But it is worth remembering that many of the tech innovations whose dominance we now take for granted - the smartphone, social media, the cloud - were initiated, seeded and grew during tougher economic periods. Venture investing and entrepreneurship are not going away. Success will go to the best and most discerning. JL

Adam Felesky reports in Fortune:

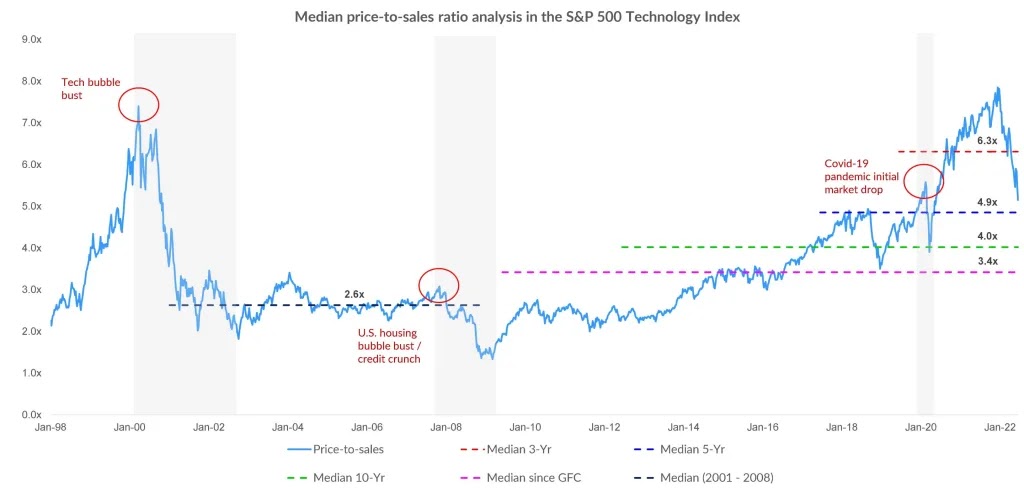

After a year of record-breaking funding, 2021 saw $621 billion in global venture capital financing, doubling the previous high. The number of unicorns surged in 2021, a 69% increase from the year before. (But) public tech revenue multiples peaked in December 2021 at 7.85x P/S. As of June 2022, they were at 5.15x. Public tech revenue multiples compressed by 75% in the dot-com bust (2001) and by 60% in the Great Recession (2008). It wasn’t until November 2014 that tech stocks recovered to pre-recession peaks and August 2021 they recovered to the peak before the dot-com bust. The easy money of boom days is gone though smart, disciplined venture investment is still available for the best companies.It may be blockbuster season at the movies, but over in the fintech investment space, the season for mega deals has passed. After yet another year of record-breaking funding—2021 saw $621 billion in global venture capital financing, easily doubling the previous high—the easy money of boom days is gone.

That said, smart, disciplined venture capital investment is still available for the best companies.

A hands-on, prescriptive investment approach is not easy. It requires in-depth knowledge of the market and significant resources combined with a disciplined and rigorous decision-making process. We believe in this approach in all cycles, and that its impact may become even clearer in a challenging market.

The blockbuster cycle and vanity

We are coming off a banner year in the tech investment space. Startups across several industries took advantage of record-breaking investment numbers to raise tons of capital at founder-friendly valuations. Portage portfolio companies alone raised almost $1.2 billion of capital in the last 12 months from investors.

Along with the blockbuster funding, the total number of unicorns also surged in 2021. The total number hit 959 last year, a 69% increase from the year before.

The focus on vanity markers, such as unicorn status, was a sure sign that we were approaching a “top”. In the run-up to the dot-com bust, “number of eyeballs” (i.e., daily/monthly unique site visitors) was a much-touted metric. Similarly, this valuation status was an all-consuming pursuit, rather than one data point among several important others in the journey of building a great long-term business.

And now, sure enough, the end of the boom cycle has come. Expected interest rate spikes, high inflation, the ongoing pandemic, and geopolitical tensions are contributing to a tumultuous market. According to our calculations, public tech revenue multiples peaked in December 2021 at 7.85x P/S and, as of June 2022, they were at 5.15x, a reduction of 34% from peak levels thus far. We will likely not reach a bottom in the market until inflation peaks. A period of muddiness could then follow until the markets can see through to the next growth cycle.

How muddy might it get, and for how long? If the past is a prologue, we may be able to learn something from how tech stocks did during the dot-com bust and the global financial crisis (GFC). Public tech revenue multiples compressed by 75% in the dot-com bust and by 60% in the GFC. It wasn’t until November of 2014 that tech stocks recovered to their pre-GFC peaks. It wasn’t until August of 2021 that they recovered to the peaks they had hit before the dot-com bust.

While we can’t predict the future, as tech multiples head quickly toward their five-year median, it’s not unreasonable to believe that it will take years to reverse.

Being a wartime investor

You can’t be a wartime investor unless your entire team understands that they are on the battlefield. As a first step, ensure your team understands that the market environment has changed.

Turn the focus to your existing portfolio to understand who is most at risk and what actions need to be taken to mitigate failure. Align with other investors and management and get on with it—don’t wait for another quarter or two—regardless of your financial position. Wartime does not reward those pursuing a wait-and-see approach.

Realign internally where you invest future human and capital resources. Sadly, both are finite, and when sources of capital thin out, the power law of venture capital becomes a mission-critical consideration. Making the right big bets is doubly important in this environment because there is a higher likelihood that the companies already in your portfolio will be looking to you to lead or support their future rounds.

Shift your focus to targeted origination. Now is the time to refine and reprioritize your theses through deep research, market mapping, and customer due diligence. This is also the perfect time to build and rigorously test your investment theses.

Meet as many companies as possible. It boils down to understanding why you are a differentiated investor for a company and what actions you can take to drive its success.

Being a wartime CEO

If you lead a later-stage venture business, the first step is the same: ensure your team understands that the market environment has materially changed.

Hopefully, you took advantage of the previous robust market and have built a war chest that gives you runway for at least 24 months before requiring new funding. If you have the luxury to drive toward breakeven by sacrificing top-line growth—do it. If you do not, then get clarity on what the company needs to look like at the end of the runway to be attractive to future investors, who are likely to be more disciplined than those you saw in prior rounds.

This most likely means being able to demonstrate efficient growth, expanding gross and operating margins, and visibility into future profitability. In action, this translates to radical internal prioritization. You have to be resolute in cutting out activity that doesn’t immediately drive toward these three tenets.

If you are an early-stage business, it’s imperative that you align with your investors on what success looks like. This is especially important because, in many cases, your next investor will probably be your current investor. If you are able to raise externally, you will likely have demonstrated some form of product-market fit to a specific segment with a good understanding of your pricing power. And you probably have done so on a rather modest budget. You also probably started with an awesome, passionate, mission-driven team that is now starting to attract top talent. Finally, I bet you can articulate concisely how important and big your mission is and why you will be the winner.

A new world order

Some may find that making a quick buck from investing in the cutest CryptoKittie is more fun than pouring over spreadsheets or A/B testing, but that part of the cycle has passed.

But venture capital isn’t easy for investors or founders, nor is it supposed to be. We must understand and adapt to the shifts of a new cycle. When the next growth cycle comes, the commitment and support we show our highest-potential startups will pay off exponentially as multiples start to expand again.

0 comments:

Post a Comment