For Now, Prime Economic Impact of the US Iran Bombing Is Heightened Uncertainty

As of this morning, there are mostly 'what-ifs.' Reports on the scale and impact of the US bombing indicate that they were not as devastating as originally described - a nearly universal experience of war. That could lead to a variety of rabbit-hole chasing scenarios regarding what Iran could do to retaliate, what the White House could do if it is (again) embarrassed by overblown hype, and so on.

So the greatest short term economic impact appears to heightened uncertainty. Which is not nothing. That leads to rising rates, tighter credit, more cautious corporate decision-making, resource allocation hesitancy and a host of other decisions with financial consequences for a global economy already dealing with tariffs, layoffs and Al triumphalism. Leaders and executives have probably spent the weekend exploring how to anticipate or react to a variety of scenarios. That, in itself, has a dampening affect. Prudence suggests it should be expected to continue. JL

Noah Smith reports in Noahopinion and ING reports:

A lot of people are worried about the effect of the strikes on the global economy. The US claimed it had “obliterated” the facilities, while Iran reported only limited damage. This leaves us with the all-too-familiar sense that we understand far less than we thought we did. With more than 80% of oil flowing through Hormuz ending up in Asia, the impact on the region would be larger than that on the US. (But) uncertainty at elevated levels is another dampening factor for economic activity in the US and eurozone. So far there has been a lack of flight-to-safety. The most likely economic consequences from the US strikes will be on general uncertainty and on the price of oil. We remain in the Goldilocks fairytale for now.

On Sunday morning, the conflict in the Middle East escalated further with the US bombing three nuclear facilities in Iran. US President Donald Trump called the strikes “very successful” and US Defence Secretary Pete Hegseth claimed that the US had “obliterated” the facilities, while Iran reported only limited damage. This leaves us with the all-too-familiar sense that we understand far less than we thought we did this morning.

Along with uncertainty regarding the immediate impact of the US strikes, the longer-term consequences are also unclear at this point in time. Over the last 24 hours, the military reaction by Iran has been limited, fuelling the narrative that Iran doesn’t have or doesn’t want to use military means to react. Also, the US strike should not (yet) be seen as a ‘boots on the ground’ step by President Trump. It rather appears that the strikes were a “one and done mission” from the US - perhaps comparable to Trump’s assassination of Iranian general Qasem Soleimani in 2020. Let’s not forget that the right to declare war sits with Congress and not in the Oval Office. At the same time, it’s unlikely at this juncture that Trump would want to declare war, especially as he was elected partly on a mandate for the US to be less involved in global wars. Whether this approach is sustainable and realistic is a different matter.

Financial markets are currently waiting for Iran's response. There appear to be four main options: full escalation, potentially drawing in other nations such as China or Russia; disruption of the Strait of Hormuz; active or passive support for terrorist attacks in the US and Europe; or, alternatively, taking no action at all. We will abstain from speculating about the next steps and instead conclude that the most likely economic consequences from the US strikes will be on general uncertainty and on the price of oil. This analysis builds directly on our earlier assessment of the situation.

Impact on oil market

With recent events, our more severe scenario has become more likely: disruption in shipping through the Strait of Hormuz, a crucial choke point for global oil and LNG flows, with a quarter of seaborne oil trade moving through the strait. Roughly 20% of global LNG trade also moves through the strait.

And even if there’s scope for some flows to be diverted, an effective blocking of the Hormuz would lead to a dramatic shift in the outlook for oil, pushing the market into deep deficit. Spare OPEC production capacity wouldn’t help in this situation, as the bulk of it sits in the Persian Gulf. So, these flows would also have to go through the Strait of Hormuz.

While higher oil prices would see a boost in US drilling activity, it will take time for this additional supply to come to market. And the volumes will not be sufficient to offset losses through the Hormuz. Under a successful blockade, we would expect to see Brent trade up to $120/bbl in the short term. A prolonged outage (until the end of 2025) would likely see prices trading above $150/bbl to new record highs.

However, let’s not forget that even if Iran feels it needs to retaliate, blocking the Hormuz might be a step too far. Given the potential impact on oil flows and prices from such action, there would likely be a swift response from the US and others. Also, with more than 80% of oil flows through Hormuz ending up in Asia, the impact on the region would be larger than that on the US. Therefore, Iran would want to be careful not to upset the likes of China by disrupting oil flows. In addition, Iranian oil moves through the Hormuz, too. Blocking the strait would have an impact on these flows. Read more on this here.

Economic impact for US, eurozone and central banks

It’s probably also a sign of the times we are living in that a US strike on nuclear facilities has not immediately led to fire sales and panic in financial markets. It seems we've all grown accustomed to just how volatile and unpredictable the world has become.

Along with the threat stemming from higher oil prices, uncertainty at elevated levels is another dampening factor for economic activity in the US and eurozone. As if we haven’t had enough of this uncertainty recently. The new spike in oil prices threatens to disrupt the current narrative of more disinflationary than inflationary pressures in both the US and the eurozone, despite the expected inflationary impact of US tariffs.

Regarding the US and the Federal Reserve, inventory buffers may have allowed firms to put off decisions about raising prices, but that won’t be the case for much longer. We expect to see bigger spikes in the month-on-month inflation figures through the summer. The Fed’s recent Beige Book cited widespread reports of more aggressive price increases within the next three months. Rising oil prices only reinforce that outlook. At the same time, any disruption in the Strait of Hormuz would likely inflict only limited damage on the US economy. The US is a net energy exporter, with less than 10% of its oil imports coming from the Persian Gulf. Still, higher global oil prices would weigh on US consumers and businesses, though they might also boost the appeal of new domestic drilling projects.

For the Fed, this combination of potentially higher oil prices, new geopolitical uncertainty, and the still looming tariffs and ongoing trade tensions should strengthen the current wait-and-see stance. We expect the first Fed cut in the fourth quarter, potentially starting with a 50 basis-point cut in December

For the eurozone, the impact of higher oil prices on economic activity would be limited. According to a European Central Bank scenario, a 20% spike in energy prices could cut growth by 0.1pp in both 2026 and 2027. While this is a model-based outcome, the recent memory of elevated energy prices among consumers and businesses suggests that the actual impact of a renewed oil price shock could be even greater.

But it’s not just consumers and corporates who still vividly recall the surge in energy prices. The ECB and other major central banks also bear the scars of that episode. The term 'transitory' has effectively been erased from the ECB’s vocabulary. Simply applying today’s oil prices to the ECB’s own June macro projections would lift inflation by 0.3pp this year and 0.6pp next year. Say goodbye to fears of inflation undershooting and hello to renewed inflation concerns. A rate cut in July is now clearly off the table, and even the September decision could prove more contentious than anticipated after the decision in June.

Return of the dollar?

In this morning’s trading session, the dollar staged an expected rebound. The demonstration of US military strength, as well as the fear of higher oil prices, weakened the euro. Looking ahead, one of the key questions is whether US involvement in the conflict could restore the dollar’s safe-haven appeal. Here, a crucial factor will be the duration of any potential Strait of Hormuz blockade. The longer such a blockade lasts, the higher the likelihood that the value of safe-haven alternatives like the euro and yen is eroded, and the dollar can enjoy a decent recovery.

If Iran’s retaliation is contained, the US does not follow through with more attacks, and the oil spike proves temporary, support for the dollar should vanish quite rapidly. The market continues to prefer strategic dollar shorts even at expensive levels, so a temporary geopolitical shock may simply see markets sell the USD at more attractive entries. Read more here.

No safe-haven effect, yet

What has been remarkable so far has been the lack of flight-to-safety in bonds. Right from the initial strikes through to 12-13 June, the market reaction showed minimal movement into traditional safe havens - neither Treasuries, Bunds, nor rates markets more broadly saw significant inflows. Bond markets quickly moved on. Should things turn dramatically more sinister in the coming days, there must be a route for this to flip, and for cash to fly out of risky assets and into core bonds.

If yields were to lurch lower in the near term, it could reflect a growing market discount for significant risks to the broader global macroeconomic outlook.We have two sizeable wars ongoing, with minimal expectation for containment. That, plus the negatives coming from the tariff tax wedge in the US, has a feedback loop that absolutely can result in a flight out of risky assets and into bonds.

That said, and given what we know, market rates will likely be primed to discount two things. First, a “positive” outcome, in the sense that a so-called bad actor has had its nuclear bomb-making capability severely downsized. Second, even on such an outcome, the rates market will fret about any inflation sting in the tail through upward pressure on energy prices amid wider regional angst. Given that, the dominant reaction should be some curve steepening pressure, likely from the long end. Professional investors can read more here.

Credit unmoved, for now

Credit markets continue to be unaffected by the growing geopolitical tensions, for now. A further, more drastic escalation may result in a risk-off modus. Credit spreads opened up this morning unchanged in both CDS and cash. Meanwhile, the primary markets remain open and see plenty of deals coming through. Spreads are sitting in the bottom half of the trading range, but still have 6-10bp of tightening potential to the bottom end. At those tighter levels, the relative value between credit and other asset classes (Govies and SSAs) becomes very limited, and thus, asset allocation comes into question.For now, credit is still supported by the large demand and cash readily available. Whilst technicals, on paper, look less strong (higher supply, slower inflows, ECB maturities), the credit space remains well bid and highly demanded, as evidenced by the tight spreads, and the very low NIPs and well-oversubscribed books in the primary market.The growing tensions and potential economic impacts (for example, energy price impacts) add to the growing list of volatility drivers in the complicated credit cocktail. But we remain in the Goldilocks fairytale for now.

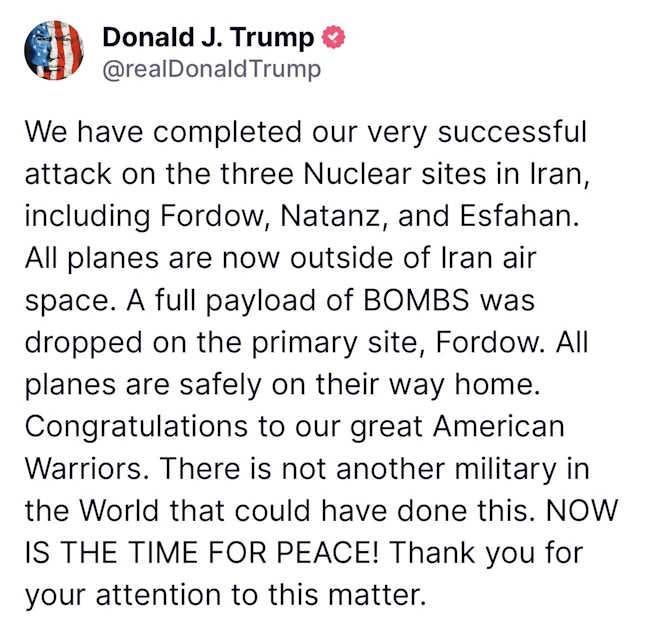

Noah Smith Well, I suppose Trump doesn’t actually chicken out of everything. The U.S. has bombed Iran’s three nuclear enrichment facilities. Here was Trump’s announcement of the strikes on social media:

The consequences of these strikes aren’t yet clear. I’ve seen a lot of hyperventilating takes about how World War III is now underway, but this seems obviously false. The world may indeed be in the foothills of WW3, but even if it is, it’s highly doubtful that strikes on Iran’s nuclear facilities will be what push us over the edge. Iran has friendly relations with China and Russia, but neither one seems to have any interest in coming to Iran’s aid in the current conflict — China doesn’t appear to be interested in getting in wars outside its own neighborhood, while Russia is simply too preoccupied with its war in Ukraine.

Nor do I expect the strikes on Iran to lead to a U.S. “boots on the ground” invasion. First of all, there’s the TACO factor — Trump was only willing to conduct some very limited airstrikes, and only targeted narrowly at Iran’s nuclear program, and he was only willing to do it after Israel had already neutralized much of Iran’s long-range strike capability. So far, the best Iran has been able to do in this war was to kill a few dozen Israeli civilians, and even its ability to do that much might have been mostly neutralized. Iran’s leaders are issuing dire threats against the U.S. in response to today’s strike, but there’s just not much they can do other than take some weak potshots at U.S. bases in Iraq.

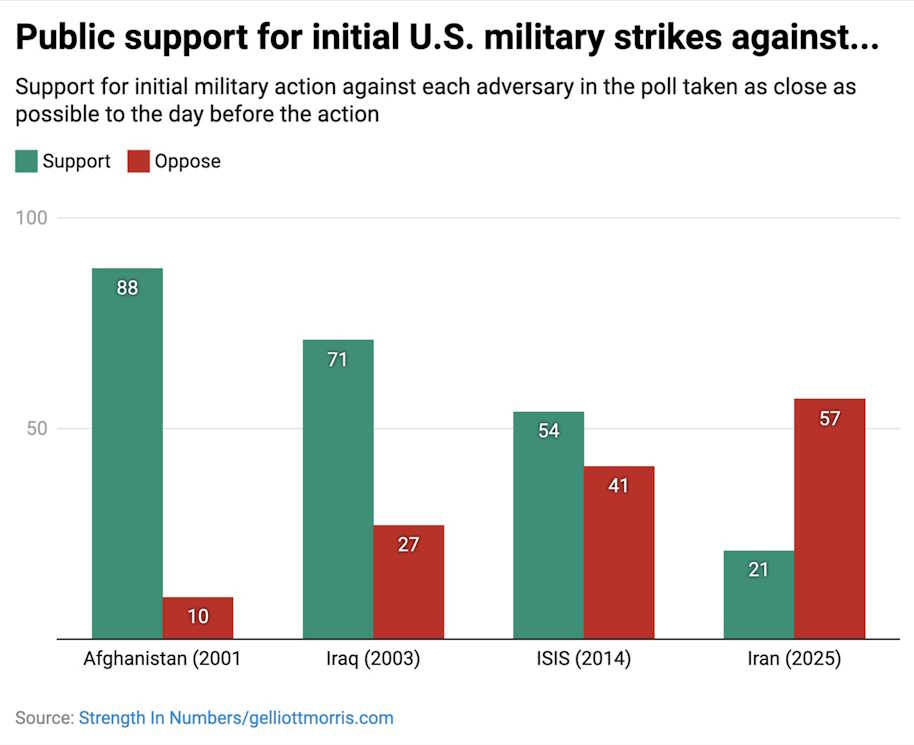

So Trump was taking almost no military risk with these strikes — they don’t show a new, bolder, braver Trump. And the President knows that public opinion is strongly against a war with Iran:

So while these things are always hard to predict, the likeliest outcome seems to be that Trump simply conducts airstrikes until Iran’s three nuclear facilities have been destroyed (if that isn’t the case already), and then backs off and leaves the conflict to the Israelis. Trump’s assassination of Iranian general Qasem Soleimani in 2020 turned out similarly.

But even though a major war seems highly unlikely, it’s still worthwhile to consider possible economic consequences. When we’re talking about the Middle East, that really means one thing: oil.

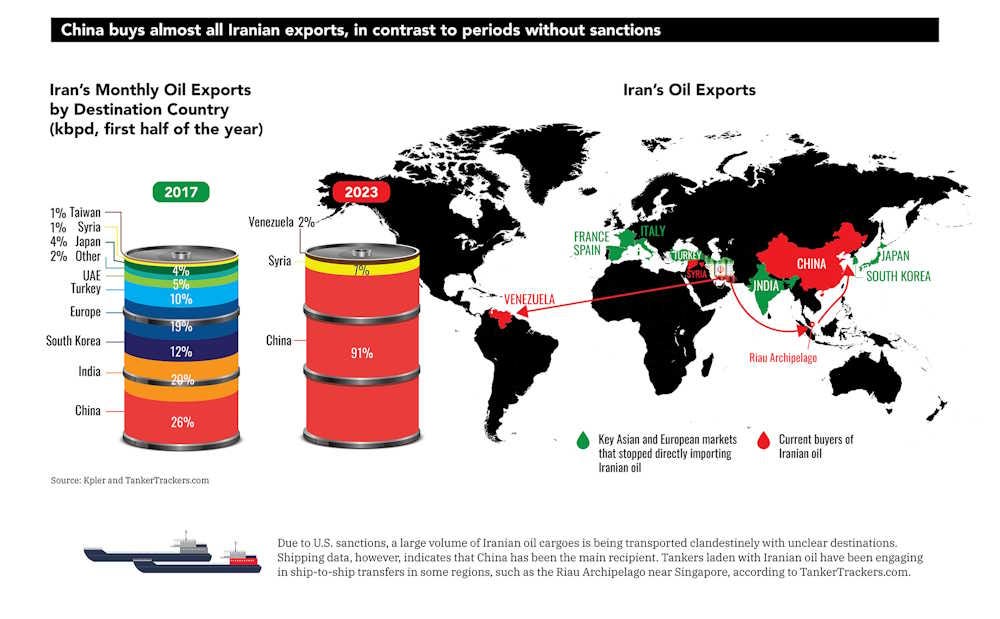

There are two ways that the Iran war might affect oil prices. First, Israel’s strikes on Iran may reduce Iran’s own oil exports. Iran is responsible for about 3-4% of world oil production, though only around a third of that gets exported. Almost all of Iran’s oil exports go to China:

Second, and more importantly, Iran may close the Strait of Hormuz, which is the main transit point for Middle Eastern oil. About one fifth of all global oil supply goes through the Strait of Hormuz, so if it were closed off, that would be a very big deal. Iran has threatened to close the strait throughout the conflict with Israel, and in the wake of the U.S. strikes, it has reportedly announced that it’s closing the strait to all ships bound for Europe:

It’s not entirely clear whether Iran has the military ability to close off the strait, but most analyses I read say that they could probably do it. Iran has a vast and diverse array of weapons that it could bring to bear, and the strait is very narrow, meaning that its weapons wouldn’t have to operate over long range. The Houthi militia, which is supplied by Iran, has shown the ability to almost completely scare away all shipping from the exit of the Red Sea.

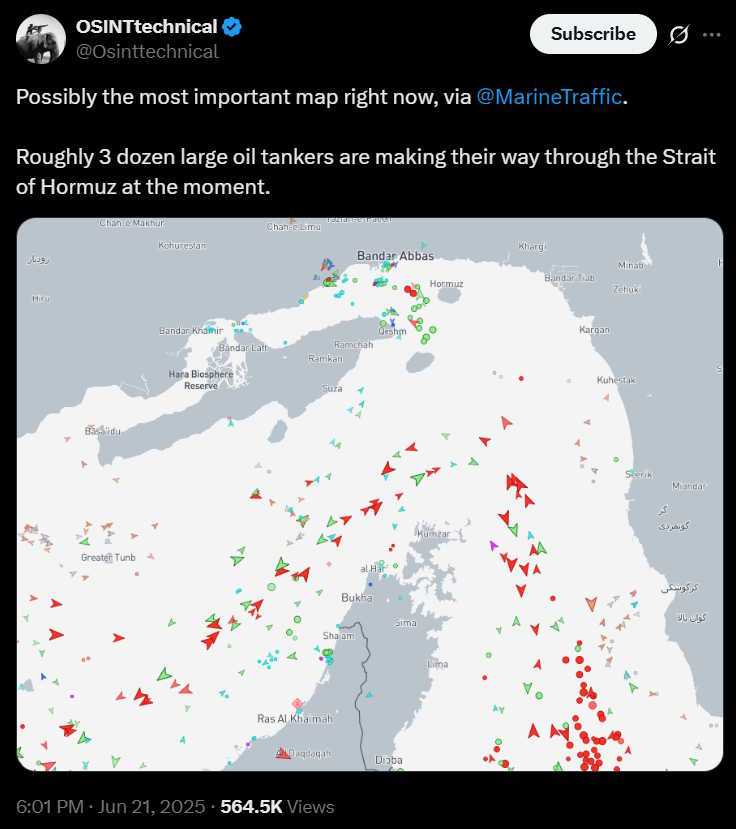

Even if Iran’s forces in the strait could eventually be defeated, the risk of attack would make civilian ships avoid the area entirely. Who wants to try sailing through a war zone? Already, tankers are scrambling to leave the area:

So a lot of people are worried about the impact of Trump’s strikes on the global economy. But to be honest, I think these worries are overblown. And the U.S. itself is even more insulated from oil disruption than other countries.

VEVOR frequently offers a variety of Vevor promotion codes that provide great savings on a wide range of products, from industrial tools to home and garden equipment.

I am grateful for your willingness to impart your expertise and experience. It is astonishing how much information is available on your website Baseball bros.

As a Partner and Co-Founder of Predictiv and PredictivAsia, Jon specializes in management performance and organizational effectiveness for both domestic and international clients. He is an editor and author whose works include Invisible Advantage: How Intangilbles are Driving Business Performance. Learn more...

2 comments:

VEVOR frequently offers a variety of Vevor promotion codes that provide great savings on a wide range of products, from industrial tools to home and garden equipment.

I am grateful for your willingness to impart your expertise and experience. It is astonishing how much information is available on your website Baseball bros.

Post a Comment