Finance is a natural extension of Amazon's other businesses.

The companyalready collects massive amounts of financial data through its Amazon World Services cloud storage business, but the big money comes from pocketing for itself the fees credit card companies now take.

Financing big ticket purchases is an added financial incentive. JL

Spencer Soper and Jennifer Surane report in Bloomberg:

With a foray

into financial services, Amazon could disrupt the card payments system, a move that could save the retailer $250

million a year in swipe fees. That could be bad news for Visa Inc. and Mastercard Inc., as well as other players. Deeper hooks into the finance industry could help Amazon sell bigger items such as furniture (which) require financial products to help shoppers make purchases. Jeff Bezos changed the way America shops. Now, he wants to change how it pays for things.

With a foray into financial services, Amazon.com Inc. could disrupt the decades-old card payments system, a move that some say could save the retailer $250 million a year in swipe fees. That could be bad news for the likes of Visa Inc. and Mastercard Inc., as well as a host of other players.

Amazon is in early discussions with banks to create a product similar to checking accounts, people familiar with the matter said this week. Consumers with the account could link directly to Amazon and money could be moved using the bank-owned ACH network, for instance, with fewer fees. Amazon wants the account to appeal especially to millennials and those who lack bank accounts and credit cards, according to the people.

The plan, if it comes to fruition, is hardly an assured success. But few analysts think Bezos would stop there as he tries to expand Amazon’s reach into consumers’ economic life, pushing further toward things like car loans or mortgages.

Amazon already has links to some of its customers’ finances through co-branded credit cards it offers with JPMorgan Chase & Co. and Synchrony Financial. And the firm likes to target customers during big life changes to garner loyalty. It offers discounted Prime memberships to college students and services geared to new parents. Such data is potentially valuable to future banking partners, which could use the visibility to offer loans at the right time.

“You could see them definitely getting into that area if they find the right partnership” Tony DeSanctis, senior director at the financial consultancy Cornerstone Advisors, said in a telephone interview. “Banks don’t do a great job of leveraging spend and debit data today to create insights. If you think about what Amazon could do with that information even with a bank partner, there’s a lot of opportunity there beyond just the interchange play.”

Deeper hooks into the finance industry could also help Amazon as it moves to try to sell bigger items such as furniture. Such purchases could require financial products to help shoppers make purchases. The company launched a car research website in 2016, signaling a potential interest in selling cars.

Cost-Cutting Plan

Amazon’s plan doesn’t threaten to immediately dislodge credits cards because most shoppers have them, Bain & Co. analyst Maureen Burns said. Plus, younger customers “don’t have a lot of trust in banks," she said, estimating Amazon could grow the proposed checking accounts to 70 million users in five years.

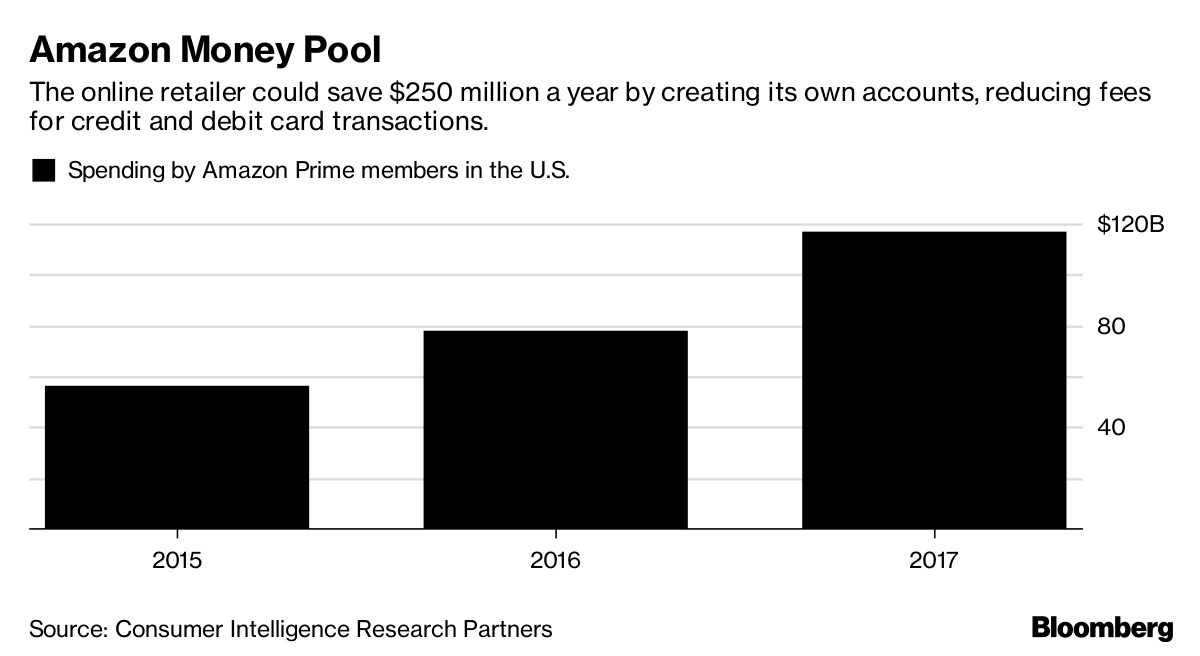

The risk to the $90 billion-a-year swipe-fee industry is larger if Amazon’s product resonates with young people who are wary of credit card debt or with members of Amazon Prime, the company’s most loyal customers who pay annual or monthly fees in exchange for shipping discounts. Members spent about $117 billion with the retailer in 2017, up 50 percent from the previous year, according to Consumer Intelligence Research Partners in Chicago.

Amazon declined to comment.

Winners, Losers

The world’s biggest online retailer would need to adhere to longstanding banking regulations, but the potential advantage is clear. If 15 percent of Amazon shoppers switch to its new account, the company could save $250 million a year in so-called credit card interchange fees, according to estimates by Bain.

The losers: payment networks like Visa and Mastercard, as well as the banks that issue credit cards and the intermediaries that help process payments, such as First Data Corp. and Stripe Inc. Those firms collect fees on each transaction, typically 2 percent for credit card transactions and 24 cents for most debit cards. “Everyone in the ecosystem is pretty much suffering with something like this,” said Dan Dolev, an analyst at Nomura Instinet. “Initially, it’s just a risk for whoever touches Amazon in terms of processing and acquiring. But down the road, if it sparks a trend and people’s usage patterns change because Amazon is just so present, then that’s a risk.”

As a Partner and Co-Founder of Predictiv and PredictivAsia, Jon specializes in management performance and organizational effectiveness for both domestic and international clients. He is an editor and author whose works include Invisible Advantage: How Intangilbles are Driving Business Performance. Learn more...

1 comments:

I think Amazon's foray into financial services could really shake up the industry and time card calculator

Post a Comment