One of the issues may be the rising impact of the experience economy, a category distinct from services and whose values and prices are increasing at a greater rate than either goods or services. The result is that inflation data may be skewed in the same way an outdated emphasis on tangibles over intangibles has failed to account for how and on what consumers are choosing to spend. Until adjustments are made, economic analysis will be suboptimal. JL

B. Joseph Pine reports in the Wall Street Journal:

Consumer values have shifted over the years, notably from goods and services to experiences. Consumers value their time more highly than they used to. The pandemic decimated physical experiences so we shifted from the physical to the digital, from the communal to the familial and individual. The government classifies experiences as services. (But) the disparity in value is profound between going to a dry cleaner and a concert or between home delivery and a day at a theme park. The pandemic made clear that what gives life meaning is shared experiences. The standard has shifted toward experiences and how much faster they increase in value - and therefore price - than services.With inflation at its highest rate since 1982, the topic seems to be on everyone’s minds, from policy makers to shoppers. The worry is especially acute as inflation appears to be rising still.

Inflation tends to be understood as higher prices resulting either from increased costs—global supply-chain issues and hard-to-find workers—or from increased demand, such as pent-up purchases, as well as easy monetary policy from the Federal Reserve and blowout spending from Congress. But there’s another significant factor at play: Price increases also arise from growth in the perceived value of economic offerings.

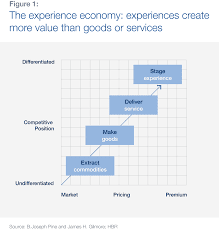

Consumer values have shifted greatly over the years, most notably from goods and services to experiences. As I first argued on these pages in 1997 with my business partner, Jim Gilmore, experiences are a distinct economic offering, as different from services as services are from goods.

Fundamentally, experiences offer time well spent. People value the time they spend in experiences, resulting in a memory (and, so often these days, a trail of social media posts). Experiences have always been around—concerts, plays, sporting events and tourism, long the largest industry in the world by employment. The 20th century saw the rise of experience industries such as movies, radio, television, theme parks and videogames. The 21st century has brought entirely new genres of experiences, including social media, escape rooms and immersive art encounters.

The pandemic decimated physical experiences; no one wanted to gather with others. Experiences are intrinsically important to human beings, so we shifted from the physical to the digital, from the social and communal to the familial and individual. But whenever experiences opened up again—theme parks, bars and restaurants—they filled to whatever capacity the government allowed. Movie theaters proved a big exception, but “Spider-Man: No Way Home,” released in December, showed the way back to packed theaters by finally offering a blockbuster film that people really wanted to see in full cinematic splendor.

Unfortunately, the government still classifies experiences as services. The latter, however, merely provide time well saved. The disparity in value is too profound between, say, going to a dry cleaner and a concert, between having your oil changed and changing your physique at a gym, between home delivery of goods and the spending the day with your family at a theme park.

Worse, the Bureau of Labor Statistics has yet to catch up to this shift in the economy. The standard market basket it uses to measure the consumer-price index is still weighted too much toward goods and traditional services. The result: The CPI for decades has been measured as lower than the actual rate. Shouldn’t we be more precise in measuring how people actually spend money?

One comparison illustrates the point. Walt Disney World first charged a single admission fee in 1981, no longer requiring separate tickets for individual rides. According to AllEars.net, a website dedicated to covering Walt Disney Co., the price back then was $9.50—$8.89 excluding the 4% sales tax.

Fast-forward to 2021, and a one-day standard ticket price is $109 before taxes. That’s a compound growth rate of 6.39%. Meanwhile, the CPI increased by 2.76% a year over that same period. So for 40 years the price to go to Walt Disney World has gone up 2.3 times as fast as the CPI. Is that because its costs—cast-member wages, ride-building supplies—have gone up so much more than in other businesses? Hardly. It’s because of more engaging and immersive rides, greatly expanded areas, shorter wait times and more personal attention.

That’s why Walt Disney World outpaced measured inflation by so great a rate—because consumers value its experience more than the average market-basket good and are willing to pay much more for it relative to other offerings. This same effect is true for the myriad experiences that make up today’s “Experience Economy.”

Consumers also value their time more highly than they used to. They want goods and services to be commodities—bought at the lowest possible price and greatest possible convenience—so they can spend their hard-earned money and their harder-earned time on experiences they value more highly.

This is true for several reasons, among them that average household income has increased enough (at least in the developed world) to pay for most all the necessary “stuff.” One of the things the pandemic made clearer is that what gives life meaning isn’t stuff but shared experiences—with family, loved ones, colleagues, and even strangers.

The federal government needs to recognize experiences as the distinct economic offering they are and accurately take them into account in its statistics, including how the standard market basket has shifted toward experiences and how much faster they increase in value—and therefore price—than services. That would lead to a better understanding of the economy.

0 comments:

Post a Comment