Peacock to Sky’s 20 million customers in Europe at no additional cost, Comcast CEO Brian Roberts said.

ViacomCBS is also using Sky: beginning next year, Paramount+ will be offered for no additional charge to subscribers to Sky Cinema in the U.K., Ireland, Italy, Germany, Switzerland and Austria, and as an add-on option for other customers in those markets. Time will tell how successful those partnerships will be, but both companies said the effort will improve brand recognition and offer a chance to win over international customers looking for local programming.

But expansion into international markets is a difficult business, and is taking longer than planned for some streamers. Both WarnerMedia and Disney told investors this quarter that their global expansions would be delayed slightly, with WarnerMedia pausing its launches in certain European markets back until early 2022, and Disney delaying its eastern European expansion from late 2021 until summer 2022.

Those postponements reflect the challenges of the business and shifted priorities in that expanded roll-out. WarnerMedia is delaying its European expansion so it can focus on its Latin American roll-out, AT&T chief financial officer Pascal Desroches told investors, while Disney is pausing its eastern European expansion so that it can also include certain markets in the Middle East and South Africa, Chapek told investors.

Some are being evasive about subscriber numbers

Every quarter, there’s a better picture as to the scale of the growing streaming landscape as companies disclose to their investors their progress and occasionally update their projections. But those disclosures can get murky depending on how companies report, and there is room for some obfuscation as companies choose different metrics to measure success.

NBCUniversal’s Peacock has perhaps been the least transparent about their size and their consumer engagement. The company has declined to share more figures other than sign-ups, whichreached 52 million at the end of the quarter, and monthly active users, which number at about 20 million. While those figures sound impressive, it offers few details, especially how much consumers are watching on the service—a key metric on the advertising side—and how many subscribers have opted for the Peacock Premium tier vs. the free offering.

Peacock isn’t the only company keeping its figures cloudy. ViacomCBS and Discovery, two of the smaller streamers on the market, don’t report out their streamers’ subscribers individually, instead lumping them in with subscribers to other streaming services.

ViacomCBS’ numbers include Paramount+, Showtime OTT and smaller platforms like BET+, while niche streamers like MotorTrend are combined with Discovery+ subscribers, making total growth impossible to gauge exactly. HBO, too, makes it difficult to parse which of its subscribers are HBO Max sign-ups versus HBO cable subscribers who activated their free HBO Max accounts at no additional cost.

Obfuscation isn’t exactly new in the streaming space—Netflix has eschewed Nielsen figures as incomplete and self-reports viewership on its own metric that makes it hard to compare to other streamers. But in an ultra-competitive landscape, companies are even less keen on revealing their strengths and weaknesses, and are even devising clever accounting tactics to hide some of the true costs of their streaming business expansions.

Streaming is taking a bigger share of upfront dollars

For the companies that have ad-supported tiers to their services, a rebounding advertising market is translating into some big wins during the upfronts. One of the biggest winners is Discovery Inc., which since launching in January has seen more than800 advertisers buy inventory on Discovery+—more than four times the company had expected, chief financial officer Gunnar Wiedenfels said.

That momentum is being felt elsewhere. Paramount+’s domestic advertising revenue more than doubled compared to a year ago, chief financial officer Naveen Chopratold investors, and streaming—which also includes the free ad-supported service Pluto TV—”will represent close to 15% of total company revenue in 2021,” he said.

At Disney, 40% of Disney’stotal upfront dollarswent to streaming and digital, which encompassed not just Hulu but to other entertainment and sports platforms. That increase was mainly due to Hulu, which benefitted from higher impressions and a dynamic ad insertion technology on its live television product that allowed for better monetization,said chief financial officer Christine McCarthy.

“The advertising sales team, if they had more inventory, they would sell it, because there’s that much demand for it,” McCarthy said. “The kind of advertising going through Hulu is a growth driver.”

Franchises are still the future

If it wasn’t already clear enough, streaming services are going to be the home for some of the entertainment industry’s biggest and most lucrative franchises. Disney has made its investment plain withexpansions of the Star Wars and Marvel franchises into television, but other companies are following suit: WarnerMedia isreadying a DC Comics expansionwith the John-Cena-led Peacemaker series (a spinoff from the recent Suicide Squad film) early next year, while ViacomCBS is readying its ownfranchise-fueled content plan.

That’s because it’s a simple and nearly fool-proof plan to attract audiences. At Paramount+, the revival of Nickelodeon series iCarly was the leading acquisition driver in the quarter, a proof point of the value of some of Nickelodeon’s properties that the company will look to replicate.

“We really are big believers in franchises and their associated value,” Bakish said. “You know, they have broad consumer appeal and awareness. You can do all kinds of things with them creatively, they obviously have commercial potential, including extensibility, to things like consumer products, and they tend to play globally. So we like franchises.”

As a Partner and Co-Founder of Predictiv and PredictivAsia, Jon specializes in management performance and organizational effectiveness for both domestic and international clients. He is an editor and author whose works include Invisible Advantage: How Intangilbles are Driving Business Performance. Learn more...

0 comments:

Post a Comment