But what does that mean? The fact that it dominates ecommerce and continues to muscle other companies out of its way suggests it wants - and can - be even bigger. The question for regulators is how big is too big. And the answer may ultimately lie in the eye of the beneficiary or victims. JL

Benedict Evans reports in his Blog:

Amazon is a big company. But how big? Hundreds of billions are thrown around, but is that big in relation to US retail? What should we compare it to? Amazon has 35% of US ecommerce. But, it competes with physical retailers as well. On that basis, Amazon’s real market share is closer to 6% (it’s 2/3 the size of Walmart). Walmart was also once the bogeyman of terrifying efficiency and scale but also failed to crush all other American retailers. Amazon won’t either. If you think Amazon will go towards taking over ‘everything’, then your definition of Amazon’s market share has to be its share of, well, ‘everything’. Today, that’s around 6%.

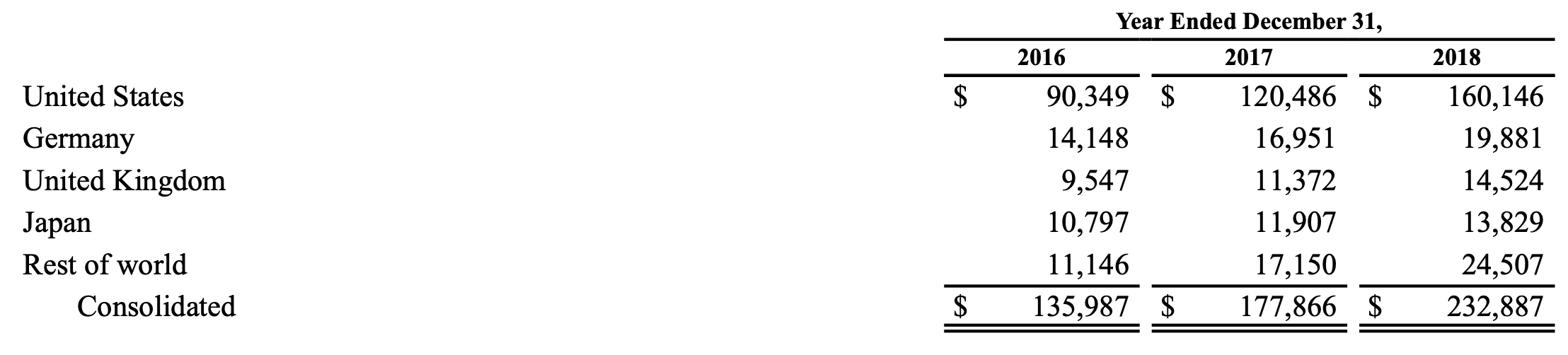

Amazon is a big company. But how big? Numbers of hundreds of billions of dollars are thrown around, but is that big in relation to, say, US retail? What should we compare it to? We often hear that it has ‘huge scale’, and maybe it’s ‘dominant’, or even ‘a monopoly’, but what does that mean? What is Amazon’s real scale, and what is its market share? This might sound like an easy and perhaps boring question to answer, but if we’re going to talk (and worry) about a company’s size, we should probably want to know what size we’re actually talking about.So, to begin: market share in principle is Amazon’s business divided by the total market. If we want to do that for the USA, what are those numbers?Well, Amazon discloses its revenue by country, and US revenue in 2018 was $160bn.

However, only 53% of Amazon’s total revenue is the actual direct ecommerce business. 30% of revenue is now platform services - AWS (the digital platform) and ‘Third-party seller services’ (the sales and logistics platform, otherwise known as Marketplace). Another 10% comes from ‘Other’ (mostly advertising) and subscriptions (Prime), and then there’s the ‘physical stores’, which today is almost all Whole Foods (the revenue number in the table below jumps from 2017 to 2018 because Amazon only owned Whole Foods for part of 2017.Amazon doesn’t actually tell us the splits, but we can make some reasonable estimates. Whole Foods is almost all in the USA. If we exclude the stores, ~66% of Amazon’s revenue is in the USA, and it seems reasonable to assume as a starting point that the same proportion of ecommerce is also in the USA. On the other hand, you could also guess that AWS, Prime and maybe advertising have a larger proportion of their business in the USA, meaning US ecommerce would have to be smaller to make the maths work, but we don’t really know. So, let’s fill in the table on the basis of that 66%. These assumptions give us $81.5bn US ecommerce, but you could very easily flex it $5bn up or down. Now let’s come back to that ‘third party’ thing. Amazon lets other companies list products on its website and ship them through its warehouses as the ‘Marketplace’ business. It charges them a fee for this, and it reports the fee as revenue. That’s the $42.745bn. But, Amazon doesn’t treat the value of the actual purchases as its own revenue, which is in line with US accounting rules, since technically Amazon is only acting as an agent. So, if you buy a $1,000 TV on Amazon from a third party supplier, Amazon will charge the supplier (say) $150 in fees for shipping and handling and commission, and report $150 as third party service revenue, but won’t treat the $1,000 as Amazon revenue at all. eBay has the same accounting policy, but it also reports the value of the actual purchases as a separate number - ‘gross marketplace value’, or GMV. In the past Amazon didn’t disclose its GMV, but in the 2018 shareholder letter it finally gave a bunch of rounded numbers: global first party sales were $117bn (note this is slightly different from the $123bn above, given in the formal accounts in the same report), and global third party sales were $160bn, giving global GMV of $277bn and meaning that 58% of global Amazon ecommerce is actually made by third parties using its platform, not by Amazon itself. To repeat: Amazon doesn’t treat that $160bn as its own revenue and so it’s not in the revenue tables above - it only reports the $43bn of fees for handling it. But clearly, this belongs in any discussion of Amazon’s market share. (As an aside, one should note that the revenue from the third party platform services business is almost twice that of AWS, and certainly pretty profitable; Amazon discloses revenue and profitability for AWS but only revenue for this. Remember that the next time you see someone claiming that AWS subsidises Amazon.)So, we need to consider both Amazon’s own sales and the value of third party sales (together, GMV) in market share, and again we know the global number but not the US number. However, if we assume the same 66% split, and switch to using the $117bn ecommerce number instead of $123bn, that means that in the USA in 2018:

There are other things inside retail that you might also want to exclude from ‘addressable retail’ (building materials are $335bn, say). But another important strand is that a regulator doesn’t just look at the share of ‘retail’ (however defined), but at the share of particular segments, and it chooses what definition it wants to use depending on the problem it thinks it’s addressing (and this is a political question, not just an economic one). Amazon has 50% or more of the US print book market, and at least three quarters of publishers’ ebook sales (it also has its own ebook publishing business, for which it has never disclosed any data). Walmart has 9% of ‘addressable retail’, but 20% of grocery sales (and in a small number of US cities it has over 50%). Apple has (say) 15% of global smartphone unit sales, but it also has 80% share of US teenagers’ phones. That is, a central part of the regulatory process is ‘market definition’, and in the past the EU has defined Microsoft as having dominance of the market for ‘commercial third party PC operating systems’, and Google Play as having dominance not in ‘app stores’ but in Android app stores.A cynic might say that this is a bit like deciding that Ferrari has a monopoly on Italian sports cars made by companies whose names begin with ‘F’. But if you do it right, then you focus on the market that actually matters. If Amazon was still ONLY doing books, and it had even 90% of the US consumer print book market, that is still only 0.2% of US retail. That clearly wouldn’t mean it wasn’t dominant in the ‘relevant market’.Finally, of course, Amazon is growing. Its US ecommerce business probably grew 20% in the last year, and so its market share of total and of addressable retail is going up. Hence, you could argue that since ecommerce is clearly going to take over a much larger share of retail, and since Amazon has a large (35-40%) share of ecommerce, Amazon’s strength in ecommerce means it will swallow everything else, even if it’s only at 5-6% today.This is a coherent argument, but not a complete one. I don’t think one can just assume that Amazon’s market share of online sales will be maintained indefinitely in a straight line into the future. The more that ecommerce expands beyond the original commodity categories, the more that we see new and different models and experiences proliferating. Shopify, another platform for online retail, is now at an annual run-rate of $60bn of GMV, up from nothing five years ago. As I’ve written elsewhere, I don’t think Amazon is well suited to create proliferating models - it has to do almost everything in the same way. Indeed, the very concept that one retail format can swallow all others seems flawed to me - department stores did not, nor supermarkets, not Walmart, which was also once the bogeyman of terrifying efficiency and growth and scale but which also somehow failed to crush all other American retailers. Amazon won’t either.

Still, if you disagree, and do think that Amazon will go much further towards taking over ‘everything’, then your definition of Amazon’s market share has to be its share of, well, ‘everything’. Today, that’s around 6%, not 35% or 50%.

0 comments:

Post a Comment