Like most gold rushes and bubbles, too many people get in too late to prosper. And the sharks always attracted to speculative investments create both too much competition for the available resources as well as too little value to be harvested.

The recent 50% drops in cryptocurrency values in the past week are symptomatic of the larger trend. JL

Vanalli reports in The Startup:

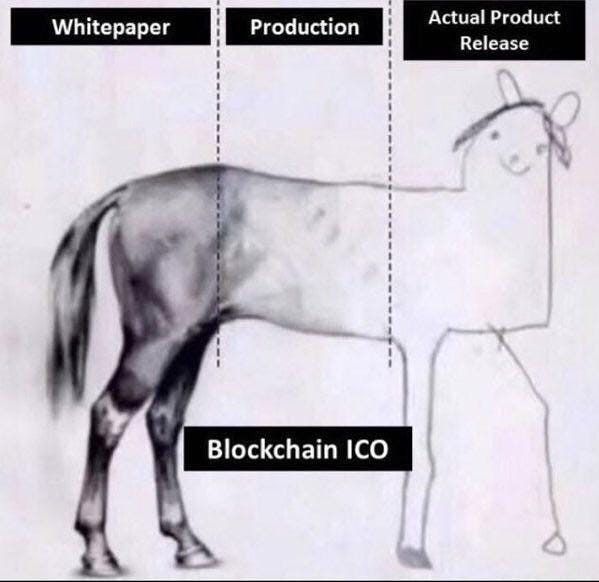

Most crypto projects shouldn’t exist. If they’re not outright scams, they’re cash grabs, a last-ditched attempt to sell a token that will never be used

for the utility outlined in the whitepapers written. Use cases are tenuous. Once the funds have been

raised, teams cash out or mismanage the money

until they bleed themselves dry. The relationship between crypto project and community is entirely

contrived. People base their crypto beliefs on

tokens they are invested in. (There're) half a dozen useful cases for blockchain in the top 1,000 cryptocurrencies. There are thousands of

projects, few

focused on products people will use. Most will lose the majority of their value.

When I started working full time in crypto I thought it was the coolest thing ever. It felt like I was part of the ultimate disruption of the financial world. Long Bitcoin! Short the bankers!Buy the t-shirt!

But after being in the space for a couple of years, I just wanted to get out (and get out I did).

The crypto sector is a mess and in need of a reality check. What gives me the right to call out an entire space? Not much, truth be told. I worked for a crypto company, Liquid, and formed my own opinions, though this blog is less about the company I was employed by and more about crypto as a whole. Either way, I invite you to read what I have to say and then let’s have a conversation about the points raised.

Almost All Crypto Projects Are Complete Bullshit and Will Fail

I didn’t believe it when I first heard people saying that most crypto projects will fail.

Boy was I wrong.

I’ve lost count of the number of projects I’ve seen fail. Some went out with a whimper, simply dying quietly while the team hoped nobody would notice. Blockex, a project I followed closely for a while, was a digital asset exchange focussed on ICOs. A token, $DAXT, gave early access to these ICOs, while the platform also had regular trading pairs.

At one point in 2018, Blockex was a hot commodity. Crypto influencers heavily shilled the project. Blockex raised 24 million USD in their own ICO, although in the end they only received about 5.5 million GBP (around 7 million USD) after an investor failed to come through. The project barely got off the ground and last we heard they’d quietly gone into liquidation. The token, meanwhile, which sold at ICO for 1 euro a piece, ended up going to zero.

Another that caught my attention early was Authorship, a seemingly innocent project aimed at supporting authors that ended up raising 4 million USD to create a decentralised, digital publishing platform. At some point the founders, Nolan Warfield and Petre Coman, realised they’d made a horrible mistake and abandoned the project (they basically created an ugly ebook store), selling it to a Chinese investor who similarly ended up giving up on it. The token, of course, went to zero.

One final example: I did some marketing work for a project called IP Chain, later rebranded to Vaultitude, operated by an Austrian businessman named Dominik Thor, who is also the CEO of a cosmetics company, tomorrowlabs. I met Dominik online as he was trying to build a team for his project before an ICO. At that time in 2017, you could have put potatoes on the blockchain and done an ICO and it would have made millions. I was to be paid a healthy sum, in Vaultitude tokens, of course.

The project was to build a platform that harnessed blockchain to allow people to protect their intellectual property. It was a decent use case (or so I thought at the time) and Dominik had a lot of connections with IP heavyweights like Dennemeyer and even the World Intellectual Property Organization.

We did a presale and raised a modest sum, but Dominiik subsequently burned through that by flying around the world to attend and speak at various conferences and events. Eventually it became clear that Dominik had run out of money and that there was little interest in an ICO we couldn’t afford to do anyway. I never got paid for the hours of work put in (more fool me) and last I saw, Dominik had pulled a swift exit, deleting the project website and any of the social channels he had access to, along with his own Twitter account and Linkedin profile. Hindsight is a wonderful thing.

Crypto is full of curiosities like these.

Expectation vs Reality

Many projects that seem “good” (or at least, not terrible) in a whitepaper and maybe even complete a successful ICO, soon find that their ideas aren’t that great after all. While the teams may work hard and try to soldier on through the bear market, they are more often than not flogging a dead horse.

Leadcoin, for example, raised 50 million USD to build a platform where marketers can buy leads. Few people at the time questioned why they needed so much money. Two years down the line, almost all the project’s team members have left (compare the original team with their Linkedin accounts; see how many Leadcoin staffers there are now on Linkedin). The one remaining staffer, Chief Marketing Officer Eyal Rosel, runs the Telegram group, providing inconsequential updates every three months to perpetuate the illusion that the project is alive.

The token lost 99% of its value after being delisted from every exchange except Bancor, which has a number of dead projects listed (including Authorship).

A lot of projects end up failing more spectacularly than Leadcoin, either through being outright scams or just suffering at the hands of gross incompetence or general misfortune, or a combination of the above. The truly impressive blowups are always the most fun to watch, in a car crash sort of way — and boy have their been a lot of car crashes. When Bitconnect turned out to be a massive ponzi scheme, there was a monumental fallout that saw people lose millions of dollars while a new generation of memes was born.

Shopin was another one. After raising more than 40 million USD, the founder, Eran Eyal, was last year arrested on charges of fraud before being hit with new fraud charges by the SEC in December, putting the final nail in the coffin of a calamitous project that ended up screwing everyone over.

So most projects fail. This isn’t unique to crypto. It’s true of startups in general. But I’d be willing to bet that crypto has a higher proportion of failures than the average for startups. Most crypto projects are just straight-up garbage.

Welcome to Startup Hell

Projects end up failing for a variety of reasons. But the one that really stands out is that most crypto projects shouldn’t exist in the first place. They’re pointless. If they’re not outright scams, they’re normally cash grabs. We’ve seen pretty much every niche and possible use case, from tokens for cosplayers and “stans”, to collectible cats, endless dice games under various guises, dogshit blockchain games and much more.

Genius.

Every sector has had a crack at going on the blockchain — HR, marketing, food production, content sharing, gambling, blogging, ratings, journalism, publishing, lending, social media, pet care, shopping, commerce…

Almost always it’s a last-ditched attempt to fleece retail punters out of millions of dollars, selling a utility token that will never be used for the utility outlined in the abundance of whitepapers that have been written. These utility tokens are also extremely volatile assets. Most will lose the majority of their value. There are now thousands of projects with thousands of different tokens, with surprisingly few focussed on building products people will actually use.

We don’t need all these projects. Use cases we’ve seen are tenuous at best. Once the funds have been raised, teams either cash out, profit or end up mismanaging the money until they bleed themselves dry. I would challenge you to find more than maybe half a dozen actual useful use cases for blockchain in the top 1,000 cryptocurrencies. It’s a con almost every time. ICOs were and still are a scam—and yet they still happen to this day.

We have so many different blockchain platforms now, so many ecosystems, so many tokens providing the “fuel” for those ecosystems, when in reality, the platforms could have worked just fine without a new token.

It’s All About the Money

ICOs are cash grabs and the user experience ultimately suffers. How many video and content platforms do we need with a token that grants people “access to special content”? How many crypto platforms do we need at all really?

Look at BlockTV, a reasonably successful crypto online TV channel. They seemed to be doing just fine before they announced they were raising 2 million USD in an ICO (that wasn’t an ICO), despite the founder’s previous ICO efforts (Stox and Sirin Labs) losing 99% of their value.

It’s often overlooked that such tokens and applications of blockchain usually degrade the user experience. Projects expect users to jump through numerous hoops just to get access to and use their platform.

Here’s roughly what a new user is expected to do:

Research how to buy Bitcoin.

Find an app to acquire Bitcoin.

Move the newly bought Bitcoin to a crypto exchange.

Exchange Bitcoin for a utility token.

Sign up on the utility token platform.

Move utility token to platform or learn how to use Metamask or some other service.

Learn how to use the platform itself.

For a newcomer, this is a lot of legwork. Sometimes when they realise this, project teams will go so far as to allow users to actually bypass even needing the token to pay for features and services in the first place. It’s nonsensical.

Do these projects earnestly expect their users to go through some roundabout process to acquire tokens (the process is never straightforward) and then learn how to use them on the platform? No, they don’t. They know it’s futile. They just want to raise money and continue to work under the illusion that they’re doing something worthwhile.

A few of these project teams may have the best intentions, I won’t deny that. They may truly believe that they’ve found a unique application of blockchain that is going to improve their sector, but the reality is that they don’t have the capacity to actually deliver something that is going to make an impact and as a result, they end up creating solutions for problems that don’t exist, making more problems than they had to begin with, especially for the users.

If we’re looking at cryptocurrency as a form of digital cash, then sure, that’s a use case we can all get behind, but do we really need hundreds of different forms of digital cash? Do we expect vendors to accept all these tokens? It’s just creating more clutter.

Crypto Communities Are Cesspits

Most crypto projects are pointless, despite the billions of dollars raised in ICOs, but we should also discuss the backbone of any crypto project: the community. The relationship between crypto project and community is entirely contrived. For a start, people tend to base their crypto beliefs on tokens they are invested in (rather than the other way around). They become zealots. Maybe on the surface this doesn’t sound so bad, but investment is driven almost entirely by outrageous expectations of profit.

People put money into tokens they believe will increase in value exponentially, hoping for a repeat of what we saw with Bitcoin, Ethereum, TRON, Verge and many others in the past. Given how manipulated and immature crypto markets are, you come to understand that price action is irrational. There was a time when something as mundane as a rebrand could cause the price of a project’s token to skyrocket. So people invest hoping to make big money, then more often than not, their investment decreases in value and they continue holding the token. It’s at that point they usually join “the community”—the bottom of the food chain.

Near the top are the shills, influencers, early investors and VCs who have vested interests in creating hype and price action. These ringleaders work hard to mislead retail investors into believing that their token of choice is a great investment. At the very top, there are the founders and team members who are happy to ride the waves and create money out of thin air.

It’s toxic. All of it.

Project teams and their mouthpieces do their best to convince others that they should “invest” in their token. I use the term invest here lightly because when you buy a token, you’re not buying equity in the company. You’re not really buying anything. All you’re getting in return for your funds is a token with a contrived use case that you’ll never even use it for.

All kinds of tactics are used to build a community around a project (usually without even a product). Some may join a community because they’re interested in the kind of project, but most others will be drawn to the lights by influencers, YouTubers, PR, press, crappy YouTube videos and other shiny objects.

Teams spend as much money as they have on getting users into their Telegram groups, enticing them with shitty bounties, meme contests and quizzes. For a while it seems like everyone is in it together. People are excited, looking forward to the token sale, and then looking forward to that first listing on a crypto exchange. They think they’re all going to make money and be rich.

But at some point the relationship between project and community falls apart. It can happen before the ICO. It can happen a month after, a year, sometimes two years, but inevitably, with any crypto project and community, it will go to shit. Why? Because there is no real link between the community and the project. It’s all built on bullshit.

Further compounding these issues is the rampant sexism, racism, misogyny and intolerance on display in crypto chat rooms and online spaces. It’s worth noting that the vast majority of people in crypto are (often anonymous) men. Women have been targeted with online abuse and harassed. There are relatively few female leaders in the space. Most crypto conferences field all-male panels, like the special example below that literally couldn’t have squeezed more men on a stage if they’d tried.

There are some amazing women in crypto. But they have had to put up with more bullshit and nonsense than any reasonable human being should have to endure.

The Community Always Comes Last

Most crypto projects have already offered their tokens to private investors at heavily discounted rates before any kind of public sale. That’s where the real money is made. Then along comes the community and they get to buy at a higher price and immediately put at a disadvantage. But beyond that, the project team only needs the community to raise funds. Once the money is handed over, that’s when the real nonsense begins and project teams have to keep up appearances by providing just enough updates and AMAs and morsels of meat to feed the hungry mouths.

The goal is to keep spirits high enough so that there isn’t a public outcry about how the team has stopped providing updates on development of the roadmap seen in the whitepaper.

It’s the same every. damn. time. Gradually, the community will start to become unsettled, unhappy with progress, and this will mutate into anger, with frequent outbursts in Telegram or on Reddit. Then comes a level of acceptance as most people either cut their losses or decide to hold onto their tokens until they go zero.

The only thing the community is really interested in is the price of the token. They couldn’t give a shit about the tech. They simply want to sell their tokens at a profit. But the team has no obligation to the community to deliver on any kind of roadmap or keep the project active, although there have been a small number of class action lawsuits and charges filed by the SEC.

Project teams will sometimes do their best to get listed on big exchanges (for hefty listing fees), to build hype, to work with market makers, to try and ensure that the token gets pumped at some point so early buyers can exit, but with the nature of how volatile crypto is, there will always be those who don’t sell, those who buy the top, those who hold when they should have sold. Community members cling onto the hope that one day they’ll be able to sell their tokens and make a huge profit, make a small profit, break even or just not suffer a massive loss. People become emotionally attached to their communities and it creates a cycle of despair that can go on for years.

Some community members will eventually realise the fallacy of this attachment and begin to understand that crypto is a place to make money as a trader, and that to do so you really need to become project agnostic. Then, it doesn’t matter what token you buy, so long as there is a short term upside. The worst thing you can do is end up holding a token for months for no other reason than you thought it would eventually go up in value.

We had so many overhyped projects in 2017 and 2018 that created these nonsense communities. I joined literally hundreds of Telegram groups over the past two years, mostly for work, sometimes as a potential investor myself. Now when I go back to take a look at how they’re doing, I see that the optimism has evaporated and there are now countless posts asking for updates from the team, who are usually trying to figure out how to break the news that they’ve completely run out of money (the curse of running a company with no revenue streams).

Electrify Asia, Apex, Auctus, Zap, Soma, OCN, CNN, Gems, Internxt, Hero… there were hundreds of projects that were hyped to the moon over the past couple of years. People poured millions into them while the tokens all went to zero or thereabouts. Almost all of these crypto projects should never have existed and certainly shouldn’t have raised funds with an ICO.

Join Our Cult

Crypto communities are irrational and cult-like, especially the larger ones. They are territorial, willing to defend their tokens against any criticism or scandal that comes their way. They look out from rose-tinted glasses, ignoring red flags and repeating the nonsense of their cult leaders.

Few people stop to wonder if it’s really worth having all these different, seemingly competing communities. Isn’t there some kind of greater good?

Not only do investors become aggressively, emotionally attached to their tokens, but they elevate founders, CEOs, CxOs and leaders within the space to near godlike status. Justin Sun (founder of TRON), CZ (founder of major crypto exchange Binance), Charlie Lee (creator of Litecoin) et al are celebrities now.

The crypto rich and famous have been able to build a brand around being the “good guys”, in it for the community, contributing to a better tomorrow, when the reality is that most of them are are selling snake oil—or worse. The wider crypto community is, however, incredibly forgiving. There’s no scandal too big to be overlooked in the name of profit.

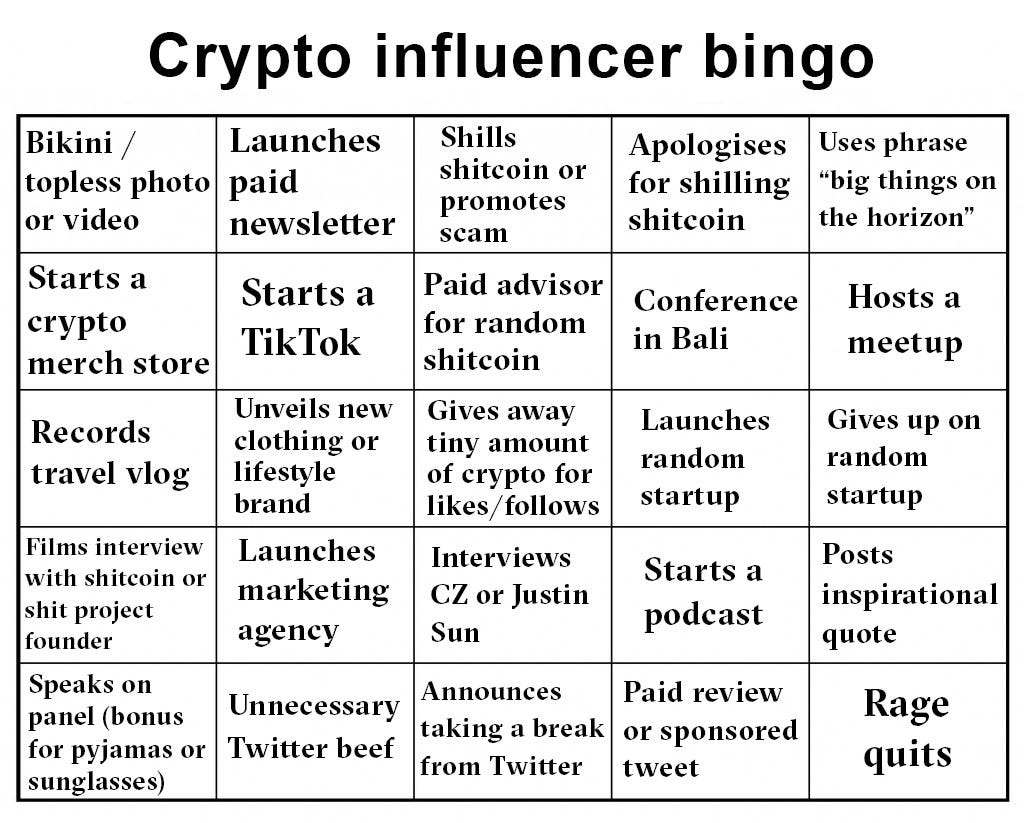

The Art of Wasting Everybody’s Time

Crypto content creators tend to fall into three categories:

Those who actually know what they’re talking about and add value.

Those who got crypto rich and decided to make a career out of wasting everybody’s time.

Those who wished they got crypto rich and decided to make a career out of wasting everybody’s time.

I have no problem with people in the first group. There are some genuinely knowledgable, intelligent content creators doing good work. But they are vastly outnumbered by those who make a living wasting everybody’s time.

Crypto influencers are out to make money any way they can. Some will try and shill you a token in which they’ve invested or else encourage you to sign up to leverage-trading platforms with their referral links. Some try and persuade their followers to buy into the latest ICO. The really crafty ones make snazzy videos and rank ICOs and potential investments, all with disclaimers of not being financial advisors. But what they’re really trying to do is get you to buy something. The most influential influencers will have access to presales and private sales, so they’re always a step ahead of their audiences.

Through the bear market, crypto influencers have had to branch out and find other ways to profit, stroke their egos and amuse themselves. Some have formed startups that usually seem to be based around providing marketing services. Whatever they’re doing, they’ll be trying to sell something.

You can buy spots on any one of 10,000 crypto podcasts, or pay for tweets or coverage on Youtube. Got a spare 38,000 USD? Well then you can get on one of the major Youtube channels. Only got a couple of grand? Take the preferred choice of soon-to-fail crypto projects by paying one of the lower tier influencers for a review that ends up being 20 minutes of the influencer just reading the content from your website. The craftiest influencers organise events and try and get sponsorship from bigger companies so they can keep getting their holidays paid for. They prey on unsuspecting crypto startups, ready to flash rate cards for sponsored tweets, shoutouts and “exposure”.

They’ll remind you constantly on Twitter that they are focussing on their passions, which these days usually means looking bored on stage at conferences, launching lifestyle brands or making travel vlogs. They’re always on the verge of greatness and doing their part by launching the latest newsletter, education portal, podcast, investment firm, news site or research outlet.

Yet despite the best efforts of influencers, crypto mass adoption isn’t going to come from another tutorial teaching people how to manage their own private keys. Mass adoption comes when we have products and services that people can use and that make their lives easier without even knowing about crypto or blockchain.

We’re nowhere near that stage and the barriers to entry are way too high. But sure, let’s have another YouTube channel or podcast to teach people about the basics of crypto so an influencer can feel like they’re contributing to something.

Most crypto content creators are just filling the airwaves with noise in the hope of getting paid for it.

Immature Space, Immature People

Crypto is full of adults behaving like spoiled children. So-called leaders within this space simply don’t know how to interact with each other without being complete dicks.

From CEOs and founders to evangelists and developers, crypto is an unruly mess because people spend so much time arguing, bickering and calling each other names over the most trivial nonsense. Every little disagreement gets aired for all to see.

Crypto conference organisers go out of their way to put on stage the most obnoxious lineup of speakers possible. If there’s a blockchain week somewhere in the world you can be sure that Craig Wright, Roger Ver, Tone Vays, Nouriel Roubini (who hates crypto), Brock Pierce, Samson Mow and other familiar faces will be rolled out to argue with each other in public.

The Sorry State of Crypto Media

Crypto is one of the most poorly covered sectors I’ve ever seen. The standard of crypto journalism is so terrible that I wouldn’t even call it journalism. General media’s reporting on Bitcoin and cryptocurrency is usually bad and focussed on extreme negatives or else wild stories about people getting rich. But you can perhaps forgive regular journalists for not having much of a clue as crypto isn’t a topic of widespread interest.

The real rot, however, lies within. At the bottom of the pile there are the multitude of crypto sites, which are little more than blogs, full of poorly written articles, which if not auto-generated may as well be.

Then there are the real crypto news sites like CoinDesk and Cointelegraph, where at least some real journalism goes on, but the quality overall is still relatively poor. Crypto outlets like The Block, Decrypt and Breakermag (RIP) add real value, but even these reputable sites have staffers who have posted inaccuracies, deleted tweets and bickered like kids with others.

Crypto journalism is shoddy. Corrections and edits are frequent. Allegations can run wild. There’s healthy debate, sure, but the standards to which we should hold journalists often don’t apply in crypto. Reporters can pretty much write or cover anything they want and nobody bats an eyelid about conflict of interest.

Ran Neuner’s CNBC show is one of the most popular and widely watched shows about crypto. Neuner is able to host it despite being an advisor to, and investor in, multiple crypto startups and projects. He has a considerable financial interest in cryptocurrency in general, even in crypto exchanges. But that doesn’t stop him giving a platform to projects in which he’s invested.

While crypto journalism may be below par, it’s not helped by pressure from rich and powerful figureheads in the space. Billionaire Binance founder CZ and TRON founder Justin Sun both supported an Internet troll who spent considerable time harassing journalists and analysts from The Block by inciting Twitter mobs after an unfavourable story about Binance was published.

The story in question needed a correction to clarify that a police raid didn’t take place, but that wasn’t enough for the army of trolls who frequently bully and attack anyone with whom they disagree.

Crypto Conferences and Events for Days

Not a week goes by without some kind of crypto forum, meetup or event. We are bombarded with endless gatherings that serve little more purpose than to perpetuate the echo chamber. The crypto rich spend their time travelling around the world to meet up with each other in different cities and take selfies.

How much crypto conference content (most of it contributed by influencers) do we need to sit through before people realise they’re wasting their time? From poorly recorded interviews with shitcoin founders to countless vlogs showing someone walking through the doors of the latest conference, we are scraping the barrel here even before we’ve got to the villa pics.

New people aren’t attending these conferences. Sure, there’s networking going on, but let’s be under no illusion: it’s a vacation. There’s nothing inherently wrong with that, but it shouldn’t masquerade as driving financial inclusion. People make careers off this nonsense, just organising and/or attending events.

The Problem with Justin Sun

Is it fair to single out one person as being the root of all that is wrong with the crypto space? Probably not. I don’t think he’s a bad person, but I do feel there’s validity in pointing to Justin Sun as representing much of the worst that this space has come to stand for. It all started in 2017 with an incomprehensible white paper that was partly plagiarised from other whitepapers. From then on, TRON became wildly popular because of it’s low token price and propensity to volatility, with a massive pump from 20 sats up to 2,000 sats that made a lot of people very rich.

Justin Sun made a name for himself by announcing new partnerships every other day, almost all of which turned out to be bullshit. Most of the time, he’d just hype up a partnership with some other startup operated by his friends, like Gifto, Game.com, OCN and various others. Sometimes Justin would partner with bizarre companies like toilet manufacturers or space companies (“China’s SpaceX”, he said).

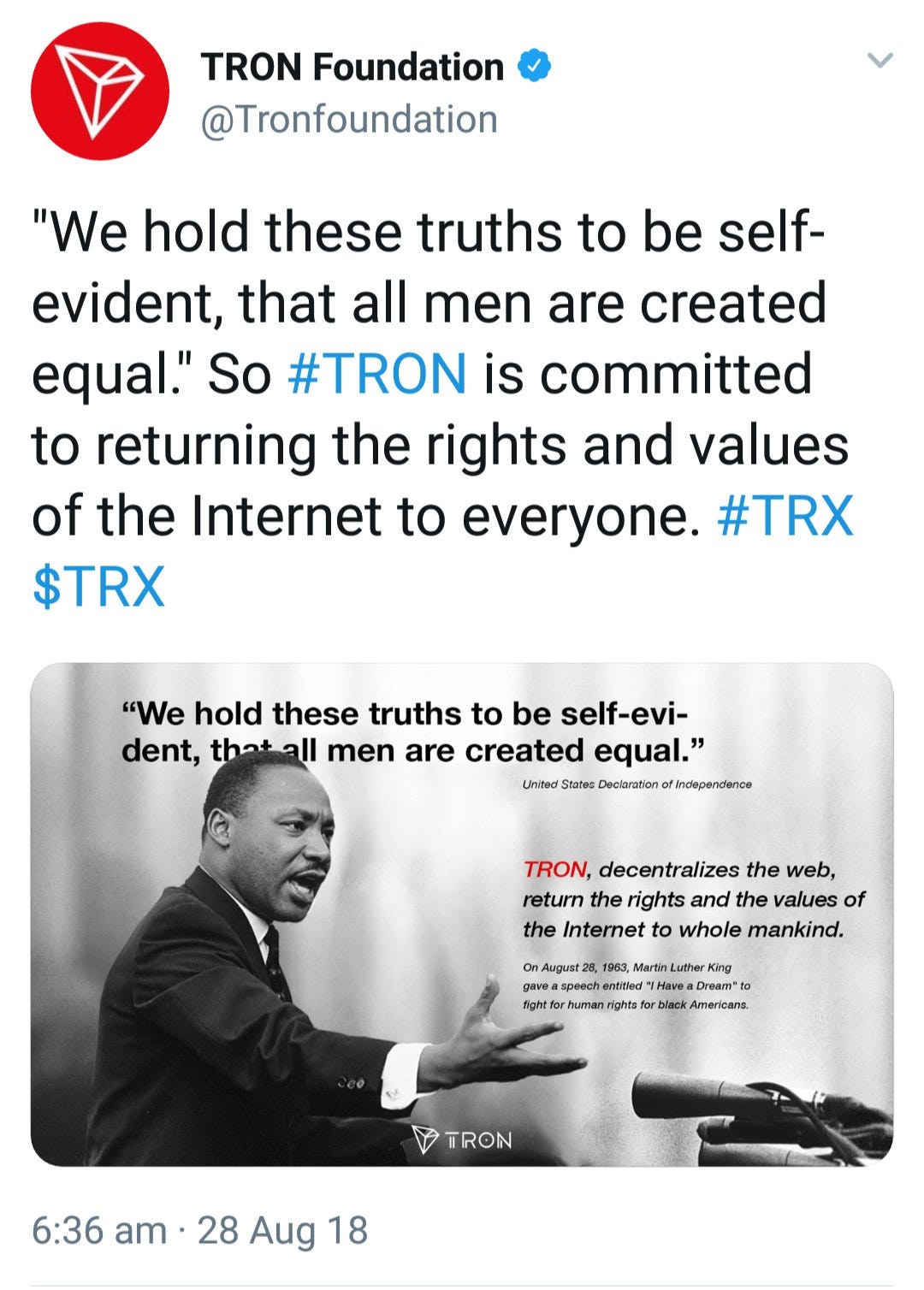

There is no event or circumstance that Justin Sun won’t use to try and draw attention to himself and TRON. From randomly pledging 1 million USD to Greta Thunberg (did he ever follow through with that?) to comparing TRON’s mission to the Civil Rights Movement, if there’s a cause to be hijacked, Justin will be right in there.

Justin has been able to get away with the kind of nonsense that doesn’t fly in any other sector. Worse than that, he is enabled by shills, journalists, bloggers, crypto exchange CEOs and others within the space.

Justin Sun has made everything about himself, splashing his face on every poster, billboard, advertisement and marketing material he can. The smallest unit of TRON currency is called a “Sun”; the network TRON runs on is called Sun network.

He’s made so much money and has access to such vast resources that he believes he can act without consequence. If he puts a foot wrong, he knows he will be defended by his ravenous community and uber shills, who seem unfazed by the fact that TRON isn’t even decentralised, with most of the network controlled by Justin (at least 6 of 27 Super Representatives) or his friend CZ and Binance (54.30% of the voting power).

Justin Sun represents the worst of what crypto has become.

I learned my lessons in crypto, some the hard way. I have no regrets, but I’m glad I got out. I just hope that the space matures and can one day really make the world a better place. There are some great minds in crypto and they are tackling some of the big issues of our time — privacy, access to financial services, financial inclusion and more — but they’re being weighed down by hangers-on.

My experience and thoughts are just that — mine. I’m sure many will disagree with me. But the truth is, I just had a lot I wanted to get off my chest, and that’s before even getting into my experiences at Liquid. That in itself could probably provide about a book’s worth of material. Some day, maybe.

As sad as it sounds, there are few professions now where you will not work hard and earn a decent wage, so that you can afford to do anything. But when you're in investments, that's the kind of life you can come to after a couple of years. So I advise you to think about your life and make the right decision. I trade through a broker and I use cryptocurrency portfolio tracker to keep track of my well-assembled portfolio, how it grows day by day.

Before you start, as with any investment, it is important to understand exactly which global asset you are investing in. This is especially true for a speculative - and constantly evolving - asset like cryptocurrency. It is much easier to do this if you are familiar with the words that are often used in this world.

Demand creates supply and more and more cryptocurrency holders are forced to exchange digital assets for real money as bitcoins and altcoins are difficult to use for settlement transactions. Today, cryptocurrency can be easily withdrawn to any electronic wallet or bank account, as well as cash. The main thing is not to rush to choose the method of cashing out, I advise you to read the article https://godex.io/blog/crypto-currencies/complete-guide-how-to-cash-out-bitcoin, as haste and inattention can quickly lead to a fraudulent service, for example, to phishing pseudo-exchange.

The major reason behind its failure is that people are still not trusting bitcoins and they still think that its some type of fraud and the only solution to avoid such type of fraud is to always go for some reliable exchange like crypto exchange software to avoid such types of frauds.

The girl left me because I didn't have a profession and a car, but now I have everything I wanted. I invest in bitcoin, ethereum, solana and other promising coins, and I also check the coins that go through the ICO. There is a list of rated exchangers at https://cryptototem.com/top-crypto-exchanges/ I think this can be interesting for you.

As horrible as it may sound, there are few jobs nowadays where you will not work hard and make a fair pay, allowing you to do anything you want. When it comes to investing, though, that's the type of life you may have after a few years. So, I encourage you to reflect on your life and make the best option possible. To keep track of my well-assembled portfolio and how it increases day by day, I created a PHP Web Development Company Los Angeles tracker.

The biggest reason behind its failure is its online existence but one thing I can make sure and that is essay writing services from Top Essay Writing which will never be failed and give you best services.

It was extremely helpful! I've scarcely started, yet I'm realizing even more at this point! Esteem my appreciation and keep up the mind boggling work. Belgian Waffle Near Me

It's unfortunate but true that many cryptocurrency projects ultimately fail, as highlighted in this insightful piece. The current volatility in the crypto market reflects the challenges faced by these projects, from cash grabs to mismanagement of funds. I recognize the importance of shedding light on such issues to foster a more transparent and sustainable crypto ecosystem. For those navigating the crypto space, consulting reputable companies like Consulting24 for regulatory guidance and licensing support is crucial.

No have idea regarding this issue but one thing I can recommend you and that is our best mobile app development company UK as they are offering the best and most professional services.

I completely agree! Fantastic blog—truly an enjoyable read. By the way, if you’re seeking high-quality solutions, I’d suggest checking out our offshore mobile app development services. Their services are top-tier and highly professional.

As a Partner and Co-Founder of Predictiv and PredictivAsia, Jon specializes in management performance and organizational effectiveness for both domestic and international clients. He is an editor and author whose works include Invisible Advantage: How Intangilbles are Driving Business Performance. Learn more...

14 comments:

As sad as it sounds, there are few professions now where you will not work hard and earn a decent wage, so that you can afford to do anything. But when you're in investments, that's the kind of life you can come to after a couple of years. So I advise you to think about your life and make the right decision. I trade through a broker and I use cryptocurrency portfolio tracker to keep track of my well-assembled portfolio, how it grows day by day.

I think crypto exchanges will be the best option. But you need to pay attention to how long these exchanges work and study user reviews.

Before you start, as with any investment, it is important to understand exactly which global asset you are investing in. This is especially true for a speculative - and constantly evolving - asset like cryptocurrency. It is much easier to do this if you are familiar with the words that are often used in this world.

Demand creates supply and more and more cryptocurrency holders are forced to exchange digital assets for real money as bitcoins and altcoins are difficult to use for settlement transactions. Today, cryptocurrency can be easily withdrawn to any electronic wallet or bank account, as well as cash. The main thing is not to rush to choose the method of cashing out, I advise you to read the article https://godex.io/blog/crypto-currencies/complete-guide-how-to-cash-out-bitcoin, as haste and inattention can quickly lead to a fraudulent service, for example, to phishing pseudo-exchange.

The major reason behind its failure is that people are still not trusting bitcoins and they still think that its some type of fraud and the only solution to avoid such type of fraud is to always go for some reliable exchange like crypto exchange software to avoid such types of frauds.

The girl left me because I didn't have a profession and a car, but now I have everything I wanted. I invest in bitcoin, ethereum, solana and other promising coins, and I also check the coins that go through the ICO. There is a list of rated exchangers at https://cryptototem.com/top-crypto-exchanges/ I think this can be interesting for you.

As horrible as it may sound, there are few jobs nowadays where you will not work hard and make a fair pay, allowing you to do anything you want. When it comes to investing, though, that's the type of life you may have after a few years. So, I encourage you to reflect on your life and make the best option possible. To keep track of my well-assembled portfolio and how it increases day by day, I created a PHP Web Development Company Los Angeles tracker.

The biggest reason behind its failure is its online existence but one thing I can make sure and that is essay writing services from Top Essay Writing which will never be failed and give you best services.

It was extremely helpful! I've scarcely started, yet I'm realizing even more at this point! Esteem my appreciation and keep up the mind boggling work. Belgian Waffle Near Me

Such an interesting post.

It's unfortunate but true that many cryptocurrency projects ultimately fail, as highlighted in this insightful piece. The current volatility in the crypto market reflects the challenges faced by these projects, from cash grabs to mismanagement of funds. I recognize the importance of shedding light on such issues to foster a more transparent and sustainable crypto ecosystem. For those navigating the crypto space, consulting reputable companies like Consulting24 for regulatory guidance and licensing support is crucial.

No have idea regarding this issue but one thing I can recommend you and that is our best mobile app development company UK as they are offering the best and most professional services.

I completely agree! Fantastic blog—truly an enjoyable read. By the way, if you’re seeking high-quality solutions, I’d suggest checking out our offshore mobile app development services. Their services are top-tier and highly professional.

Post a Comment