Why Private Equity Firms Are Pouring Investment Into Tech Start-Ups

Tech investments accounted for 41% of all private equity deals in 2021. While this is a strong endorsement of tech's current and perceived future strength, as the pandemic enhanced tech's importance, it is also a sign of excess cash seeking too few opportunities.

Part of the 2021 influx was driven by concern for potential US tax changes that now seem less likely to occur. Combined with the very high valuations at which tech companies are selling, there is growing concern that these investments may not be able to generate anticipated returns and may even be a sign that founders and VCs are playing the greater fool theory game with overeager private equity investors. JL

\Laura Cooper and Preeti Singh report in the Wall Street Journal:

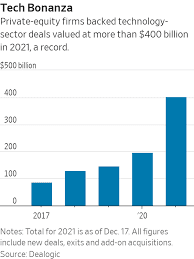

Private-equity firms announced backing U.S. technology deals

totaling $401.71 billion, including new purchases, asset sales and

add-on deals in 2021. That accounted for

41% of a record $990.25 billion in overall private-equity deals, more than double the 2020 level. Private-equity finds software-as-a-service

businesses particularly attractive, as these offer reliable

recurring-revenue models and yield consistent returns. The pandemic drove greater digital adoption, making technology-enabled businesses all the more alluring. (But) companies sell for 20 or 30 times Ebitda, while

years ago 15 times was the norm. Elevated valuations could make it tougher to generate strong returns

Private-equity firms had a blockbuster year for deal making, largely driven by technology investments.

As of mid-December, private-equity firms had announced backing U.S. technology deals totaling $401.71 billion, including new purchases, asset sales and add-on deals, according to data provider Dealogic. That accounted for 41% of a record $990.25 billion in overall private-equity deals through mid-December, Dealogic said.

The tech-deal value for 2021, which more than doubled from the 2020 level of $196.34 billion, was the highest since Dealogic began tracking the data in 1995. In 2020, tech transactions also represented 41% of overall private-equity deals, which totaled $474.06 billion.

Investors say they expect more tech deals in 2022. Private-equity fund managers have long found software-as-a-service businesses particularly attractive, as these companies offer reliable recurring-revenue models and yield strong and consistent returns. The Covid-19 pandemic drove greater digital adoption across all aspects of life, making technology-enabled businesses all the more alluring to investors and whipping up competition for tech companies.

Pent-up investor demand and sellers eager to strike deals ahead of anticipated tax changes helped drive activity, said David Humphrey, co-head of Bain Capital’s North American private-equity business. The tech sector’s strong performance throughout the pandemic also buoyed deal volume, according to Mr. Humphrey, who worked on the pending$17 billion acquisition of healthcare-technology company Athenahealth Inc. by Bain Capital and private-equity firm Hellman & Friedman LLC.

Bain Capital and Hellman & Friedman LLC struck a deal to buy Athenahealth for $17 billion.

PHOTO:JENNY KANE/ASSOCIATED PRESS

Other large tech deals in 2021 included theroughly $12 billion pending acquisition, excluding debt, of Nasdaq-listed cybersecurity provider McAfee Corp. by a consortium including investors Advent International and Permira Advisers as well as Clearlake Capital’sagreement to buyQuest Software Inc. from Francisco Partners for about $5.4 billion, including debt.

However, private-equity firms often must pay up to win these deals.

Richard Hardegree, a vice chairman at Barclays PLC who leads technology mergers and acquisitions at the investment bank, said he routinely sees companies sell for roughly 20 times or even 30 times their annual earnings before interest, taxes, depreciation and amortization, while years ago a purchase price of 15 times Ebitda was the norm.

“This has been a tale for the last decade-plus of increasing Ebitda multiples, particularly in the software space, where most of the activity has occurred,” he said. “We’ll see how it ends. I think there are a lot of people—including myself—who were skeptical at 15 [times], and now we’re at 30 [times] Ebitda.”

As firms spend more to win deals, many have returned toraise new fundsrelatively quickly, a testament to the volume of cash in the market.

Private-equity firms specializing in technology investments, such as Vista Equity Partners, Thoma Bravo, Silver Lake and Francisco Partners, have started or are in the midst of fundraising for what would be their largest vehicles yet, in some cases returning less than a year after securing their previous funds.

Though many investors remain bullish about prospects for tech investing in 2022, some are raising concerns that elevated valuations could make it tougher to generate strong returns on certain technology investments.

“We expect to continue investing in 2022 but taking a bit more nuanced approach with sectors we like and staying away from sectors that we think could get hit hard in the down cycle,” said Mirza Baig, a managing partner at growth-equity firm Aldrich Capital Partners. Mr. Baig said valuations looked frothy in sectors such as European financial technology, wealth technology and real-estate technology.

“On the healthcare side, given the context of a global pandemic, we have seen a splurge by investors in parts of biotech, revenue cycle management, payer facing risk adjustment, and [the] perioperative space,” Mr. Baig said, adding his firm had passed on a number of deals in these areas.

Andrew Olinick, a partner at private-equity firm3i GroupPLC, said that he also has seen the market taking a harder look at potential deals.

“I think what happened for a while was if you were an average business you expected an exceptional price. Now what you’re finding is they’re not getting the exceptional prices,” Mr. Olinick said, noting that he has seen more failed deals in recent months.

“As [interest] rates go up there will be a bit more discernment,” he added. “I think businesses that are strongly performing will still command very full valuations.”

Great post I was just wondering to looks for it but I am looking for some Finance Homework Help USA during research I find ou this blog its related to my topic and help me to complete my homework.

Thank you for the information. Once I was given the task to write an essay on the topic of investments . But due to the lack of information, I could not start writing my work. I decided to turn to dissertation writing service uk for writing my assignment. Thanks to this, my work turned out to be informative and I learned a lot of interesting things for myself.

Thanks for sharing There is a growing demand for advanced technology solutions across all industries. financial analytics software , for instance, is increasingly sought after by businesses looking to leverage data for strategic decision-making. Private equity firms recognize this demand and invest in start-ups that can meet these market needs.

They're really pushing innovation forward. Have you thought about teaming up with a top video marketing agency in Saudi Arabia? They could help you share the exciting impact of these investments and attract even more opportunities.

Private equity firms are increasingly investing in tech start-ups within the car maintenance and repair sector for several compelling reasons. Firstly, these firms recognize the immense potential of technology to revolutionize traditional automotive services. By backing tech-driven solutions, such as innovative diagnostic tools, automated repair systems, and digital platforms for service scheduling and customer management, private equity firms aim to streamline operations and enhance efficiency in the car maintenance industry.

They see potential for high returns. These firms believe that supporting innovative technology can lead to profitable opportunities in the fast-evolving digital economy.

The amount of private equity that is currently being invested in technology is astounding. Although the numbers are enormous, there is undoubtedly some concern about whether these lofty values would ultimately result in profitable returns. It kind of makes you think about how sometimes things can get out of hand when everyone’s rushing into something. Kinda like when you’re drowning in assignments and thinking, "I need to pay someone to write my dissertation to get this off my plate!

Explores the increasing interest of private equity firms in the tech sector, driven by its growth potential and innovation. These firms are capitalizing on the disruptive nature of tech start-ups to secure high returns and gain market dominance.

As a Partner and Co-Founder of Predictiv and PredictivAsia, Jon specializes in management performance and organizational effectiveness for both domestic and international clients. He is an editor and author whose works include Invisible Advantage: How Intangilbles are Driving Business Performance. Learn more...

11 comments:

Great post I was just wondering to looks for it but I am looking for some Finance Homework Help USA during research I find ou this blog its related to my topic and help me to complete my homework.

Thank you for the information. Once I was given the task to write an essay on the topic of investments . But due to the lack of information, I could not start writing my work. I decided to turn to dissertation writing service uk for writing my assignment. Thanks to this, my work turned out to be informative and I learned a lot of interesting things for myself.

Thanks for sharing There is a growing demand for advanced technology solutions across all industries. financial analytics software , for instance, is increasingly sought after by businesses looking to leverage data for strategic decision-making. Private equity firms recognize this demand and invest in start-ups that can meet these market needs.

They're really pushing innovation forward. Have you thought about teaming up with a top video marketing agency in Saudi Arabia? They could help you share the exciting impact of these investments and attract even more opportunities.

Private equity firms are increasingly investing in tech start-ups within the car maintenance and repair sector for several compelling reasons. Firstly, these firms recognize the immense potential of technology to revolutionize traditional automotive services. By backing tech-driven solutions, such as innovative diagnostic tools, automated repair systems, and digital platforms for service scheduling and customer management, private equity firms aim to streamline operations and enhance efficiency in the car maintenance industry.

It's like everyone rushing to buy the latest Gucci marmont bag. They want to be part of something exciting and valuable.

They see potential for high returns. These firms believe that supporting innovative technology can lead to profitable opportunities in the fast-evolving digital economy.

Thanks for sharing There is a growing demand for advanced technology solutions across all industries. financial analytics software

The amount of private equity that is currently being invested in technology is astounding. Although the numbers are enormous, there is undoubtedly some concern about whether these lofty values would ultimately result in profitable returns. It kind of makes you think about how sometimes things can get out of hand when everyone’s rushing into something. Kinda like when you’re drowning in assignments and thinking, "I need to pay someone to write my dissertation to get this off my plate!

Explores the increasing interest of private equity firms in the tech sector, driven by its growth potential and innovation. These firms are capitalizing on the disruptive nature of tech start-ups to secure high returns and gain market dominance.

VUA88 vua88nyc vua88nyc vua88nyc vua88nyc

Post a Comment