The Reason Giving Covid Stimulus Checks Directly To Americans Worked

People spent the money they received, which helped keep others employed and stimulated the otherwise moribund economy as intended. JL

Jordan Weissmann reports in Slate:

The CARES Act sent adults cash payments of up to $1,200, plus an extra $500 for

each of their kids, and tacked $600 a week onto unemployment benefits so

the jobless could keep paying their bills. Congress’ plan has succeeded. Washington handed out a lot of money and

as a result, by May even the hardest-hit

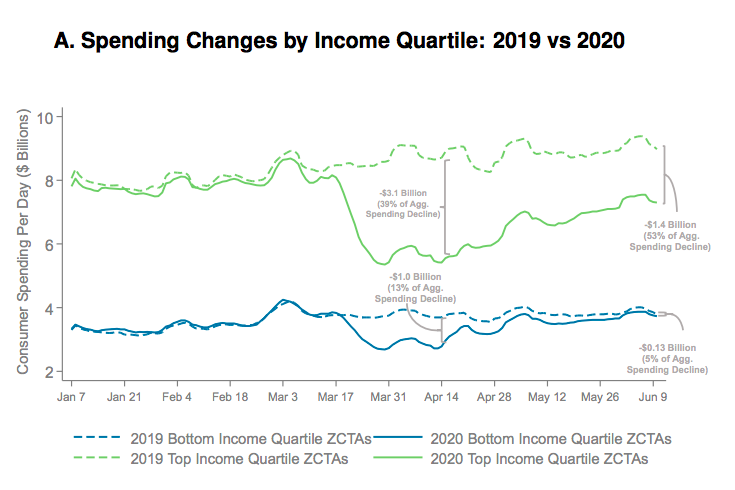

households were able to go back to spending like normal. By June, households living in the poorest quarter of zip codes had only

reduced their credit and debit card spending by 4%.

When Congress passed the CARES Act in March, it had a straightforward strategy to help families make it through the economic nightmare of the coronavirus crisis: Give them money. It sent adults cash payments of up to $1,200, plus an extra $500 for each of their kids, and tacked $600 a week onto unemployment benefits so the jobless could keep paying their bills. (Higher-income households got less, and in some cases, nada.)

Some criticized the plan for being too stingy; among left-wing activists and politicians, the phrase “$1,200 is not enough”became an angry Twitter mantra. Others—myself included—worried about the execution, and whether cash would make it to those who needed it most. State unemployment systems were overwhelmed by the record flood of applications, leaving laid-off workers to wait weeks or even months for their benefits. The IRS stumbled as it tried to get stimulus payments to Americans who didn’t have a direct deposit account on file, whotend to be poorer; some people actually threw out the prepaid debit cards the agency sent out, because theylooked like junk mail.

But as more economic data has started to roll in, giving us a fuller picture of Americans’ finances over the past few months, it’s begun to look more and more like Congress’ plan has succeeded. Washington handed out a lot of money and as a result, a new paper suggests, by May even the hardest-hit households were able to go back to spending like normal.

The first clear evidence that Congress’ giant cash bomb had worked as intended arrived late last month, whenthe government reportedthat despite massive job losses, personal incomes had actually risen to an all-time high in April. This was mainly due to the $1,200 economic impact payments, though the CARES Act’s generous unemployment benefits contributed as well.

But while this was all welcome news, it still wasn’t clear that poorer Americans were getting as much help as they needed. After all, job losses during the crisis appeared to beconcentrated amonglow-wage employees in service industries like restaurants and hotels that had been forced to shut down. It was entirely possible that, even if the CARES Act had raised incomes overall, many of those workers and their families were still in trouble.

But the latest evidence suggests that Washington really has done a pretty good job supporting poorer households through the pandemic. On Thursday, the researchers at Harvard’s Opportunity Insights project released awide-rangingpaper that analyzed the successes and failures of the government’s economic response to the pandemic, using real-time private sector data from personal finance apps and companies that track credit card transactions, among other sources of information. It concludes that after falling sharply in April, spending by low-income families rebounded in May, after relief checks started going out. By June, households living in the poorest quarter of zip codes had only reduced their credit and debit card spending by 4 percent, compared to the same point in time in 2019.1Those in the richest quarter, who cut back on little luxuries like travel and dining out due to the plague, dropped their spending by 17 percent.

Opportunity Insights

So Americans’ incomes rose overall by the end of April, and low-income families were able to start spending more or less like normal by May, even amid unemployment rates unseen since the Great Depression. Put two and two together and you have pretty strong evidence that, in aggregate, Congress may have actually kept poorer Americans financially secure throughout the economic crisis.

None of this is to say that every single person in America is doing just fine at the moment. There are still droves of out-of-work people waiting for their unemployment benefits, especially in Florida, where the system has beensuch a disasterthat it has sparked protests and become a political headache for the state’s Republican leaders. And it’s possible that many Americans are only managing to cover their essentials like groceries and electric bills because they’veheld offon paying their debts; asNPR reportedearlier this month, 9 percent of mortgages are in forbearance, and 15 million credit card and 3 million auto loan accounts are on some sort of delayed or partial payment plan. If we see a tsunami of mortgage defaults or evictions in the coming months, we’ll know Washington’s rescue plan didn’t go far enough.

It’s also conceivable that the Opportunity Insights study is understating how much low-income families have cut back. Again, the new data is based on debit and credit card transactions. But poorer Americans tend torely heavilyon cash, and if they’re using much less of it, their overall spending may have fallen more than we can see at the moment.

On top of all this, out-of-work Americans could find themselves in a world of trouble if Congress fails to renew the expanded unemployment benefits it created, which are now scheduled to expire in July.

Still, we have some hopeful signs that Congress might have gotten at least one critical part of its response to the coronavirus crisis right (especially in comparison to itspoorly orchestratedattempts at aiding small businesses). At a moment when almost all of our institutionsseem to be failingin disastrous ways, lawmakers may have successfully thrown out enough life preservers to keep Americans from drowning financially. For now, anyway,it turns out that $1,200 (and $500 per child and $600 a week in unemployment benefits) might have been enough.

As a Partner and Co-Founder of Predictiv and PredictivAsia, Jon specializes in management performance and organizational effectiveness for both domestic and international clients. He is an editor and author whose works include Invisible Advantage: How Intangilbles are Driving Business Performance. Learn more...

0 comments:

Post a Comment