The lesson is that markets always revert to the mean and the illusory lure of grabbing short term gains all too often remains just that - illusory. JL

Berber Jin reports in the Wall Street Journal:

During the recent bull market, venture-capital investors that typically exit a stock after taking it public held on to shares in the hope of maximizing returns. Seeing the sharp rise of stocks like Zoom Technologies Inc. after their public listings, they decided to hold on to shares in the hopes of capturing those gains in the supercharged public market. Instead, the sharp selloff in technology stocks in 2022 has dealt a punishing blow to that strategy. Some of the splashiest startup stocks from 2021 plunged, making it unlikely those investors will recover the value of their earlier positions anytime soon, if at all. These losses further mar a dismal year for VCs (due to) a slowdown in startups and public listings.Venture-capital firms that deployed a new strategy of holding stocks for longer have come to regret it amid last year’s market rout.

During the recent bull market, venture-capital investors that typically exit a stock after taking it public held on to their shares in the hope of maximizing returns. Instead, the sharp selloff in technology stocks in 2022 has dealt a punishing blow to that strategy. Some of the splashiest startup stocks from 2021 plunged, making it unlikely those investors will recover the value of their earlier positions anytime soon, if at all.

Roblox Corp. investor Altos Ventures Management Inc. held a $7.5 billion stake in the videogame company when it went public in March 2021. While it returned some shares, the value it retained swelled to more than $11 billion at the stock’s peak in November 2021, according to public filings. Then, the market soured, sending Roblox’s shares tumbling, and Altos’s gains with it.

The venture firm still held more than 60% of its IPO stake as of Sept. 30, an unusually large percentage for a company that went public almost two years ago. It has lost more than $5 billion on those paper gains in the first nine months of 2022, the filings show.

“The rise in the public market was intoxicating for everybody,” said Matt Murphy, a partner at VC firm Menlo Ventures. When that changed, he added, “a number of firms got burned by that.”

Menlo Ventures still held around half of its shares in clothing reseller Poshmark Inc., which went public in January 2021, by the end of that year. By that time, Poshmark’s stock had fallen more than 80% from its peak. Mr. Murphy said most venture capitalists wished they had exited shares more quickly last year, but the firm felt good about its exit timing on Poshmark stock.

The strategy that has left VC investors questioning their new approach is only one of several investment plans to have backfired during a more than yearlong stock market retreat that lowered the portfolio values of a vast number of financial players and individual investors.

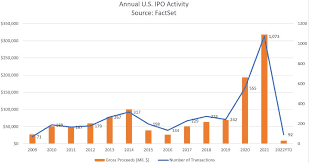

Startup investors typically exit companies once they have gone public to avoid market volatility. But during a decade-plus bull market that accelerated during the pandemic, these investors changed tactics, according to venture capitalists and fund investors. Seeing the sharp rise of stocks like Zoom Technologies Inc. after their public listings, they decided to hold on to shares in the hopes of capturing some of those gains in the supercharged public market.

Sequoia Capital, an early backer of Apple Inc. and Airbnb Inc., announced a new longer-term fund structure in the fall of 2021 that would allow it to hold shares in public companies indefinitely, arguing that it could accrue more profits through the new approach. In addition to holding on to stock, the firm has purchased new shares in public companies including software provider Datadog Inc., public filings show, part of a broader trend among Silicon Valley investors.

“For the great companies, there was so much more return potential,” said Sequoia partner Roelof Botha at The Wall Street Journal’s Tech Live conference in October. “The last time I checked, you don’t want to put an expiration date on your relationship with a great company.”

Some venture firms haven’t just seen paper gains shrink, they actually lost money outright by hanging on to shares—a rarity for such investors given how early they initially acquire stakes in startups.

Sequoia plowed a total of $258 million into three funding rounds for stock-trading app Robinhood Markets Inc. beginning in 2018, according to calculations by the Journal and people familiar with the matter. The firm’s stake was worth around $175 million as of Wednesday’s market close, the Journal calculations show, translating into an $83 million loss for the firm.

Had Sequoia unloaded those shares when lockup restrictions expired in December 2021, it could have made a profit of over $240 million on its investment. Robinhood’s shares fell 55% in 2022 as the business has struggled with a drop in active user count and falling revenue, denting its long-term prospects and triggering a wave of job losses.

Sequoia, among the most vocal venture-capital proponents of the new strategy of holding public stocks, also missed out on billions of dollars in potential gains for some of its largest stock positions, including software provider Snowflake Inc. Sequoia still owns the majority of its IPO shares in Snowflake, which went public more than two years ago, public filings show. Snowflake’s stock has lost roughly 65% from its post-IPO high.

A Sequoia spokesman declined to comment.

These losses further mar a dismal year for venture capitalists that are contending with a slowdown in startup deal-making and a drought in public listings.

VC firms in 2022 were on pace to return the lowest percentage in more than 15 years of the assets they manage to their backers, according to data compiled by Hamilton Lane as of Sept. 30.

The lower returns could decrease the fresh cash these investors need to back new funds and slow down the pace of fundraising for new funds, according to fund investors. Venture firms typically distribute stock back to their fund investors, known as limited partners, who are then able to sell them on the open market.

The decision on whether to hold on to a stock after its public listing or stick with the more traditional approach has at times helped define the difference between venture-capital winners and losers.

Khosla Ventures and Spark Capital both invested early in Affirm Holdings Inc., a financial technology lender that went public in January 2021. Spark, which had a smaller IPO stake, unloaded its entire holding in Affirm by the end of 2021, returning more than $1 billion worth of shares to limited partners, public filings show. By contrast, Khosla liquidated less than one-fifth of its stake for less than $500 million by the same time, the filings showed.

As of Sept. 30, Khosla still held more than half of its IPO stake, whose value plunged by more than $600 million in the first nine months of 2022.

“We have seen more down cycles than most venture capitalists,” said Shernaz Daver, a spokeswoman for Khosla. “Short-term dips are not worrisome if the fundamental business is strong.”

0 comments:

Post a Comment