Larry Light reports in CIO Magazine:

After the number of US malls peaked at 1,500 in 2005, mall closures have whittled them to 1,100. A quarter of the nation’s malls will be shuttered in the next five years. The US simply has gone too far in opening stores, with 23.5 square feet of retail space per capita, while Britain and Canada have 4.6 square feet. “We have a massive over-supply” of retail space. (But) sales growth for retail is outpacing US gross domestic product as a whole. Room exists for good stores to do well. (And)owners are transforming vacant spaces, especially in defunct department stores, into (fulfillment centers), movie theaters, restaurants, and medical offices.

The death of the shopping mall. Retail apocalypse. The triumph of clicks over bricks. Phrases like this are rife amid the retreat of physical retailers due to an Amazon-led online onslaught. This phenomenon is touted as a disaster for retail company investors—and the landlords who are faced with vacant stores.

A major shakeout is underway across the retail landscape, as iconic names of American merchandising wither. Dying off with them are numerous shopping malls, which used to be America’s town squares. Nevertheless, odds are good that, once the bloodletting is over, surviving malls and their stores will be fine, just different—a smaller and more practical collection of stores better suited to the modern era. And a solid investment, for a change.

When that happens, the extreme pessimism about this arena will seem overdone. “The headlines about a retail apocalypse,” said Ted Chang, a portfolio manager at Thornburg Investment Management, “were too bearish.”

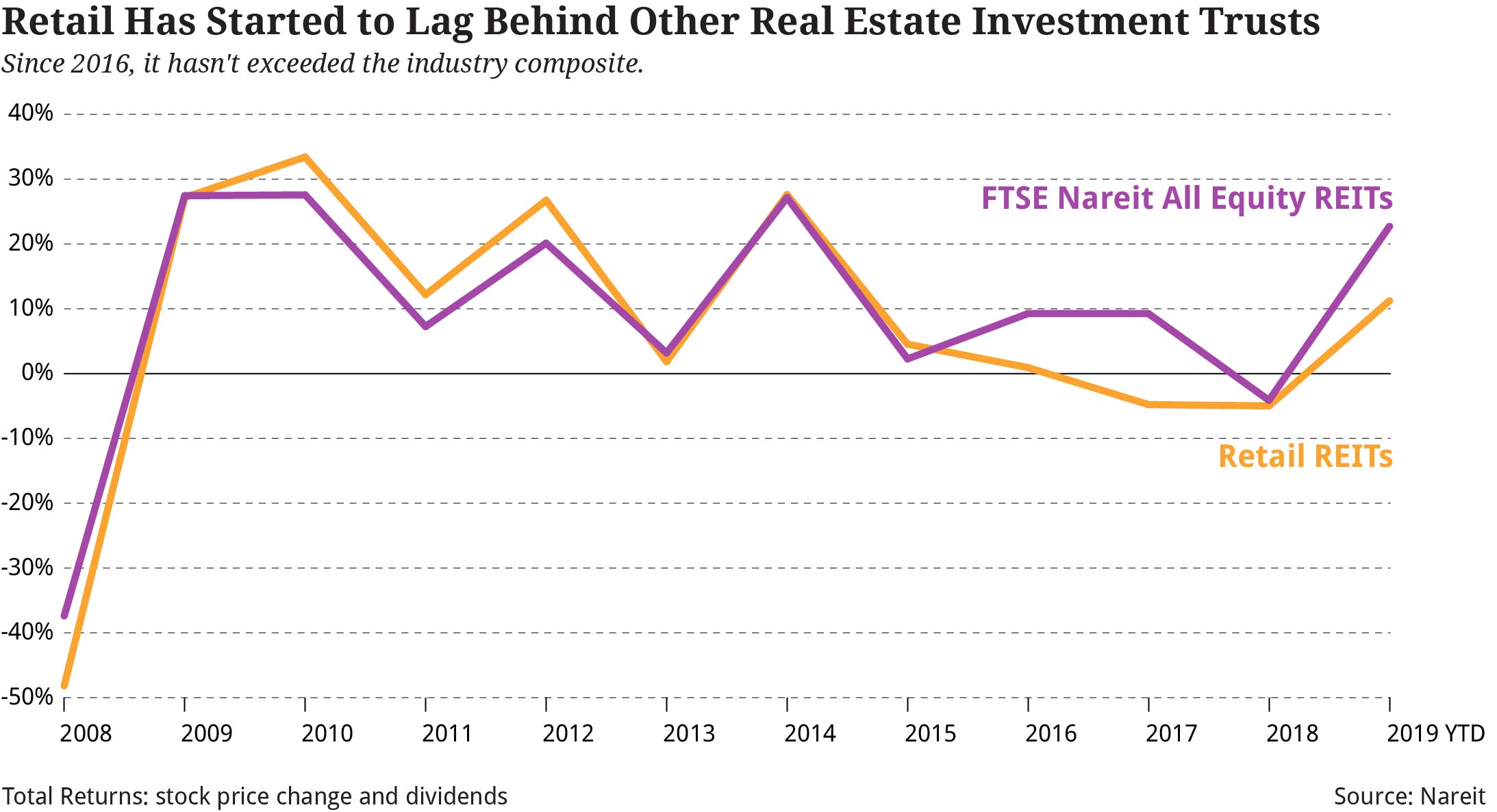

True, although retail property owners have come up wanting when compared to other investments, at least lately. Consider the trajectory of real estate investment trusts (REITs) specializing in retail, in terms of total return (stock performance and dividends). Coming out of the Great Recession, where they got slammed, retail REITs recovered better than the composite index for all REITs, by the reckoning of Nareit, the group’s trade association.

But the retail trusts hit an inflection point around 2016, when steadily growing e-commerce really took off. For the next three years, this subsector posted minimal or negative numbers, and lagged behind the all-REIT composite. At present, though, things are looking up. While retail trusts’ total returns are up about half as much as the composite this year, they’ve managed to post a respectable 11.24% gain.

The picture is the same for earnings. Using REITs’ preferred metric, funds from operations or FFO (net income plus depreciation and amortization), retail ones were up 6.8% over the 12 months ending March 31, compared to 31.9% for infrastructure, 28.1% for data center, and 16.8% for industrial REITs.

Retail Slaughter

To understand the direction of retail real estate, let’s first look at the ugly culling that’s taking place. Payless, Gymboree, Toys “R” Us: The list is mounting of bricks-and-mortar retailers going out of business. Add in a second list of struggling merchants that are still alive but paring back stores amid sales slumps, which Macy’s, J. C. Penney, Gap, and many others are doing.

Result: Malls are closing amid less foot traffic. After the number of US malls peaked at 1,500 in 2005, mall closures have whittled them to 1,100 lately. Credit Suisse estimates that a quarter of the nation’s malls will be shuttered in the next five years, concentrated on the lower end of the quality scale.

Regional mall vacancy rates edged up in this year’s first quarter to 9.3%, an increase from 9.0% in 2018’s final period, and 7.8% five years before, Moody’s Analytics finds. The carnage is most concentrated in the regional malls, vast enclosed spaces that typically have been book-ended by two major anchors, namely department stores like Macy’s or Penney. Strip shopping centers, usually sitting in the open air and featuring small outlets like nail parlors and convenience stores, have been hurt far less.

Meanwhile, throughout mall-land, the tenant base shrinks. Thus far this year, 6,986 store closures have been announced, which eclipses the number for all of 2018, according to Coresight Research. That sounds dire. There’s a mitigating factor, however: 2,985 new stores are opening, replacing almost half of the closings.

The US simply has gone too far in opening stores, with around 23.5 square feet of retail space per capita, while Britain and Canada have 4.6 square feet, respectively, Cambridge Associates points out. “We have a massive over-supply” of retail space, noted Nitin Sacheti, a portfolio manager at Papyrus Capital.

Some Positive Signs

The Buffett factor is often a good way to assess a promising if little-appreciated value investment, as the venerated investor Warren Buffett so often has been right. Despite all the gloom, Buffett’s Berkshire Hathaway last year discerned a bright spot in Sears Holdings, now in Chapter 11, and a classic example of the brick-and-mortar retail failure.

Berkshire made a $1.6 billion loan to Seritage, a REIT that contains 250 Sears stores, which it stands to acquire if and when the chain goes out of business. They don’t come any cannier than Buffett, so his maneuver suggests that those spaces will continue to have a useful economic life.

The creative destruction of capitalism is at work in the retail sphere. New venues rise up to replace the old and outmoded. Department stores and apparel outlets, at least those that haven’t kept up with the times, are endangered. Specialty retailers (like Home Depot), discount emporiums (Dollar General) and fast-fashion providers, which means designer clothing at cut-rate prices (H&M), are examples of those that have done well.

In addition, the mad mall-building days are over and few new malls are going up, noted Calvin Schnure, Nareit’s senior vice president for research and economic analysis. That means, he said, that “net absorption is positive,” a measurement of occupancy trends. This, in turn, has helped lead to the 11.24% rebound in REIT total return so far this year.

Aiding the improved performance are the ample dividends that retail REITs pay, at a lush 5% yield. (Malls owned by publicly traded REITS are slightly less numerous than those with private owners, 487 to 525, as of late 2017, Nareit figures show.) The mall crunch has affected lower-end properties the most, with ones in wealthier locales better able to do a rewarding business. “Malls in good locations still have a steady stream of tenants and customers,” Schnure said.

Among retail REITs, the bellwether is Simon Property Group, which has survived all the turbulence to remain the most valuable REIT ($109.5 billion), surmounting trusts in hotter areas like cell phone towers and warehouses. Its stock has been on the downswing since 2016, losing 24%, yet it has posted some respectable earnings. FFO per share in the first quarter was $3.04, an almost 6% improvement over the year-ago period’s $2.87.

The company doesn’t need department store anchors anymore, CEO David Simon told investors last year. The REIT has had to swallow the closing of 33 Sears stores. But it controls 17 of them, and plans to re-purpose the stores for other uses. “We’re going to redevelop this,” he said. “We’re going to generate positive momentum with the properties.”

Many mall owners are transforming vacant spaces, especially in defunct department stores, into such uses as movie theaters, restaurants, and medical offices. At its Phipps Plaza mall in Atlanta’s tony Buckhead section, Simon is converting the former Belk department store into a mixed-use facility with a new hotel, a restaurant, offices, an athletic club, and an outdoor entertainment venue.

Malls can be repurposed in all kinds of ways. “They should convert abandoned malls to senior living,” suggested Rosalind Hewsenian, CIO of Helmsley Charitable Trust, with enough retail to be supported by the residents and their visitors.

One additional grace note for REITs: The apparent stalling of plans for higher interest rates work in their favor. Since the trusts borrow lots of money to buy properties, lower-cost debt will aid their bottom lines.

Why Physical Retailing Will Thrive Anew

While Amazon and its ilk have undoubtedly made retailers suffer, they may not be an existential threat in the long-term. Indeed, e-commerce made up just 10% of total retail sales in this year’s first quarter, US Census data shows. That level is up from 4% in 2009. The question is will it plateau at some point.

A case can be made that being able to shop for certain products in person will retain its allure. Online offers the convenience of shopping at home, a larger selection of goods, and often lower prices. Nevertheless, the ability to touch, to try on, and to see first-hand are powerful trump cards for stores.

Consumers who ordered shoes or clothes digitally might find the goods, when they arrive, don’t fit. Or that chair whose photo looked so compelling doesn’t come off as well in the light of day, and is uncomfortable to boot.

Some brick-and-mortar merchandisers, like Walmart, are taking the war to Amazon. Walmart offers its own digital service that offers conveniences such as same-day store pickup. It even has opened a pilot program where its employees will enter your home when you’re away and put food in your refrigerator. How consumers will cotton to strangers gaining access to their unoccupied dwellings remains to be seen.

Food is a huge part of Walmart’s online business, and by year-end, the company aims to have 1,600 stores able to deliver food, and 3,100 grocery pick-up points.

While Amazon comprises half of all US e-commerce sales, Walmart is gaining share. In 2018, it elbowed aside Apple to become the third-largest online retailer in the country, behind Amazon and eBay, stats from eMarketer indicate. The market research group predicts Walmart will end 2019 with a 4.6% share of the US e-commerce market, up from 4% last year.

More broadly, absent a recession, the retail pie is growing, which allows room for physical retailers who know what they are doing and can lure customers. US consumer confidence still is healthy. Overall retail industry sales including online rose 4.6% in 2018, and should expand between 3.8% and 4.4% this year, the National Retail Federation says.

As Coresight points out, sales growth for retail is outpacing US gross domestic product as a whole. Upshot: Room exists for good stores to do well.

If malls and kindred retail venues can cater to 21st century consumers’ tastes, the natural desire to be around others is a powerful advantage that has the potential to give a rebirth to malls and other land-based retail venues. As Thornburg’s Chang put it: “People still want to congregate in areas that are compelling.”

1 comments:

Thanks for interesting share about the trend of real estate market. Most of real estate agents is confusing about the 2020 real estate market. It can be a hard year for all of of.

Alice

Real Estate Content Writer

Post a Comment