New York Is Roaring Back From the Pandemic. Why Isn't San Francisco?

Location, location. In the post pandemic era, many people want to live and work in New York, even if they don't go to the office. And tourists are returning to NYC as well.

The explanation appears to be the conversion of more office space to apartments, New York's thriving media, law, tech and finance industries as well as its cultural scene. More stringent return to office policies by finance and law appear to be part of that. San Francisco has generally adapted Silicon Valley's relaxed hybrid approach. The result has been a strong rebound in NY. JL

Roland Li reports in the San Francisco Chronicle:

Manhattanlost 6.9% of its population, from April 2020 to June 2021, a more severe drop than San Francisco,which lost 6.7%. New York was the country’s coronavirus epicenter, with

41,000 deaths, 5 times the

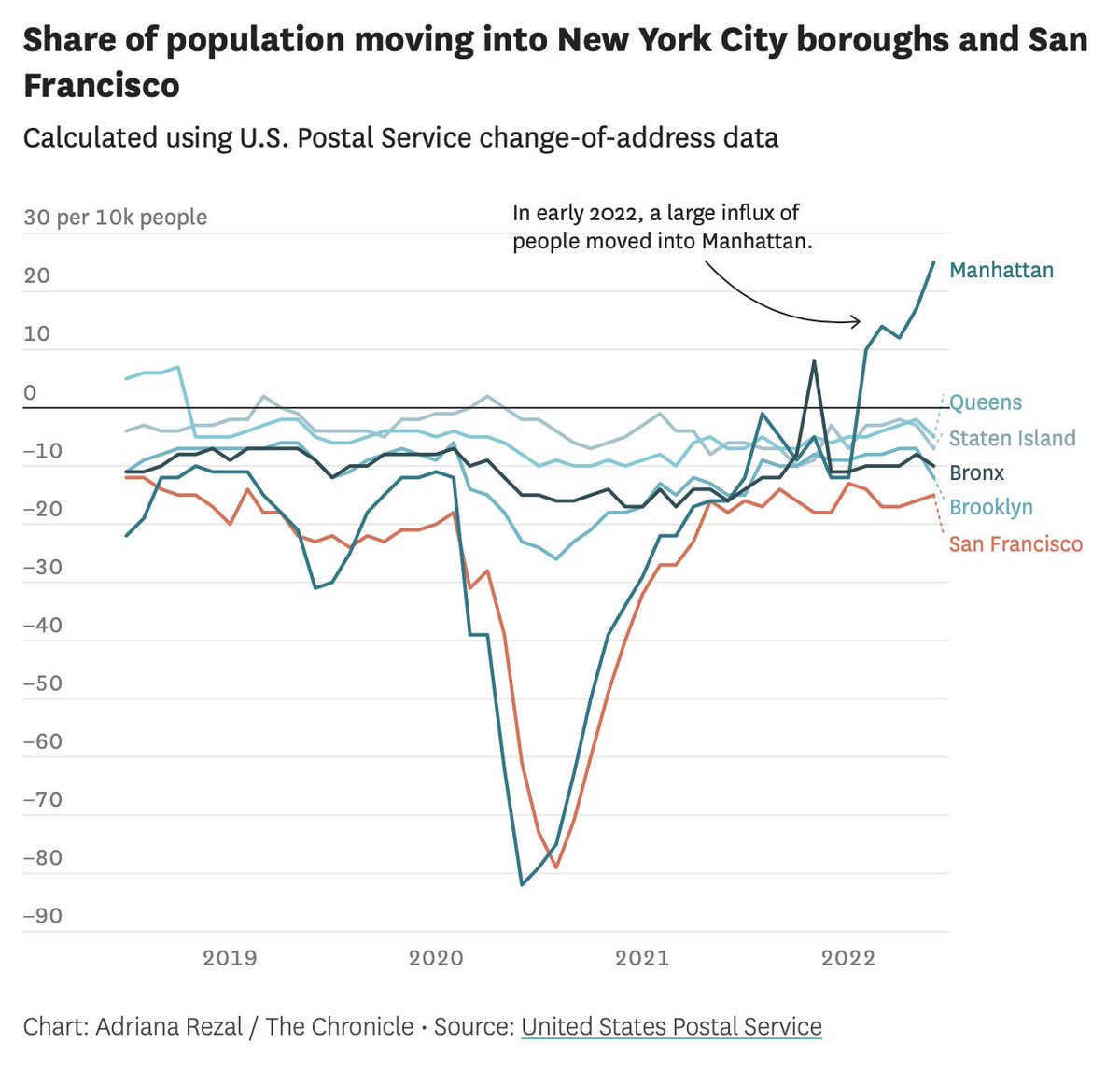

rate of San Francisco, which had fewer than 1,000. (But) more people are moving into Manhattan than before the pandemic. Manhattan median apartment rent hit a record of $4,150 per month in June, up 40% from fall 2020. "There are people living in New York who aren’t working in New York.” San Francisco is the only major U.S. city where rent still is belowpre-pandemic levels. Return-to-office mandates (in NY) forced residents to return. San Francisco’s more

lenient work-from-home allowances haven’t led to a similar rebound. (And) San Francisco’s tourism collapse was more severe than New York by many measures.

On a scorching summer evening, humidity choking the city, thousands of sweaty visitors lined up to ascend almost 1,400 feet.

Children squealed in delight as they disembarked on the 57th floor Summit observatory at the One Vanderbilt tower, all of Manhattan unfolding in front of them through glass windows, from the delicate, silvery tip of the Chrysler Building to One World Trade Center catching the setting sun, a symbol of the city’s rebirth from the terrorist attacks of Sept. 11, 2001.

San Francisco also knows how to attract people during these bizarre times — takeOutside Lands,for instance — but there’s a difference between an annual extravaganza and, in Summit’s case, a typical Monday. Lethargic downtown San Francisco lacks the energy and sheer mass of daily locals and tourists who have reinvigorated Midtown Manhattan and beyond to provide a sense of how life in this metropolis used to be.

There’s always been a disparity — New York has 10 times the population of San Francisco, which is a blissful 30 degrees cooler this summer — but the coastal tourism and economic hubs have diverged in striking ways as they recover from the pandemic. That’s despite grappling with similarly high costs, rising crime and stubbornly slow returns to the office that both rank among the nation’s worst.

One Vanderbilt epitomizes the different recovery trajectories. What is now New York City’s fourth-tallest tower was completed during the height of the pandemic at the cost of $3 billion, receiving its Temporary Certificate of Occupancy on Sept. 11, 2020, 19 years after another crisis. Its enormous 1.7 million square feet of office space is about 98% leased, with some of the highest rents in the city and only two floors available. Meanwhile, a slew of planned office projects inSan Francisco are stalled,and existing buildings struggle to find tenants.

From its opening in October 2021 to July 2022, Summit welcomed 1 million visitors. New York officials expect overall tourist volume to reach 85% of pre-pandemic levels this year, edging out San Francisco’s forecast of 83.5%.

The size of the crowds is jarring, considering New York was once the country’s coronavirus epicenter, with more than 41,000 deaths, or 0.5% of the population. It had five times the death rate of San Francisco, which had fewer than 1,000 deaths.

And residents fled both cities. In the first 15 months of the pandemic, New York lost 300,000 people, mostly to out-migration. Manhattanlost 6.9% of its population,or 117,375 people, from April 2020 to June 2021, a more severe drop than San Francisco,which lost 6.7%,or 58,764 people.

Despite San Francisco’s relative public health success and New York’s catastrophe, the East Coast metropolis is bouncing back stronger.

In 2022, more people are moving into Manhattan than before the pandemic, a major contrast to the four other New York boroughs and San Francisco, which are still seeing net losses, according to U.S. Postal Service change of address data reviewed by The Chronicle.

Manhattan median apartment rent hit a mind-boggling record of $4,150 per month in June, up around 40% from fall 2020, a sign of surging demand, according to real estate brokerage Douglas Elliman. Apartment vacancy peaked at 6.1% in October 2020 and was down to 1.3% in February of this year.

The market was like a faucet that was “dripping, dripping, dripping. Someone took a sledgehammer to the faucet and it exploded like a fire hydrant,” said Janna Raskopf, a top Douglas Elliman broker in New York.

In contrast, San Francisco is the only major U.S. city wheremedian rent still is belowpre-pandemic levels, and that’s after losing its title as the country’s most expensive rental market to New York last summer.

So, why has New York come back stronger?

City veterans credit a critical mass of return-to-office mandates that have pushed, and in some cases forced, former residents to return. San Francisco’s more lenient work-from-home allowances haven’t led to a similar rebound.

New York’s economic engine, Wall Street, has done far better than in earlier recessions and been more eager to return to the office than the tech industry. And Manhattan’s tech sector is no slouch either, seeing more office growth during the pandemic than San Francisco. Facebook, Google and Apple have huge expansion plans concentrated on Manhattan’s booming west side.

Despite canceling a second headquarters in Queens, Amazon has grown to become New York’s second-largest private employer with about 20,000 workers, mostly in warehouses, said Kathryn Wylde, CEO of the Partnership for New York City, the top business advocacy group.

“The city is constantly reinventing itself,” Wylde said. “It will flourish.”

There’s still a long way to go. Many Manhattan storefronts remain empty. New York’s offices are seeing only 40% occupancy, one of the weakest rates in the country and barely better than the San Francisco metro area’s 37.5% as of last week,according to Kastle, a building security firm.Transit has had an uneven rebound, with the New York region’s subways, buses and rail ridership rising to 69% of pre-pandemic levels in June, compared with San Francisco Muni’s 64% and BART’s 42%, according to the National Transit Database.

But New York has endured previous crises like 9/11, the 2007-08 recession and Superstorm Sandy, and it appears to have survived the worst of COVID.

“We have weathered, over hundreds of years, lots of constant struggles and setbacks,” said Jessica Lappin, president of the Downtown Alliance, which advocates for Lower Manhattan. “What we’ve learned from that is it takes a long time, sometimes, to recover.”

Flight to quality

One Vanderbilt owner SL Green, New York’s biggest office landlord, has benefited from the twin revivals of tourism and the office market. Last month, 6,400 people visited Summit in one day, and it’s on track to generate up to $25 million in net operating income this year.

And that’s not even the most lucrative part of the building.

The tower’s office space is 2% vacant, far better than Manhattan’s 21.5% vacancy rate, which doubled during the pandemic and is the worst on record. Manhattan’s rate is almost identical to San Francisco’s 21.7% vacancy rate, according to real estate brokerage Cushman & Wakefield.

Office experts call it a “flight to quality.” In the age of hybrid work, tenants want the fanciest interiors, coolest conference rooms and impressive outdoor decks. With many firms in tech and finance enjoying record profits during the pandemic, they’re willing to pay up.

“The biggest change is the tenant migration to better quality buildings. This is true at all levels of the market and not exclusive to new construction,” said Steve Durels, SL Green’s director of leasing and real property.

One Vanderbilt’s top office floor wasreportedly leasedwith an asking rent of $322 per square foot annually, probably a New York record and more than quadruple the market average. Across its office space, the tower is set to collect hundreds of millions of dollars in rent revenue a year.

Unlike the Bay Area, New York has not seen major companies downsizing or moving their headquarters to other cities, said Lori Albert, New York director of research at Cushman & Wakefield. “Attracting talent is what they need to do. That’s why they’re moving to these prime locations” like One Vanderbilt, she said.

Manhattan is expected to have an additional 10 million square feet of new office construction completed this year, a sign developers are still bullish, but also a trend that will increase vacancy.

In contrast, San Francisco has seen almost no new office development during the pandemic, and leases have been canceled at major projects like Pinterest’s deal at 88 Bluxome, where construction never started. Tech firms includingSquareandTwitterhave downsized offices.

San Francisco has been outperformed by Silicon Valley’s office market, and the biggest tech companies have been growing more rapidly outside of California.

“The real challenge is, what do we do with this office space that’s really not attractive to the market anymore?” said Nicole La Russo, real estate brokerage CBRE’s senior director of research and analysis in the region. It’s a question for both New York and San Francisco. One possibility is converting them to housing, which has decades of precedence around Wall Street but has beenmore challenging in San Francisco.

At least in Manhattan, it’s clear the demand is there.

‘It rebounded so quickly’

Raskopf, the Douglas Elliman broker, remembers when the New York apartment market turned.

It was April 2021, and then-Mayor Bill de Blasio announced city workers were going back to the office in June. Numerous private companies followed suit.

She got a call from a former New Yorker who had moved to Miami. He was being called back to work and was willing to rent an apartment without looking at it. Over the next 48 hours, she rented nine more apartments. In many cases the tenant wasn’t physically present, and would send a friend to scout or use video chat to do a tour.

“There was this sense of urgency I hadn’t seen in years: ‘I need to be here immediately,’” Raskopf said. “It was such a different mentality.”

The pace hasn’t let up.

Jonathan Miller, CEO of real estate appraisal firm Miller Samuel, said Manhattan rents fell as much as 30% in 2020 but have climbed about 40% from the bottom since that fall.

“What it’s suggesting is there are people living in New York who aren’t working in New York,” Miller said. “One of the byproducts of remote work is people are living in locations where they want to live, which may involve paying more rent.”

Raskopf is the leasing broker for 500 Manhattan apartments. During the depths of the pandemic she had around 65 open listings, and people were ditching apartments and breaking leases. Today only four are available, less than half of pre-pandemic levels.

She’s received 150 prospective tenants for one listing in less than a day, about 10 times the pre-pandemic level. During 2020 she was lucky to get two inquiries in a day.

She’ll talk to unlucky renters who are living in hotels with their belongings in storage because they weren’t able to secure a new apartment before their leases expired.

There’s an urgency fueling the frenzy that sounds familiar to anyone who tried to rent a San Francisco apartment during the pre-pandemic tech boom: bidding wars, lines spilling onto the street, “love letters” from prospective tenants to landlords with appeals to why they should be picked — which happen to violate the federal Fair Housing Act.

Many of Raskopf’s clients are ex-New Yorkers who decamped for warmer climates in places like Miami, Phoenix or Charleston, S.C. Even if workers are required to be in a New York office only two or three days a week, they still need to live nearby.

“I am inundated,” she said.

As downtown San Francisco struggles to revive and considersnew urban design efforts,there are lessons in Lower Manhattan, New York’s historic city center.

Since the 1990s, as Lower Manhattan lost companies to Midtown and the suburbs, there have been efforts to turn it into a mixed-use neighborhood and convert offices into housing. Some scoffed at the idea, but now having a “15-minute city” where work, housing and leisure are all within a short walk has become a global trend.

After 9/11, “thousands and thousands of units of housing were created in New York,” said La Russo of CBRE, who helped bring down the office vacancy rate. “It also helped the office market because it really revitalized the neighborhood.”

And it helped keep the area alive during COVID. Today around 64,000 people live in Lower Manhattan, up from 14,000 in 1995.

Housing conversions are happening again. The office tower at 55 Broad St., once home to Goldman Sachs, is planned to be converted into 571 housing units. And the landmark Woolworth Building, the world’s tallest building a century ago, has seen its top office floors converted to condos.

Lower Manhattan’s waterfront views; easy access to transit and Brooklyn, where many workers live; and cheaper rents were all lures for a generation of residents and workers. Lappin of the Downtown Alliance hopes those advantages help the area rebound from COVID. There are positive signs.

Near the middle of the week, the World Trade Center sees 70% office occupancy. Downtown hotels are seeing as much as 90% occupancy in July, better than expected.

New York Mayor Eric Adams’ office didn’t respond to requests for comment about the city’s recovery, but he has exhorted residents to go back to the office and get outside.

New Yorkers are only half-listening. AnApril survey of 160 major employersfound 38% of their Manhattan workers are in the office on the average weekday, and 28% are fully remote. The average attendance is expected to rise to 49% in September, with 14% staying fully remote, according to the poll sponsored by the Partnership for New York City.

Even as Wall Street and tech soared, the pandemic obliterated New York tourism, with visitor levels plunging by 67% and 89,000 jobs lost in 2020, nearly a third of the 283,200-person workforce in 2019,according to the state comptroller.

Today, Broadway is back, Times Square is jam-packed, and domestic visitors to New York are expected to fully recover by next year, with international following in the next couple of years.

“The city’s back in a big, big way,” said Fred Dixon, CEO of NYC & Company, the city’s tourism bureau.

Visa credit card data showed that New York’s domestic tourist spending in the second quarter was 99% of pre-pandemic levels, and international spending was 96%, he said.

San Francisco’s tourism collapse was more severe than New York by many measures: As the city’s biggest industry, tourism supported 86,111 jobs in 2019 and lost 65,000 jobs, more than 75%, in 2020, according to San Francisco Travel. SFOlost more passengersthan any other airport in the first years of the pandemic.

San Francisco’s forecast calls for 21.9 million visitors this year, 83.5% of pre-pandemic levels, but visitation isn’t expected to fully recover until 2024.

New York’s hotel occupancy, meanwhile, is 64.3% so far this year. And in six of the last eight weeks, New York has been the top hotel market in the country, Dixon said.

Meanwhile, at One Vanderbilt, the crowds keep coming. SL Green has shifted its development focus south to One Madison Avenue, another huge new office project that inked a huge lease with IBM.

“NYC will 100% recover,” said Durels of SL Green. “COVID is no longer a reason for businesses to avoid the office.”

As a Partner and Co-Founder of Predictiv and PredictivAsia, Jon specializes in management performance and organizational effectiveness for both domestic and international clients. He is an editor and author whose works include Invisible Advantage: How Intangilbles are Driving Business Performance. Learn more...

0 comments:

Post a Comment