Is Venture Capital's Funding Behavior Becoming Counter-Productive?

As generative AI begins to look like it might actually be that next big thing, is the search for mega-growth thwarting real innovation by creating unrealistic expectations fueled by endless money and breathless hype?

The question is more than academic as IPOs become an historical anecdote and startups wither in the face of daunting demands for impossible returns. JL

Kyle Harrison reports in Newcomer:

Venture capital, as an institution, has developed a number of “move fast and break things,” “grow at all costs,” and “blitzscaling”

playbooks. But like

an unreliable drug dealer, as soon as VCs got a generation of founders

hooked on massive amounts of capital, ever larger valuations, and

increasingly grand ambitions, they disappeared. There are few playbooks for how to make progress from

unsustainable to sustainable. Who cares if Uber is at $30B of revenue,

still trying to figure out “if our unit economics work”? The early

investors made lots of money. The next phase is someone else’s problem.

Sometimes you get a song stuck in your head.

You don’t even realize you’re humming it or singing it to yourself. Eventually, your brain wakes up. And you realize the song is coming from the lips of a sentient homicidal plant desperate for human blood, and ultimately world domination.

One of those days, right?

Little Shop of Horrorsis a cult-classic movie that, when you show it to someone who has never seen it before, you almost find yourself apologizing for howweirdit is. Every time I find myself ruminating on excess, greed, or attempts to use ends to justify means, I find myself thinking about Little Shop of Horrors.

Audrey II, the aforementioned sentient murder plant, has a driving refrain throughout the film: “Feed me!” But beyond normal hunger (or homicidal foliage hunger) you also have institutional hunger. Humans are great at making hungry, hungry machines—fromhipposto industrial complexes that spanprisons,gas, andmilitaries.

Venture capital is no exception. Every engine needs fuel. Every process has inputs and outputs. But eventually, when incentives align, you start to see a hunger that is dangerously self-reinforcing.

Capital owners will rationally seek to multiply their wealth. But too often they hunger for risk. Capital allocators should pursue great investments. But too often they hunger for a way to deploy capital quickly. Startups want fuel to grow their businesses. But too often they hunger for cash as a status symbol or for their own quick enrichment.

Together these perverse appetites form their own sort of sentient murder plant. Maybe we can call it Audrey VC.

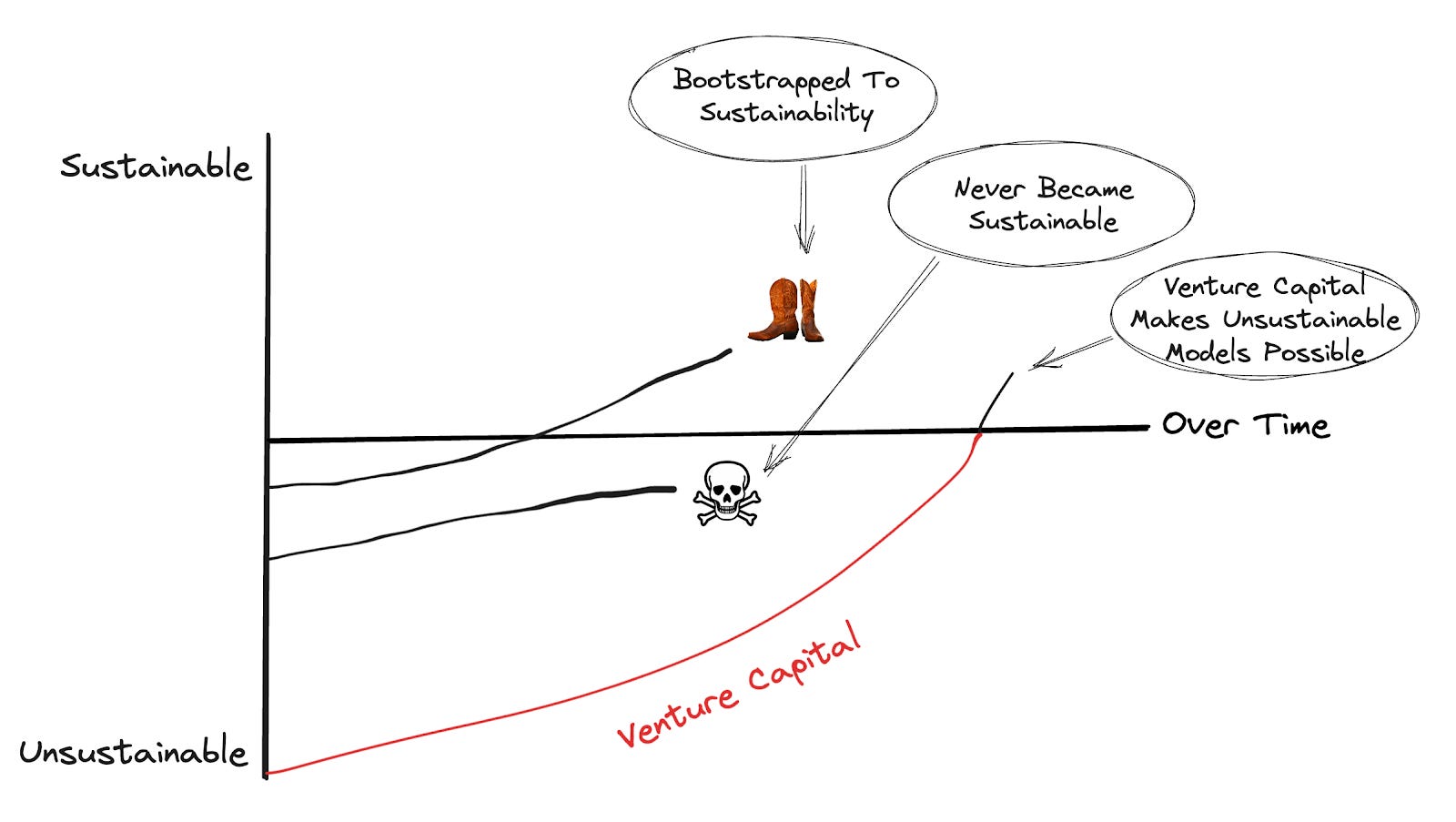

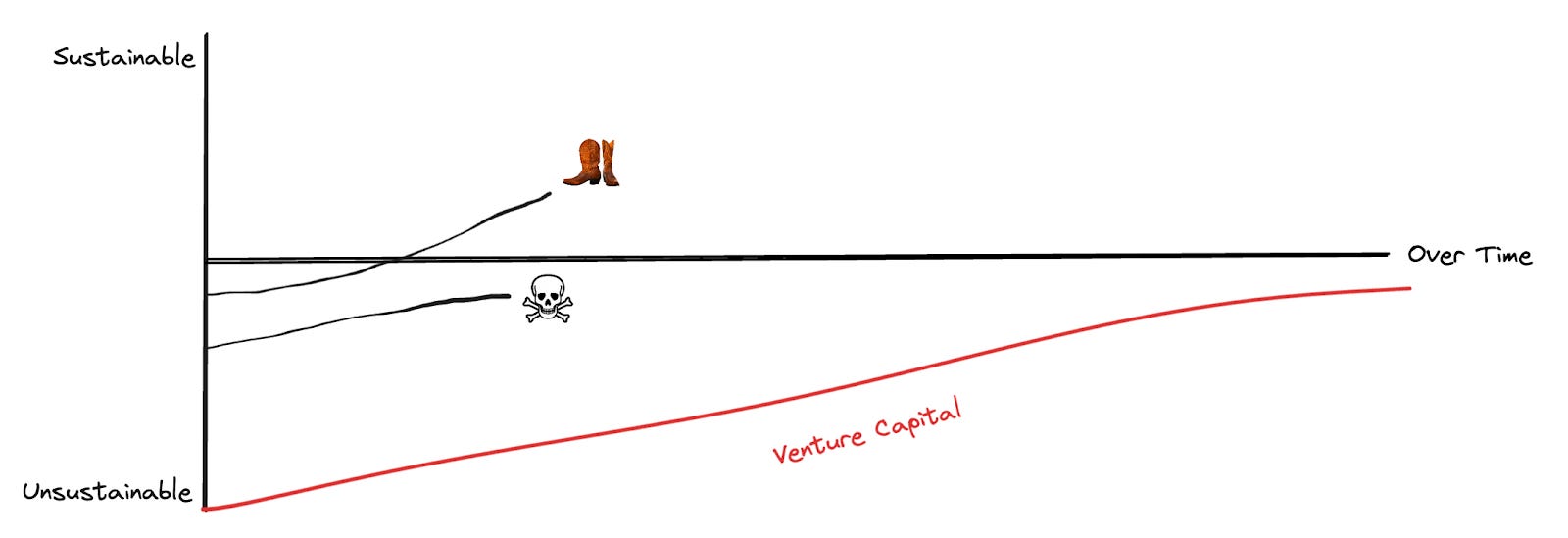

Venture capital enables the perpetuation of unsustainable models in favor of eventual scale. This isn’t necessarily a bad thing. The runway to experiment has been critical for any number of businesses.

Apple, Google, Facebook, Amazon, Salesforce, and so many others are companies that operated unsustainably for a while with the help of funding, in order to reach scale and become cash generating machines, with billions in annual cash flows today.

But any good thing taken to excess can become problematic. The same is true with capital. There are a number of businesses that have yet to demonstrate their ability to consistently turn a profit. That doesn’t mean they are bad businesses, but they’ve certainly been beneficiaries of exorbitant amounts of capital that may hide the less-than-economical aspects of their businesses.

There will always be the “move fast and break things” people who want to raise $100M every 6 months lighting money on fire as they go. And there will always be the bootstrapped worriers who look at VCs as parasites who ruin businesses. Neither of them will always be right or wrong.Cash, like any strategic asset, is a double-edged sword. It can be used effectively (even in large quantities) or it can impale you.

Uber, But For Taxis

In that same post on cash burn, I talked a lot about Uber and Lyft. When you look at Uber ($78B market cap, $31B in 2022 revenue) vs. Lyft ($3B market cap, $4B in 2022 revenue) you see a clear argument for burning hard to dominate a market. But Uber isn’t necessarily out of the woods yet.

Over the course of just the last six years since Uber went public, it has lost$30B+in market cap. In one companymemolast year, Uber's CEO,Dara Khosrowshahi, made what feels like a stunning call-to-action for a 10+ year old business: “This next period will be different, and it will require a different approach…We have to make sure our unit economics work before we go big.”

Before we go big?One newslettermade this point about Uber as the textbook example of a business that has always claimed it will reach profitability at scale:

But what is scale if not a company that operates in 72 countries and more than 10,500 cities, which last year had 118 million active users every month and completed 6.3 billion rides/trips/deliveries?Uber is the definition of scale, yet it is still nowhere near consistent and reliable profitability.

Uber faces increased pressure to turn a profit as a public company, economic conditions that could entice riders to spend less money, and a labor shortage for drivers. As a result, we've seen the price of Uber in some large cities increase by as much as40%over the last year.

A lot of people are talking about Uber as a great ZIRP that made transportation easier for everyone, but as the VC subsidy runs dry and the broader markets get more hostile, what happens to Uber's not-as-of-yet sustainable model?

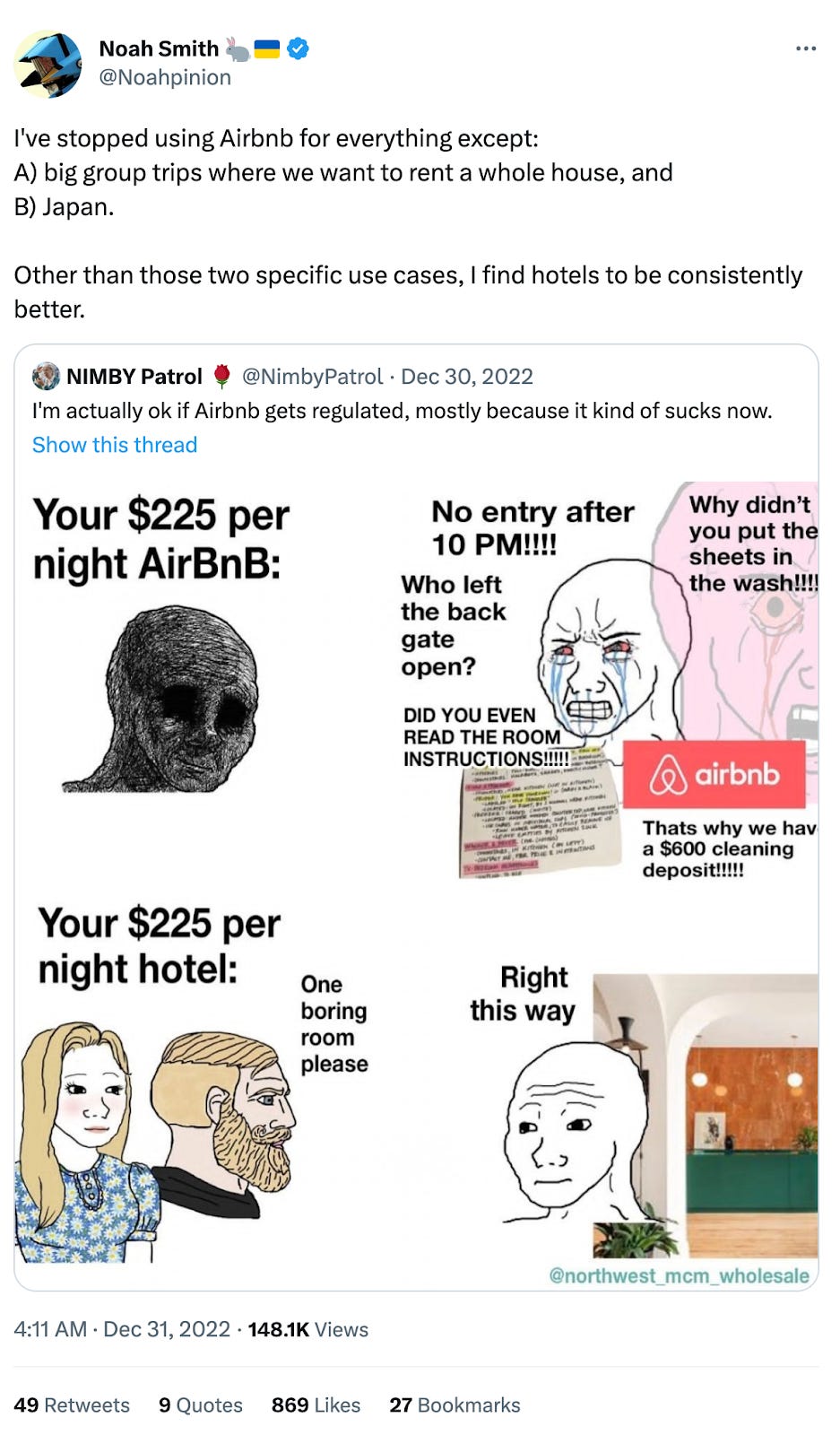

Airbnb: The Fee Machine

Where Uber was meant to disrupt the taxi business, Airbnb took similar aim at hotels. And where Uber has started to mask some of its price increases in surge pricing, Airbnb has been pushing the price grift in its fees. And theinternet noticed.

What was previously a pretty subsidized offering (by VCs and the company's willingness to live in alegal grey areawhen it comes to hospitality taxes), has become a wild west of hosts hungry for cleaning fees, armed with the best spy cameras in the world. 😳

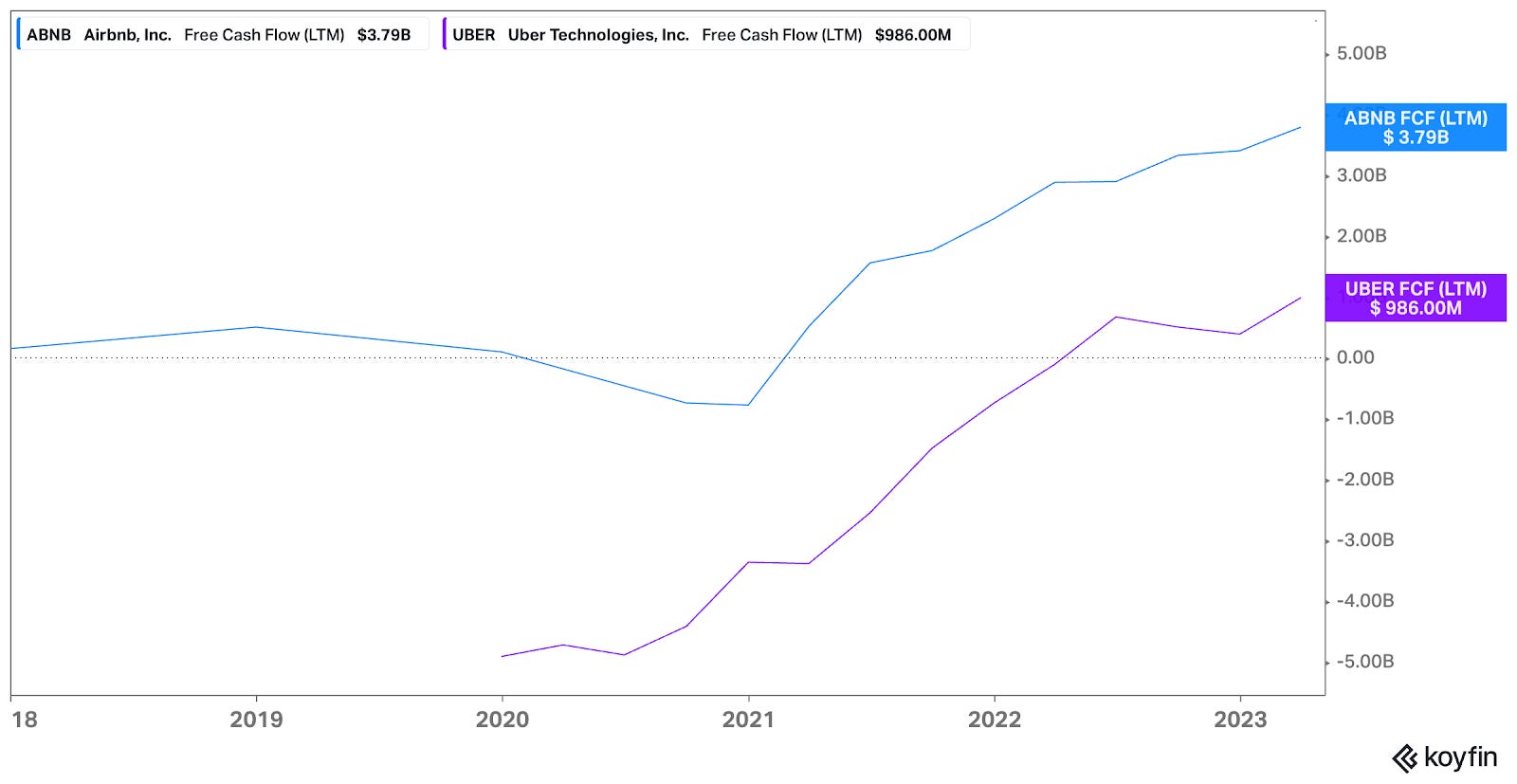

Granted, Airbnb has done a fair bit better job than Uber taking that subsidized commodity, and turning it into more of a cash-generative business. The question then becomes how consistently, and sustainably can Airbnb keep it up and grow that business?

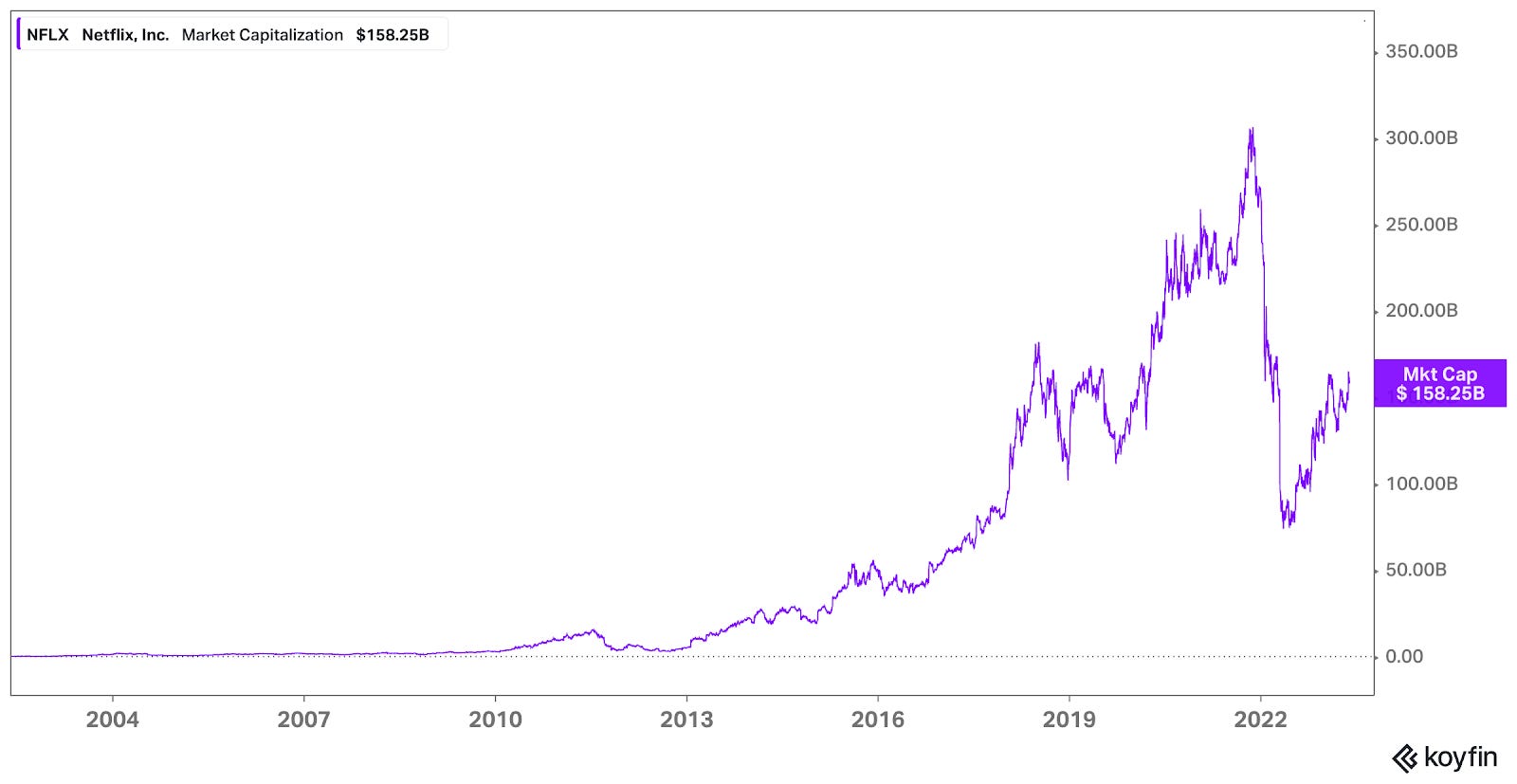

Netflix: What's Old Is New

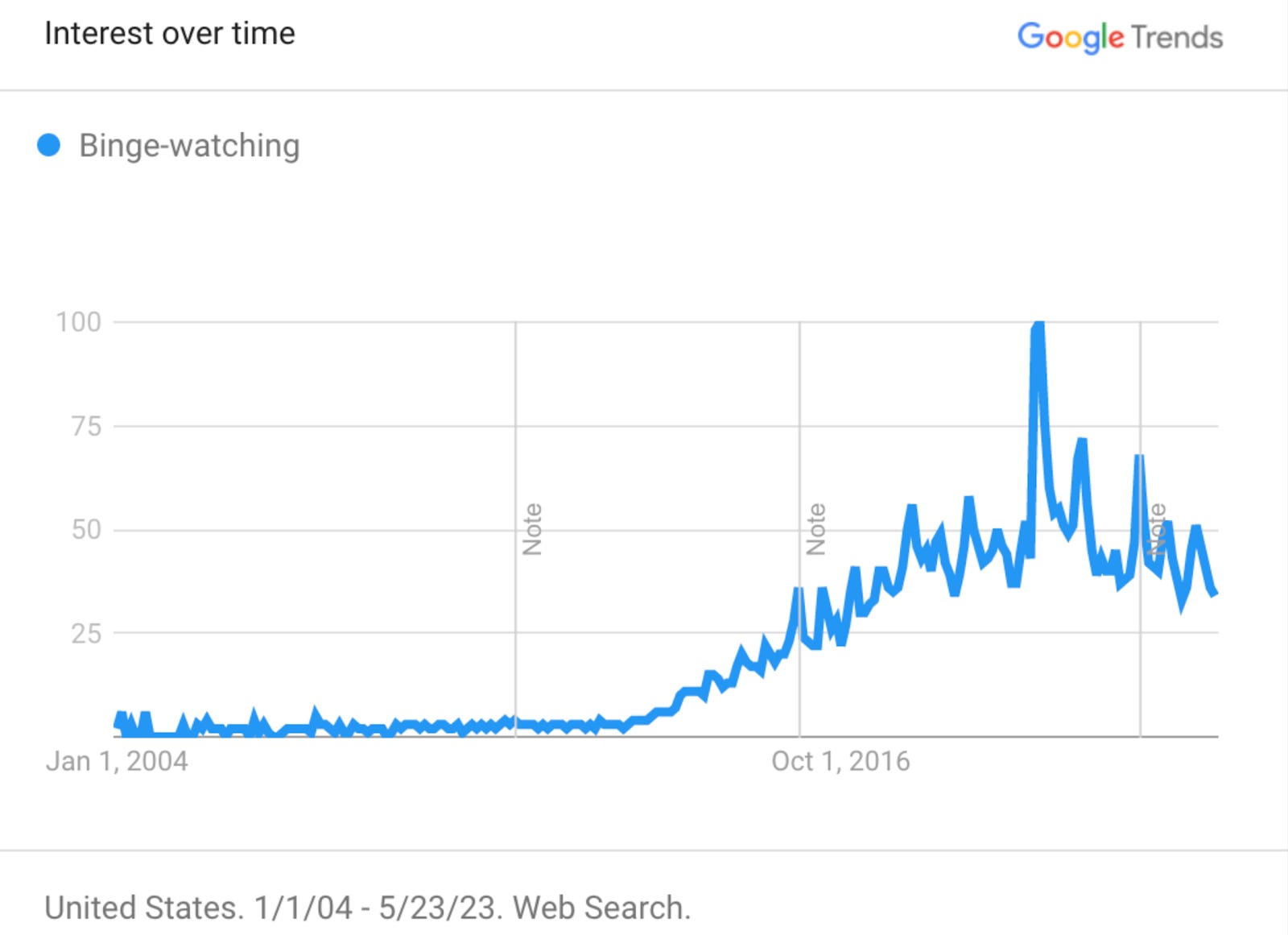

Finally, we have Netflix. Older than Uber or Airbnb (founded in 1997, compared to the other two in 2009 and 2008 respectively.) When the companystarted streamingin 2007, one of the main ideas was to provide subscription-based access to entire seasons all at once, effectively inventing the termbinge-watching.

From 2015 to 2019, Netflix was spending dramatically on their vision of building an entertainment empire, burning$9B+in cash. In 2021 alone, the company spent$17B+on content, racking up ~$27B of debt in the process.

In 2022, the bill came due to some extent. Netflix saw increased competition from rivals like Prime Video, HBO, Disney+, and a slew of up-and-comers like Apple TV, Peacock, and AL’s Toy Barn and Streaming Service (I assume). In April 2022, Netflixlostsubscribers for the first time in over a decade. The result was billions in market cap wiped out.

In a return to old-school business models, Netflix is now exploring anad-based versionof the product to drive revenue,releasingepisodes episodically rather than all at once to keep subscribers coming back, andcracking downon account sharing.

There's a famousquote, sometimesattributedtoJohn Maynard Keynes, about the market’s stubbornness in acting the way you want it to: “The market can remain irrational longer than you can remain solvent.”

I think the same idea exists for businesses whose models prove to be currently unsustainable. The market will act like a frustrated Mom waiting for her son to move out of the basement. She’s only going to put up with so much before she kicks him to the curb. In other words?What happens if the capital (or the market's patience for your unsustainability) runs out before you get sustainable?

The Unavoidable Weight Of Business Gravity

I’ve written beforeabout the force of gravity when it comes to company building. All of these companies–Uber, Airbnb, Netflix–are all results of a capital-rich environment. Netflix went public in 2002, but they were still able to access multitudes of capital as they grew and scaled as a public company.

It is a reality that the vast majority of funded companies start their lives as unsustainable engines. They burn cash in pursuit of a futureeconomic enginethat will spit off cash.But as capital became more, and more plentiful it has enabled unsustainability to persist for much longer.

When the inevitable weight of business gravity smashes into the face of an unsuspecting subsidy darling, it can get ugly.That is happening more and more as the subsidy subsides, the cash funnel shuts off, and companies have their lack of sustainability exposed. In thewordsofWarren Buffett, “only when the tide goes out do you learn who has been swimming naked.”

As the amount of venture capital exploded from$23Bin 2012 to$345Bin 2021, the appetite for funding unsustainable growth only increased. Thebusiness model of ventureis increasingly about aggregating as much AUM as possible. As a result, that sends VCs out looking for cash-hungry startups that want to consume ever more capital.

In the pursuit of unsustainable growth, there are two common strategies (among many others) that venture-backed startups have discovered as excellent cash infernos: (1) acquisition at all costs, and (2) selling to startups (aka turtles all the way down).

Acquisition At All Cost

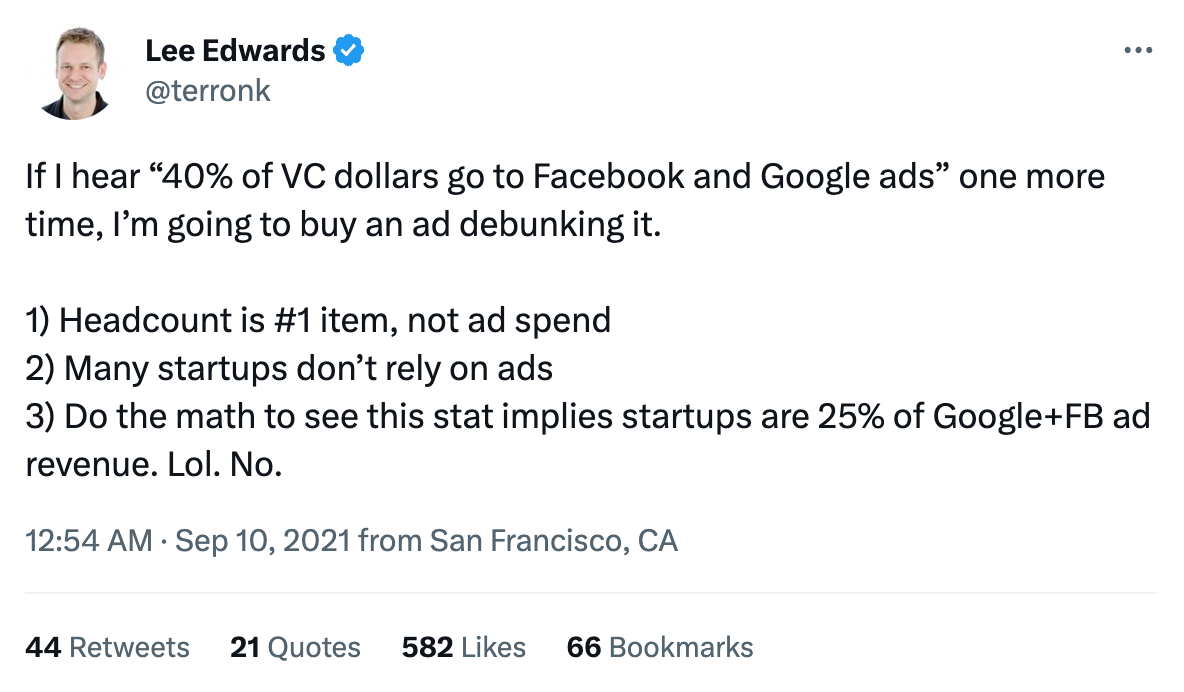

There is this oft-repeated idea that “40% of VC dollars go to Facebook and Google ads.” As best as I can tell, one common source for that data point is Chamath’s2018 annual letter, where he said:

Startups spend almost 40 cents of every VC dollar on Google, Facebook, and Amazon.We don’t necessarily know which channels they will choose or the particularities of how they will spend money on user acquisition, but we do know more or less what’s going to happen. Advertising spend in tech has become an arms race: fresh tactics go stale in months, and customer acquisition costs keep rising.

This idea that a near majority of venture dollars are going towards ads has become so memeified, that it’s often spat on by a lot of investors as a ridiculous notion.

Lee has somesolid math later in his threadthat if 40% of VC money were going to ads, then startups would account for 25% of Google and Facebook's revenue, which can’t be right. I agree with him. I don’t think startups are relying on extraordinary ad spend for pop up ads.

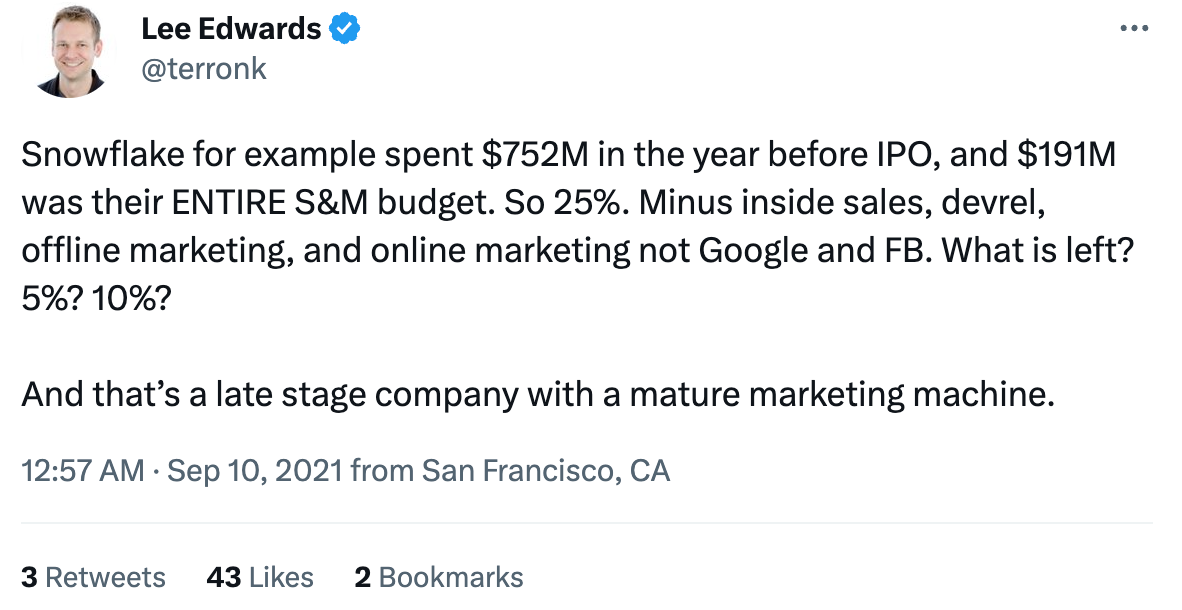

But the reality is that sales and marketing are some of the most significant portions of spend for the majority of companies. In Lee’s thread, he makes this argument about Snowflake’s S&M budget:

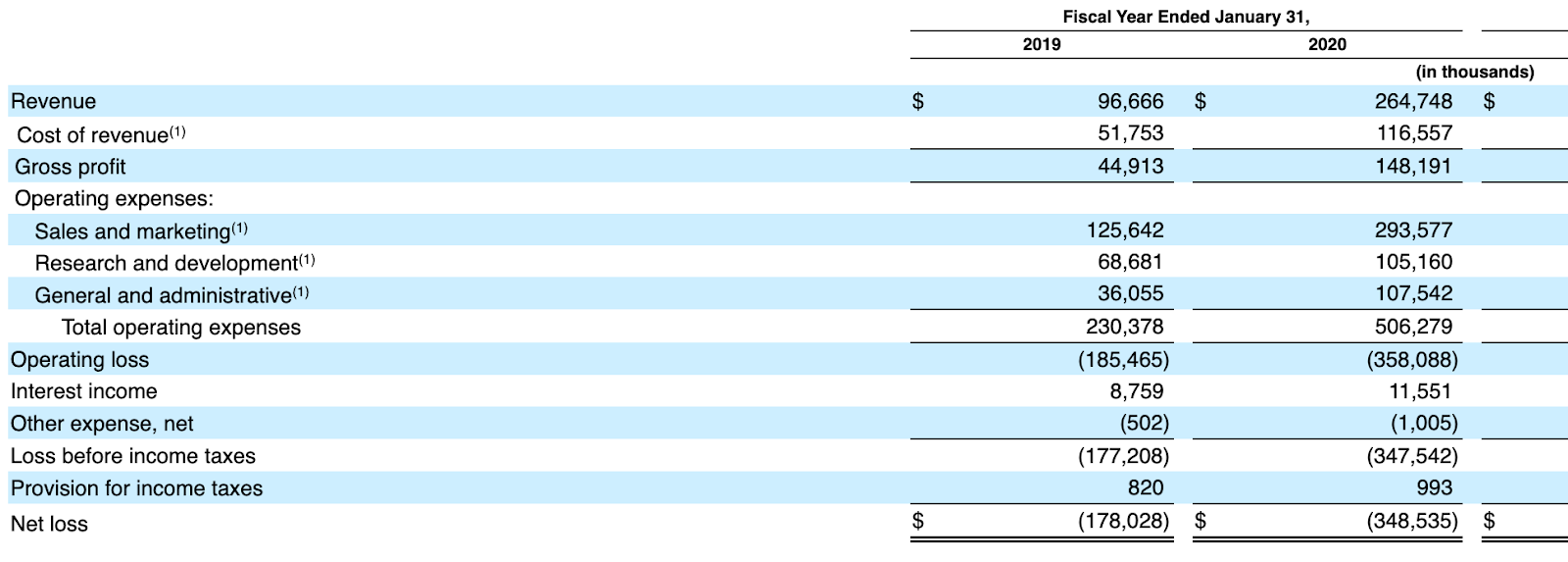

I tried to find these numbers but couldn’t find anything close to this. Snowflake went public in September 2020. Their last fiscal year before that ended January 31st, 2020. Inthe company's FY 2020, they spent $293M on S&M out of $506M of total OpEx (58% of their expenses).

Granted, one point that Lee makes is fair. Is ALL $293M just going towards Google and Facebook ads? Definitely not. There’s sales reps, DevRel, events, and on and on. I think the focus on “Google and Facebook ads” is a huge red herring that doesn't make sense.But 58% of their OpEx IS going towards sales and marketing, the company’s primary distribution and customer acquisition engine.

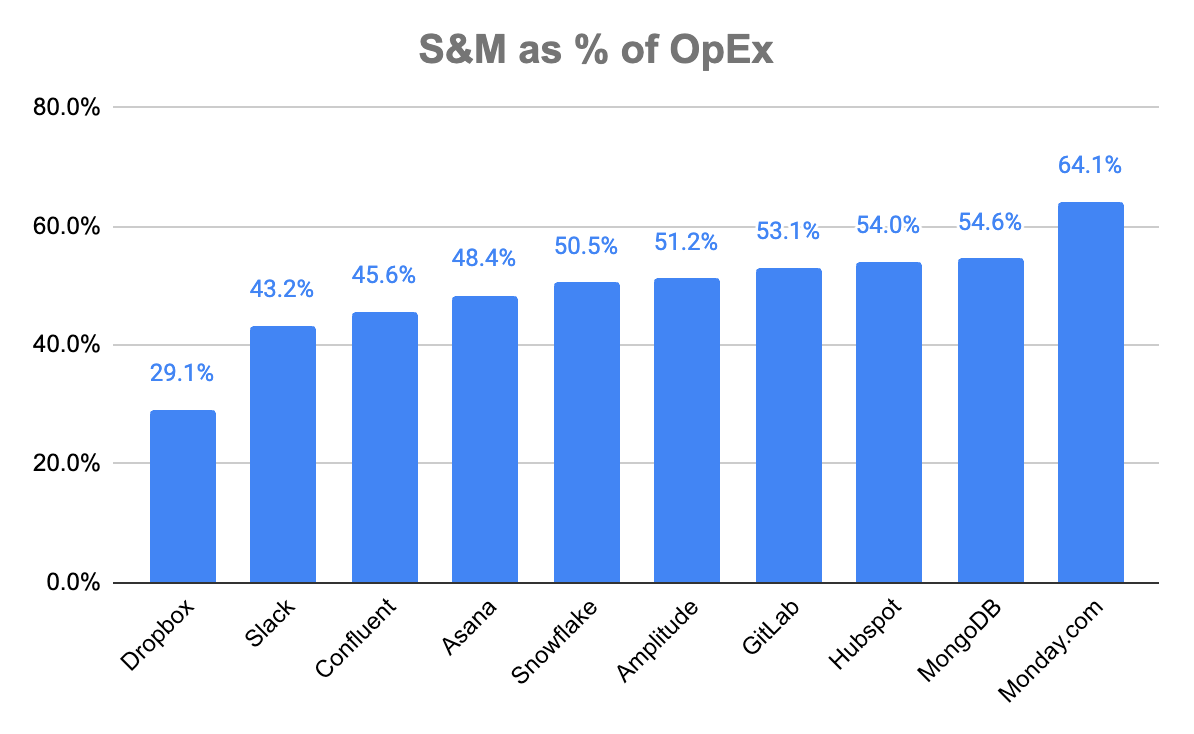

Since their IPO, I expected Snowflake’s S&M to come down, but it's only decreased as a % of OpeEx from 58% to ~50% most recently. In reality, the majority of companies are spending ~50% of their OpEx on S&M.

Source: Random smattering of 10Ks / 10Qs; Slack is April 2019; the rest are either quarterly or annually on 01/31/23 or 03/31/23

The world has become incredibly noisy. While 40% of all VC dollars going to Facebook or Google ads is nuts, the reality is that startups are being forced to borrow distribution from whatever platforms or resources they can get access to. That “borrowed distribution” creates a lot of dependencies that make it more difficult tocontrol your own destiny.

AWS might have made it easier than ever to start a technology company, but a flood of S&M-bound venture dollars have made it harder than ever to build a technology brand.Customer acquisition costs are rising across the board. So first, venture dollars flooded in and made the landscape noisier for startups. More companies in more categories doing more marketing. Then, startups turned around and realized “we all have venture funding!” and instead, started selling to each other.

Turtles All The Way Down

The phrase “turtles all the way down” is such aweird phrasethat I end up using more than I would expect. Just picture a turtle laying on a slightly larger turtle, laying on a slightly larger turtle into infinity. Got it? Good. Moving on.

A few people have pointed out this potential for “VC contagion” that exists in a GTM ecosystem of startups selling to each other.Newcomerfirst reportedthat Palantir was effectively buying revenue by pairing SPAC pipe investments with contracts for its services.Byrne Hobartcalledit “roundtripping.” The argument goes that Palantir was sending money out, so that it could come back in, and they could book it as revenue.

Unfortunately, the SPACs Palantir invested in have declined in value by~80%on average. So there’s a lot less revenue to come back to you from your investments if a number of those investments go out of business. This type of strategy isn’t limited to Palantir’s SPAC investments.

Moses Sternsteinexplainedthe implications of this kind of behavior for the broader startup ecosystem:

If my startup revenue (which I used to raise lots of VC dollars) is just your VC dollars (which you raised based on revenue that is, in fact, some other startup’s VC dollars, etc.),then it’s VC dollars all the way down.Different startups trading VC dollars with each other (and then calling it “revenue”) is no path to $100M in revenue.

One of the most common examples of this kind of behavior has been a fairly well-established playbook, most notablyexecuted by Brexin selling to YC startups. Brex started withbillboardsin SF, and eventually became a staple for YC-backed startups. As of November 2022,80%of YC companies were using Brex.

The strategy has worked well for Brex in times of plenty. But the question still remains, how well will that strategy play out in a world where funding dropped by30%from 2021 to 2022, and isn't looking much better in 2023?

The fervor of the last few years has been driven by what I call a “dream the dream” premium. Investors continued to see larger and larger potential outcomes. In early 2021, some of the most highly valued companies—Snowflake, Cloudflare, Datadog, Crowdstrike—were trading at an average of 52.9x NTM revenue.

Investors looked at that as the greatest driver of FOMO the world had ever seen. At the same time as companies were reaching absolute nosebleed valuations, VCs saw every single-digit million ARR fledgling startup as the next $100B company. Even if they missed by a few dozen billion, who cares about a $3M ARR company at $2B when it could be $40B? $50B? Venture funding shot up 100% YoY from$171Bin 2020 to$345Bin 2021.

More capital chasing more startups competing for (supposedly) unlimited total addressable markets with more dollars on sales and marketing. Noisier distribution meant you went looking for any and all revenue you could get. But when “the tide went out,” you saw a lot of weakness or unsustainability.

One customer realized they were spending$65Mon Datadog in early 2022. After growing52.8%in 2021, AWS saw growth slow down to18.8%in 2022 as people realized maybe they were spending too much on cloud computing.

That “dream the dream” premium started to become a nightmare. Klarna, at one time the world’s second most valuable fintech company at a$45.6Bvaluation, saw an 85% decline to$6.7B. Stripe, Instacart, Reddit,Cybereasonall saw drops of varying shapes and sizes.

The reality is that some of those companies are exceptional companies that will someday surpass their all-time highs, while some of them may not make it out of 2023 alive. But venture capital did very few favors to these companies as they pushed them deeper, and deeper into unsustainability with very little visibility into the path forward.

Is Venture Capital Killing Itself?

Venture capital is a complex business. The professionalized practice of venture investing isn't even100 years oldyet. In early 2013,Paul Grahamwascautioningfounders to be thoughtful of whether to raise money or not:

Such a high proportion of successful startups raise money that it might seem fundraising is one of the defining qualities of a startup. Actually it isn’t.Rapid growth is what makes a company a startup. Most companies in a position to grow rapidly find that (a) taking outside money helps them grow faster, and (b) their growth potential makes it easy to attract such money. It's so common for both (a) and (b) to be true of a successful startup that practically all do raise outside money.But there may be cases where a startup either wouldn't want to grow faster, or outside money wouldn't help them to, and if you're one of them, don't raise money.

In 2016,Bill Gurleywasmakingthe same point about ever-increasing pools of capital creating a generation of ever-hungrier startups:

Back in 1999, if a company raised $30mm before an IPO, that was considered a large historic raise. Today, private companies have raised 10x that amount and more. And consequently,the burn rates are 10x larger than they were back then. All of which creates a voraciously hungry Unicorn. One that needs lots and lots of capital (if it is to stay on the current trajectory).

Like Audrey II in Little Shop of Horrors, venture capital firms are becoming insatiablecapital agglomerators. “You don’t want to be a hungry unicorn? You don’t need any help growing? Too bad. Take the cash. We’ve got billions to deploy.”

But like an unreliable drug dealer, as soon as VCs got a generation of founders hooked on massive amounts of capital, ever larger valuations, and increasingly grand ambitions, they suddenly froze up and disappeared.That left in its wake a number of companies trapped in unsustainable territory with no extraction plan. No more funding is coming, and it’s sink or swim.

Venture capital, as an institution, has developed a number of “move fast and break things,” “grow at all costs,” and “blitzscaling” playbooks. There are very few playbooks for how to make progress from unsustainable to sustainable territory. Instead, you have a bit of a mentality of “passing the bag.” Who cares if Uber is at $30B of revenue, still trying to figure out “if our unit economics work”? The early investors made lots of money. The next phase is someone else’s problem.

All of this can start to feel really pessimistic. Don’t get me wrong. I’m a huge optimist. Economically, technologically, spiritually, and socially I believe things will be better in the future than they are today. I would consider myself an optimism maximalist. But, like an ostrich with its head in the sand, you don’t move forward if you’re not willing to take your head out and look around. This is an exercise in being willing to look around.

What’s wrong with the model for funding innovation that we have? How can we make it better? I always come back to thisideafromStephen Covey: circles of control, circles of influence, and circles of concern. While I can’t control a global economic system, there are certainly aspects of my firm, my companies, and those within the sound of my voice (or keyboard) that Icaninfluence.

I don’t want venture capital to go anywhere, because I don’t want startups to go anywhere. I don’t want there to be less experimentation, I want there to be more. But I also want there to be less of an attitude of shoot first, ask questions later.

Massive amounts of capital have distorted the way companies get built.

You can’t lay any of this blame with any one person or any single firm. It’s a prisoner's dilemma of herd mentality. Everyone is just playing the game on the field. But there is a real worry that the primary engine for innovation in the world is being built on the foundations of unsustainable frameworks.

The engine of progress is built by founders who use capital as an input to chase ambition. But as an output, people want to see actual progress — not a bloody spectacle of endlessly hungry murder plants, just looking for their next meal.

As a Partner and Co-Founder of Predictiv and PredictivAsia, Jon specializes in management performance and organizational effectiveness for both domestic and international clients. He is an editor and author whose works include Invisible Advantage: How Intangilbles are Driving Business Performance. Learn more...

0 comments:

Post a Comment